The old saying “a rising tide lifts all boats” is a phrase many investors would associate with the idea that rising markets will benefit all stocks to some degree. However, during the recent 3-year bull run, returns have been dominated by sector specific rallies, many of them short-lived. Bucking this trend, the auto and housing sectors have shown consistent strength over the last few years, and should continue as long as interest rates remain at low levels and the U.S. economy continues to limp along. This strength is sporadically beginning to filter into micro-caps.

This brings us to Consumer Portfolio (NASDAQ:CPSS),our first of many stocks we will discuss that should get a lift from the current economic trends.

As GeoInvesting followers know, we love uncovering hidden clues that prompt us to initiate stock positions before the masses do. And we have a big clue from CPSS. During the company’s 2012 second quarter conference call, the company commented that investors should reference 2004 through 2007 for a barometer on how it can grow its business. Management stated:

“Go back to the last go-around before the recession; look at that growth cycle and we should be able to grow like that; look at ‘04 through ‘07 as a gauge to how we can grow.”

The company did not mention this information in its 2012 second quarter press release. The call provided astute investors with an opportunity to take advantage of this information arbitrage. Informed investors rode the stock from $1.98 to a high of $4.87 since the 2012 second quarter release, helped along by strong 2012 third quarter financial results, but pulled back to $3.50 (as of close on 10/9/2012). We issued our first alert to GeoInvesting members on August 17, 2012 at $2.80. We consider the pause in CPSS shares momentum as a healthy retracement that should give investors who missed the first run in CPSS to get their second chance now.

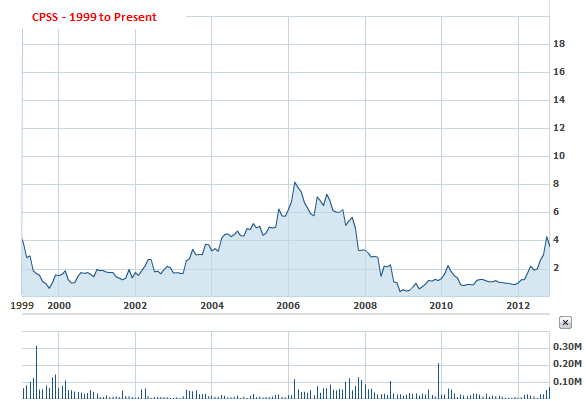

During 2004 to 2007 revenues grew from $132.7 million to $394.6 million, while 2007 EPS reached a high of $1.06 on a pretax basis ($0.61 after tax). The stock price topped out at $8.84 in May 2006 and actually reached $18.25 in September 1997 when EPS was around $1.66 ($1.00 taxed). At the 1997 and 2006 peaks, shares were trading at a P/E of around 15 on a taxed EPS. As a reference point to see where CPSS is in its growth cycle, consider that we project 2012 revenues to come in at around $185 million, up from $143 million in 2011, and that the company’s quarterly pre-tax EPSis tracking at$0.11, which has been increasing on a sequential basis for 4 quarters, a trend we expect will generally continue throughout 2013. For 2013, we expect CPSS to minimally achieve EPS of $0.55 ($0.35 taxed) on revenues of $235 million. Placing a P/E of 15 on our 2013 estimates yields a near-term price target of $5.25. We will discuss upside to our estimates later in this report including why we believe CPSS should be able to attain higher EPS at revenue levels similar to the past. Due to favorable industry dynamics, we also believe it will trade ahead of its fundamentals.

CPSS operates an automobile finance lending business catering to sub-prime borrowers. Specifically, it engages in purchasing and servicing retail automobile contracts originated by franchised automobile dealers and select independent dealers in the sale of new and used automobiles, light trucks, and passenger vans. The company, through its automobile contract purchases, provides indirect financing to the customers of dealers with limited credit histories, low incomes, or past credit problems.

Encouraging automotive sales data, the increase in sub-prime borrowers due to the great recession, fewer alternatives for traditional financing avenues for consumers and a low interest rate environment are factors that bode well for CPSS.

The Challenge

The company’s revenues are significantly impacted by the amount of its total managed loan portfolio (TMP) mainly amassed through proprietary loan originations and at times by purchasing existing loan portfolios. The bulk of CPSS’s quarterly revenue is derived from the income it earns on its sequentially previous TMP. In order for CPSS to grow its revenue base it must more than replenish the amount of its loan portfolios that mature, are paid down or become delinquent. The key for the company to obtain profitability is to:

- Minimize bad debt exposure

- Effectively manage the costs to acquire and service its portfolios

- Maximize the spread between the rate it earns on its portfolios and the cost to finance its portfolios.

