Summary:

- 344 days of time-lapse surveillance of CGA’s high-margin Jinong fertilizer factory, contributing 75% of CGA’s gross profit, shows it only shipped around 10% of the volume CGA reports it sold.

- 51 days of time-lapse surveillance of CGA’s low-margin Gufeng factory found 24% to 34% less volume shipped compared to volume sold disclosed in SEC filings.

- We interviewed current and former CGA employees, one of whom told us that CGA’s Jinong factory exaggerated its production specifically for its stock listing in the U.S.

- CGA’s auditor, Kabani, signed off on $113 million of outrageous PP&E reclassifications and deferred marketing assets wiping out CGA’s cash. Kabani was also auditor of the L&L Energy (LLEN) fraud.

- In addition to potentially falsified sales volumes, CGA’s PP&E reclassifications could constitute capex fraud that in and of itself could be enough to have the company halted and delisted.

Special Note:

Today, aware of the rising short interest in its stock and less than a day after our final attempt to confront management, CGA announced a one-time dividend of 10c per share ($3.3 million in aggregate), payable four months from now. We doubt that CGA has the capability or desire to actually pay this dividend. CGA’s dividend announcement reminds us of China Media Express (CCME), which announced a dividend policy following a short seller’s report calling the company a fraud. CCME never paid.

China Green Agriculture’s (CGA) Backstory: Financials Challenged Since 2010

China Green Agriculture (CGA) was taken public in December of 2007, via a reverse merger with a U.S. shell company supplied by Belmont Partners, touted as the “CarMax of shell corporations” by its CEO Joseph Meuse. Belmont and Meuse later settled SEC fraud charges and Meuse was barred from the penny stock business. The following will show how the company’s financials have been challenged since 2010.

In July 2010, “Alfred Little” published excerpts from a detailed due diligence report on China Green Agriculture that found CGA had exaggerated the sales of its key Jinong fertilizer factory, paid only a fraction of the Chinese taxes it claimed, overstated the purchase price of land-use rights by 4x, reported earnings of 5x to 6x what it disclosed in Chinese SAIC filings, and used a tiny auditor, Kabani & Co., whose only other substantial Chinese client at the time was L&L Energy (LLEN).

In January 2011, J Capital Research published the results of their own very thorough investigation that likewise concluded that CGA vastly inflated its fiscal 2010 sales by a factor of at least four times. J Capital believed that its findings were:

“…very serious and merit delisting [of CGA] from the NYSE. In fact, it should be embarrassing to such a prestigious exchange as the NYSE to host such an irregular company. We wonder whether an excess of entrepreneurial spirit could have affected NYSE, which has been actively seeking Chinese IPOs and seeking its own listing in Shanghai.”

Following the J Capital Report, analyst Ingrid Yin of Brean Murray downgraded CGA to a “sell” citing CGA’s failure to provide evidence refuting the short sellers’ reports, perhaps the first time a sell-side analyst covering Chinese companies sided with short sellers.

On January 7, 2011, without informing shareholders, CGA Chairman Li Tao told the Chinese 21st Century Business Herald that the SEC had begun an informal inquiry into the company following the Alfred Little publication.

On September 5, 2012, the SEC informed CGA that it had concluded its investigation without recommending any enforcement action against the company, according to CGA’s fiscal 2012 10-K.

For the next two years, CGA survived as a public company, but was awarded a miserably low valuation by investors who discounted its questionable financials.

Now, over four years after the first allegations against CGA, GeoInvesting intends to put an end to the debate. We believe CGA should be halted, investigated, and delisted from the exchange, much the same as many others before it.

One Year of Time-Lapse Surveillance and Over 2 Million Images Shows Little Production at CGA’s Key Jinong Fertilizer Factory

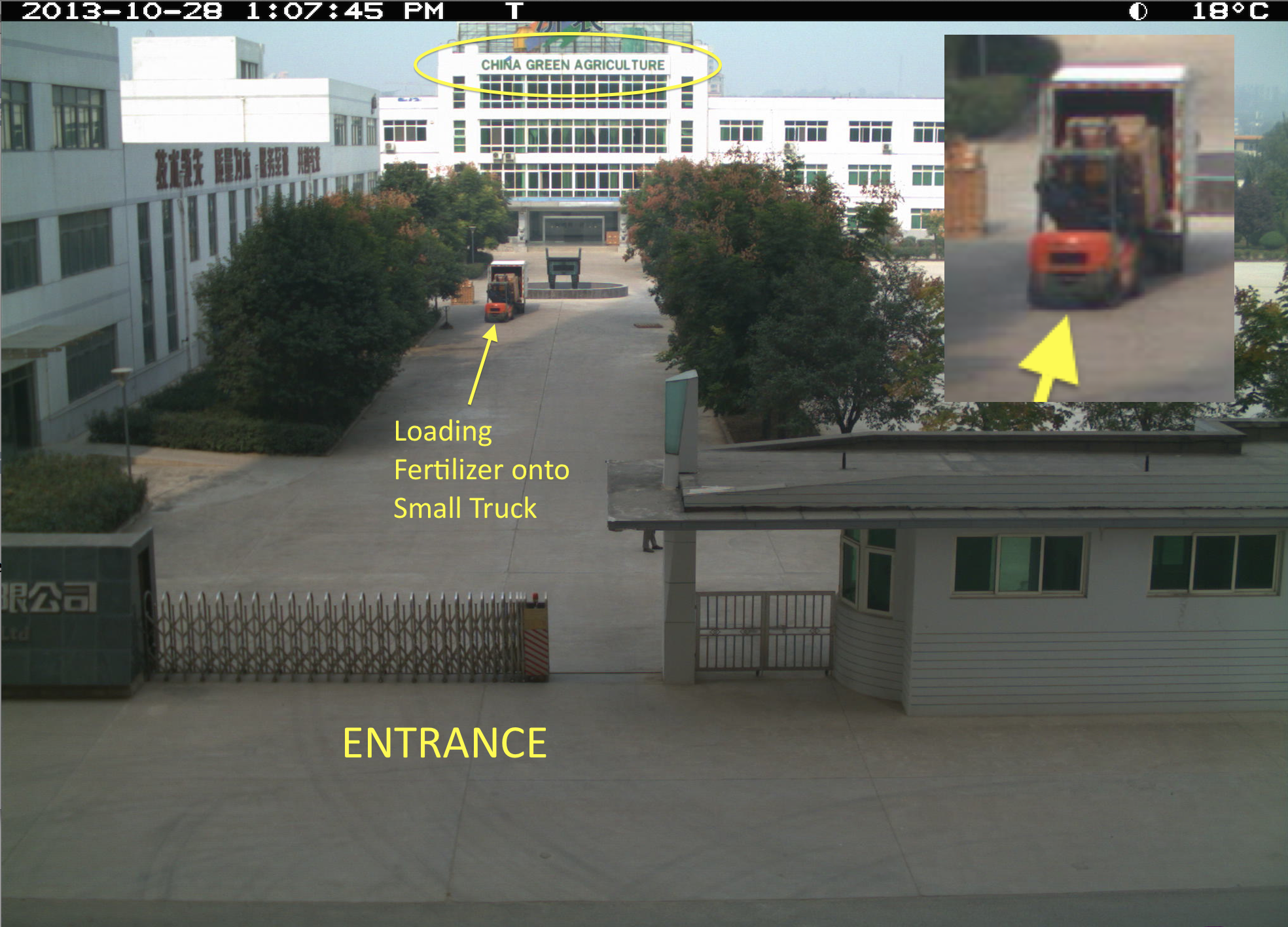

In August 2013, investigators set up a time-lapse surveillance camera in an apartment overlooking the only entrance to CGA’s Jinong fertilizer factory, which according to CGA’s SEC filings produces CGA’s highest margin premium liquid organic fertilizers and concentrated powder fertilizers. According to CGA, its Jinong division generated $117,706,033 in Fiscal 2014 fertilizer sales and $69,076,938 in gross profit, equal to 50.4% and 75.7% of CGA’s total sales and gross profit for the year.