When all cylinders are firing, CPSS has a history of exhibiting strong and consistent growth. Sales in 1999 were $14.8 million and rose every year through 2007, topping out at $394.5 million.

| Year | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 |

| Rev in million | 14.8 | 36.0 | 62.6 | 93.3 | 100.9 | 132.7 | 193.7 | 278.9 | 394.6 |

Delinquency rates as a percentage of TMP is a key metric to monitor and can give investors a sneak peek into the health of CPSS’s business before an unfavorable rise in this rate manifest in its financials. In 2006, one year before CPSS reached peak sales in the most recent bullish business cycle, the company began to encounter efficiency problems when delinquency rates began to steadily rise. In retrospect, the rise in delinquency rates was a sign of the upcoming economic collapse and in late 2009 reached a high of slightly over 8%. Ideally, the preferred delinquency rate should range between 3 to 5 percent, depending on seasonal factors. Revenues also entered a multi-year decline, retracing to $143 million in 2011. Obviously, CPSS was uniquely impacted by the recession since its business caters to the sub-prime market. The company was forced to write off or realize losses on a large portion of its loan portfolios, reduce loan originations and reassess its underwriting standards.

The following chart shows that the CPSS shares basically followed the trend of company operations.

Meeting the Challenge:

CPSS quickly addressed the challenges of a new business environment by taking steps to reduce the risk characteristics of its TPMs by:

- Becoming more vigilant in the lending process

- By decreasing objectivity of credit decisions made by the company’s staff responsible for vetting through initial loan applications. This is accomplished by increasing the amount of initial credit decisions that are made through the company’s software program. CPSS now makes initial credit decisions on 99% of incoming applications, as opposed to about 85% pre-crisis.

- Increasing diligence in the pre-funding qualification process.

- Improving delinquencies which stood at 4.64% as of September 30, 2011.

Also on CPSS’s side is the fact that the industry environment that it operates in is conducive to a sustained recovery in its operations:

- Auto sales are at the highest levels since February 2008.

- The current restrictive lending environment and increased scrutiny in lending practices has not only led to an increase in the number of sub-prime borrowers, but the quality of sub-prime borrower is now higher. Thus, you have a situation where loan portfolios are higher quality than the past at sub prime rates.

- The low interest rate environment allows CPSS to borrow money to finance its loan originations and portfolio purchases at favorable rates. This has led to a greater spread between cost of funds and lending rates than in past periods. (For example, greater margins.)

We Are Attracted To Management Teams That Do What They Say

The operational adjustments are bearing fruit. CPSS’s turnaround firmly took hold at the conclusion of the third quarter of 2011 when the company reported its thirteenth consecutive quarterly loss, but indicated that profitability was right around the corner.

Management’s comments from the third quarter 2011 release:

“In addition to completing the Fireside portfolio acquisition, our new contract purchases have increased to the point where we are now growing the CPS portfolio once again. Both of these accomplishments will have a positive impact on our profitability in future quarters.”

Since then, the company has reported 4 straight quarters of year over year sales and EPS growth and 4 straight quarters of sequential EPS growth.

| Year | 2012 | 2011 | 2010 |

| March | Rev 44.5

EPS 0.02 |

Rev 32.4

EPS (0.23) |

Rev 44.6

EPS (0.33) |

| June | Rev 44.1

EPS 0.05 |

Rev 31.2

EPS (0.35) |

Rev 38.5

EPS (0.39) |

| September | Rev 47.9

EPS 0.11 |

Rev 33.8

EPS (0.20) |

Rev 36.8

EPS (0.20) |

| December | Rev TBD

EPS TBD |

Rev 45.8

EPS 0.01 |

Rev 35.3

EPS (0.87) |

| Totals | Rev TBD

EPS TBD |

Rev 143.1

EPS (0.76) |

Rev 155.2

EPS (1.90) |

Management commentary from its 2012 second and third quarter continued to express optimism and build momentum. We expect CPSS to report 2012 fourth quarter revenues of around $50 million and full year 2013 revenues to conservatively rise at least 27% to $235 million.

2012 Second Quarter Commentary:

“The second quarter of 2012 marks another milestone in our recovery from the financial crisis,” said Charles E. Bradley, Jr., Chairman and Chief Executive Officer. “We are now growing our total managed portfolio sequentially as our new contract purchases are more than offsetting the runoff of the Fireside Bank portfolio and our 2007 and 2008 vintages. As we can see from our financial results, the operating leverage inherent in our business is once again becoming evident. This bodes well for our future profitability.

Operationally, the second quarter was also solid. New contract purchases increased 15% from the first quarter and yields and credit demographics of the new paper remain attractive. Asset performance metrics continue to be very strong as well with year-over-year net charge-offs and delinquencies continuing to decline. In addition, we achieved another record low funding cost on our June securitization.”

2012 Third Quarter Commentary:

“We are extremely pleased with our third quarter financial results,” said Charles E. Bradley, Jr., Chairman and Chief Executive Officer. “It was our first quarter of organic sequential revenue growth since 2007 and the onset of the financial crisis. This demonstrates that we are well positioned within the auto finance industry to continue growing our managed portfolio.”

The Big Clues Not Present In Press Releases Indicating That CPSS Is Entering A Period Of Growth Of Sustained Sales And EPS Growth

We stated at the beginning of our article that during the company’s second quarter 2012 conference call the company commented that investors should reference 2004 through 2007 for a barometer on how it can grow its business.