The following satellite image taken August 13, 2014 is marked up showing the Jinong factory and the location of the factory entrance and camera across the street:

The following sample image taken by the camera on October 13, 2013 shows an unobstructed view of boxes of liquid fertilizer bottles being loaded onto a small truck inside the Jinong facility:

From August 17, 2013 until August 24, 2014, our camera took pictures of the entrance and staging area of Jinong factory every 10-15 seconds, 24 hours a day, interrupted only by holidays, brief battery changes, and occasional camera/operator failures. This amounts to a total of 344 days of time-lapse surveillance footage – all of which indicates to us that CGA has inflated its Jinong fertilizer sales by around 10x.

The following table shows CGA’s reported fertilizer sales (in metric tons) by its Jinong division for the fiscal 2014 period July 1, 2013 to June 30, 2014:

| Quarter Ending | Tons Sold |

| June 30, 2014 | 12,528 |

| March 31, 2014 | 14,719 |

| December 31, 2013 | 15,510 |

| September 30, 2013 | 17,872 |

| Fiscal Year Total | 60,629 |

Source: CGA 10-Q and 10-K filings.

As you can see from the table, Jinong sold 60,629 tons of fertilizer during the twelve months ended June 30, 2014. On average, Jinong was thus purportedly selling an average of 166 tons of fertilizer per day (60,629 tons divided by 365 days) during fiscal 2014. The Jinong factory primarily ships its fertilizer in the small truck shown in the sample photo above, which based on our observation, is usually only partially loaded with around 5 tons of fertilizer. Larger trucks are occasionally used, on which we would expect to see an average of around 10-15 trucks per day delivering fertilizer from the Jinong factory.

However, during the 344 days we filmed the Jinong factory, we observed an average of only one to two trucks per day, shipping 13 (low estimate) to 20 (high estimate) tons of fertilizer from the factory, or only 4,800 to 7,100 tons for the entire year, compared to the 60,629 tons CGA reported Jinong sold in fiscal 2014.

In our opinion, CGA’s Jinong factory is simply not producing anywhere near the level of fertilizer sales that CGA reports in its public filings. Jinong’s fertilizer sales, accounting for over half of CGA’s reported total sales and 75% of CGA’s gross profits simply cannot be true, given the video evidence we have seen. With such a small level of production, it is doubtful that CGA’s Jinong factory can earn a profit at all, after accounting for its overhead and high selling expenses.

To show just how “dead” the Jinong factory is we compiled 24 sample time-lapse videos spanning the year during which we filmed the factory. In each video, we note the daily count of trucks exiting the factory (whether full of fertilizer or not). The 24 sample time-lapse videos can be viewed by clicking the thumbnails below:

|

|

|

| 8/29/2013 | 9/14/2013 | 9/29/2013 |

|

|

|

| 10/14/2013 | 10/29/2013 | 11/14/2013 |

|

|

|

| 11/29/2013 | 12/14/2013 | 12/29/2013 |

|

|

|

| 1/14/2014 | 1/29/2014 | 2/14/2014 |

|

|

|

| 2/29/2014 | 3/14/2014 | 3/29/2014 |

|

|

|

| 4/14/2014 | 4/29/2014 | 5/14/2014 |

|

|

|

| 5/29/2014 | 6/14/2014 | 6/29/2014 |

|

|

|

| 7/14/2014 | 7/29/2014 | 8/14/2014 |

Jinong Employees Readily Admit to Low Volumes and Book Cooking for U.S. Listing

After 9 months of filming the Jinong factory, we decided to further our investigation by questioning the gate guards regarding the level of activity at the factory. On May 22, 2014, our investigators interviewed one of the Jinong factory’s guards inside the guardhouse adjacent to the entrance to the facility. The following time-lapse image shows the investigators approaching the guardhouse:

A short time-lapse video of the investigators’ visit to the guardhouse is available here.

A photo of the guard holding the investigators’ completed survey form appears below:

The key findings of the interview of the gate guard were:

- The Jinong factory has 40 regular employees and 70-80 people in total

- Jinong has one cargo delivery truck and two drivers (supplemented by trucks the company rents)

- There is only one entrance to the factory

- The factory makes deliveries approximately once per week, even in the busy season

The recorded interview of the gate guard can be viewed here. A transcript of the interview can be found here.

Former Warehouse Director Admits Jinong Production was Exaggerated for U.S. Listing

On April 25, 2014, an investigator interviewed Chen Lianpeng, the former warehouse director of the Jinong fertilizer factory who we discovered after finding his resume he had posted to an online Chinese jobs website. The key findings of the interview of Mr. Chen were:

- He had worked for CGA for about 5 years, resigning in March 2012

- Jinong’s fertilizer production was falsely reported outside “for the listing” (referring to the U.S. public listing) as 20,000 tons in 2011

- 20,000 tons of production is not possible, unless the factory ran continuously for nine months of the year, which was never the case

- He emphatically claimed that the total actual production of all types of fertilizers was less than 8,000 tons in 2011, and roughly stable at only 8,000 tons per year

- There was no fertilizer production from January to March 2012

Mr. Chen’s comment that CGA’s Jinong factory production was stable at only 8,000 tons per year is completely at odds with Jinong’s quarterly reported sales volume in calendar 2011 (the last full year Mr. Chen worked for Jinong) of 57,447 tons:

| Quarter Ending | Tons Sold |

| December 31, 2011 | 14,798 |

| September 30, 2011 | 16,846 |

| June 30, 2011 | 14,254 |

| March 31, 2011 | 11,549 |

| Calendar Year Total | 57,447 |

Source: CGA 10-Q and 10-K filings

Mr. Chen’s comments yield a capacity utilization rate of just 14.5% (8,000 tons divided by Jinong’s 55,000 ton capacity), far below the 87% capacity utilization rate disclosed on page 10 of the CGA’s fiscal 2011 10-K ended June 30. (In its 2011 10-K, CGA calculated Jinong’s capacity utilization rate by dividing Jinong’s 48,038 tons sold in fiscal 2011 by its stated annual production capacity of 55,000 tons).

Mr. Chen recalled that Jinong produced no fertilizer from January to March 2012, contradicting the 14,925 tons CGA reported were sold by Jinong in the March 2012 quarter. Thus the Jinong factory’s production seemed to be declining at the time Mr. Chen quit working. Our time-lapse surveillance showed the production had fallen to under 8,000 tons (annualized).

The recorded phone interview of Mr. Chen can be viewed here. A transcript of the interview can be found here.

Gufeng Factory Fertilizer Shipments Also Appear to be Lower Than Volume Sold

CGA acquired the low-margin, high-volume Gufeng fertilizer factory in July 2010. Gufeng produces various granular fertilizers that have much lower selling prices and gross margins than Jinong’s liquid and concentrated powder fertilizers. Gufeng’s fiscal 2014 gross profit accounted for 23% of CGA’s total gross profit, as Gufeng’s gross profit margin was only 19% versus 59% for Jinong (calculated from the 2014 10-K). Both J Capital and Alfred Little alleged that CGA overpaid for Gufeng’s low-margin business, which CGA claimed it turned around, increasing Gufeng’s average selling prices from $288 per ton in the quarter following the acquisition to over $400 per ton each of the last few years.

The following satellite image taken November 13, 2013 is marked up showing the Gufeng factory and the location of the factory entrances and cameras we deployed along the main access road to the Gufeng factory. Our effort to film the Gufeng factory was hindered by a security guard Gufeng had stationed at the intersection of the factory access road and the main highway which repeatedly prevented us from approaching the factory:

Note: All trucking traffic we observed followed the yellow dashed route. The small dirt road heading southwest from “Entrance 2” appears to only be used by locals, including a neighboring greenhouse complex (which may possibly be a small customer).