The 2012 third quarter conference call also contained information that was not present in its associated press release.

The company is currently originating loans at a rate near $50 million per month versus near $30 million a month in 2011. In the 2012 third quarter conference call, management discussed its goals for monthly origination volume to reach $75 million in 2013 and get back to the $100 million to $125 million level within one to two years. They also commented that the current cost of funds is better now than it was during previous growth cycles. This means that higher EPS can be attained at similar revenue sales levels of the past.

Recent financial results support this opinion.

CPSS reported revenues of $67.2 million in its 2006 second quarter, equating to EPS of $0.11. On much less revenue of $47.9 million in its 2012 third quarter, EPS reached $0.11.

Analyst estimates do not exist for CPSS. However, armed with…

- Monthly loan origination goals, and

- Knowledge of stable historical relationships that define CPSS’s portfolio characteristics (the rate at which various portions of its TMP decrease over time, which has recently equated to about 15% to 20%)

…it is fairly simple to calculate growth in TMP and associated sales and EPS numbers.

We calculate that CPSS’s total managed portfolio will experience substantial growth the over the next 18 months. Specifically, we estimate that the TMP will increase from the $844.9 million balance at the end of its 2012 third quarter to near $1100 million by the end of 2013. Over the last 9 quarters the company has linearly increased the rate of return it has earned on its TMP, increasing from 3.6% in the second quarter of 2010 to roughly 6% in the third quarter of 2012 (TMP * rate of return = revenues) . Assuming CPSS gradually achieves its monthly loan origination goals and maintains 2012 third quarter pre-tax margins of near 6%, we estimate the company will report 2012 revenues of $185 million and grow 2013 revenue to $235 million with EPS of $0.55 (or $0.35 fully taxed). Plenty of upside to our estimates exist due to the following factors:

- We have only assumed that the company will originate loans and not purchase any loan portfolios.

- Our pre-tax margin assumptions are likely too conservative since the company has explicitly stated that its operations are more efficient now than they were in the 2004 to 2007 bullish period. At 8% of revenues, core operating expenses could see significant improvements to closer to 5%, where they were during the 2004 to 2007 period.

- As we mentioned earlier in this report, the company stated that the next 3 years should grow in a similar fashion as the 2004 to 2007 period. This implies that 2013 revenues could top our estimate. Our estimates do not take into an account any contribution from ancillary revenue sources such as products and services it offers to its dealers.

Conclusion

CPSS appears to be one of the most opportunistic investing ideas we have recently come across. Even our most conservative scenario yields attractive investment returns. Given the facts, it looks like CPSS is well on its way to experiencing a dramatic multi-year predictable run in sales and earnings. We believe it is likely that CPSS will be able to eclipse its current quarterly pre-tax EPS run rate of $0.11 in the very near future as revenues eventually surpass $60 million. We believe the stock could quickly trade at $5.25 (P/E of 15 * taxed 2013 EPS estimate of $0.35) on the low end and easily surpass this target if our more aggressive assumptions materialize. Keep in mind that the company traded near $9.00 during 2006 when it reported pre-tax EPS of $0.55 (fully taxed $0.35). We consider the recent pull back in its shares as an early present from Santa.

Caveats

- Potentially lax underwriting standards by CPSS’s competition

- Increasing interest rate environment

- Negative book value per share; however, improving operations should soon put the company in a solidly positive book value position.

- A credit crisis which results in a significant reduction in the access to funds to securitize sub-prime loans and/or an increase in associated costs.

Disclosure: Long CPSS

Disclaimer:

You agree that you shall not republish or redistribute in any medium any information on the GeoInvesting website without our express written authorization. You acknowledge that GeoInvesting is not registered as an exchange, broker-dealer or investment advisor under any federal or state securities laws, and that GeoInvesting has not provided you with any individualized investment advice or information. Nothing in the website should be construed to be an offer or sale of any security. You should consult your financial advisor before making any investment decision or engaging in any securities transaction as investing in any securities mentioned in the website may or may not be suitable to you or for your particular circumstances. GeoInvesting, its affiliates, and the third party information providers providing content to the website may hold short positions, long positions or options in securities mentioned in the website and related documents and otherwise may effect purchase or sale transactions in such securities.

GeoInvesting, its affiliates, and the information providers make no warranties, express or implied, as to the accuracy, adequacy or completeness of any of the information contained in the website. All such materials are provided to you on an ‘as is’ basis, without any warranties as to merchantability or fitness neither for a particular purpose or use nor with respect to the results which may be obtained from the use of such materials. GeoInvesting, its affiliates, and the information providers shall have no responsibility or liability for any errors or omissions nor shall they be liable for any damages, whether direct or indirect, special or consequential even if they have been advised of the possibility of such damages. In no event shall the liability of GeoInvesting, any of its affiliates, or the information providers pursuant to any cause of action, whether in contract, tort, or otherwise exceed the fee paid by you for access to such materials in the month in which such cause of action is alleged to have arisen. Furthermore, GeoInvesting shall have no responsibility or liability for delays or failures due to circumstances beyond its control.