Below are sample images from our two cameras:

Camera 1 view of Entrance 1

Camera 2 view of the Access Road to the Gufeng Factory:

During the 51 days we filmed, based on CGA’s quarterly SEC filings, we estimated that Gufeng should have sold around 760 tons of fertilizer per day on average. However, our surveillance footage only recorded shipments of 500 (low estimate) to 580 (high estimate) tons per day, a 24% to 34% shortfall.

We compiled one week of sample time-lapse videos spanning April 1 to April 7, 2013 that can be viewed by clicking the thumbnails below:

|

|

|

| 4/1/2013 | 4/2/2013 | 4/3/2013 |

|

|

|

| 4/4/2013 | 4/5/2013 | 4/6/2013 |

|

||

| 4/7/2013 |

CGA Refuses to Respond to Inquiries Regarding its Fertilizer Production

One of our investigators first reached out on September 12, 2014 to try to arrange a call with CGA’s CFO, Ken Ren, to discuss these issues. The investigator called Ken’s U.S. phone number (530-220-3026) disclosed in CGA’s SEC filings.

Mr. Ren answered his phone but refused to even acknowledge that he was Ken Ren, CGA’s CFO. Mr. Ren hung up on the investigator. On a second call, Mr. Ren again would not confirm his identity but referred the investigator to contact the person shown on CGA’s most recent press releases, Mr. Fang Wang.

One of our investigators then emailed Mr. Wang but never received a reply.

On September 30th Dan David, Principle in GeoInvesting called Mr. Ren and emailed both Mr. Ren & Mr. Wang one last time to confront them, receiving no answer to either his call or email.

After receiving no reply from management, Dan spoke to a long time investor in CGA who was able to reach Ken Ren. This long time investor called Dan late on September 30, 2014 to inform Dan that Ken Ren could not reach Li Tao but Ken would email or call Dan to set up a conference call immediately. This call never came. Rather, today, CGA issued a press release announcing a “first ever dividend”.

Today, aware of the rising short interest in its stock and less than a day after our final attempt to confront management, CGA announced a one-time dividend of 10c per share ($3.3 million in aggregate), payable four months from now. We doubt that CGA has the capability or desire to actually pay this dividend. CGA’s dividend announcement reminds us of China Media Express (CCME), which announced a dividend policy following a short seller’s report calling the company a fraud. CCME never paid.

Our Findings Cannot be Reconciled with CGA’s Public Filings

We thought about some potential reasons for the nearly 10x shortfall of production activity at the Jinong factory. One such reason we thought could be that the missing Jinong “sales” are actually just wholesale trades in fertilizer products, or outsourced production, rather than sales of fertilizer manufactured by Jinong. But we easily concluded that such a claim would be preposterous and clearly contradicted by CGA’s historical SEC filings, including the 2014 10-K which discloses on page 12 that CGA both “produced and sold” its entire 316,450 metric tons of fertilizer sold in fiscal 2014 (according to the table at the top of page 50). Hence, we believe that no material amount of production was outsourced to 3rd parties.

The following Q&A exchange from the Q3 2014 earnings conference call transcript further ruled out an “outsourcing” explanation:

“Bill Whitfield: Thank you. Now do you produce 100% of the fertilizers you sale or do you outsource or subcontract any of your production?

Li Tao: Except the number of fertilizer products, we almost surely produce our fertilizer products ourselves. Roughly 1%.

…

Bill Whitfield: So, roughly 1% okay. And so what percent of your sales are your own products that you can produce and if you tell that number?

Li Tao: Most of the products which is produced by ourselves.

Bill Whitfield: Okay. Is there anyway to get a percentage on that to quantify that?

Li Tao: Like we said approximately 1% as I say from the outsourcing parties and the rest will be produced by companies owned.”

Then, we considered whether the missing 90% of Jinong’s fertilizer sales could actually be giant intercompany cross-sales of fertilizer manufactured at CGA’s Gufeng facility. This reasoning would mean that CGA is asking us and investors to believe that its fully automated Jinong liquid organic factory, built in part with funds raised directly from U.S. investors, has hardly produced any fertilizer at all in the last year.

We discard this possibility for the following reasons:

- The Jinong factory is CGA’s only factory capable of producing CGA’s premium liquid organic fertilizers that are CGA’s highest margin product, with average selling prices of well over $2,000 per ton ($2 to $3 per liter retail price for the basic liquid fertilizer shown on Alibaba.com)

- According to the 10-K, Jinong sold 60,629 metric tons of fertilizer for an average of $1,941 per ton, over 4x the average selling price of fertilizer sold by Gufeng. To achieve such a high average selling price, much of the fertilizer Jinong sold must be expensive liquid organic fertilizer that can only be manufactured at Jinong’s factory

- Our time-lapse data showed that the Gufeng factory shipped out less fertilizer than the sales volumes reported in CGA’s SEC filings. If Gufeng was producing large volumes of fertilizer for Jinong, our cameras filming Gufeng should have recorded higher, rather than lower volumes

- CGA’s audited financials do not disclose any material intercompany sales, which should appear in “Note 13 – Segment Reporting” of the fiscal 2014 10-K

- Historically (through fiscal 2011), CGA reported each Jinong’s capacity utilization as tons sold divided by Jinong’s annual production capacity of 55,000 tons. Thus at least through 2011, when CGA reported “tons sold” the amount was the same as “tons produced” for Jinong

CGA’s Vanishing Cash and PP&E Reclassification Justifies a Delisting on its Own

CGA has conducted a series of highly questionable, if not outright fraudulent transactions that diverted nearly all of the company’s cash to questionable marketing ventures. In all of our years of experience in the market, we’re hard pressed to come up with a situation as absurd and alarming as this one.

As shown in the following table, in 2012 and 2013, CGA reported it invested $44,333,172 in Property, Plant, and Equipment (PP&E):

| 2012 | 2013 | Total | |

| Originally Reported Investment in PP&E | ($11,883,947) | ($32,449,225) | ($44,333,172) |

| Revised Investment in PP&E | ($2,532,385) | ($529,505) | ($3,061,890) |

| Investment in PP&E Reclassified to Marketing Related Deferred Assets | ($9,351,562) | ($31,919,720) | ($41,271,282) |

Source: 2013 and 2014 10-K

Note: $67,357 invested in construction in progress in 2013 is included in PP&E investment in our table above

However, as shown in the table above, in its 2014 10-K CGA reclassified $41,271,282 of its PP&E investments to “deferred assets” that the company vaguely describes as “marketing related assets” to be rapidly amortized and expensed over the next three years:

“The primary amounts reclassified were certain marketing related assets that were previously included in property, plant and equipment at June 30, 2013 that were reclassified to deferred assets.” (Page F-11 of 2014 10-K)

…

“Deferred assets represent amounts that the distributors owed to the Company in their marketing efforts and developing standard stores to expand the Company’s products’ competitiveness and market shares. The amount owed to the Company to assist its distributors will be expensed over three years which is the term as stated in the cooperation agreement, as long as the distributors are actively selling the Company’s products.” (Page F-8 of 2014 10-K)

Thus $41.3 million of the cash that CGA previously reported as invested in PP&E two years ago is now quickly going to be expensed as marketing related. This begs the question of whether this amount should have been classified as marketing related when first incurred and expensed much sooner, negating and calling into question much of CGA’s reported operating cash flow of $38,491,225 in fiscal 2012 and 2013.

Even more mind-boggling is the fact that in the last 12 months CGA invested an additional $72,061,705 of its cash in marketing related deferred assets, bringing the total “investment” in marketing to over $113 million in the last 3 years!

What has this outrageous three-year “investment” in marketing accomplished? Almost nothing, as far as sales growth shows:

| 2014 | 2013 | 2012 | |

| Net Sales | $233,402,088 | $216,897,956 | $217,524,205 |

From 2012 to 2014, sales grew about $16 million, or only 7%! CGA’s sales growth guidance for 2015 is 9% to 15%. Thus CGA’s top line sales growth is failing miserably to recoup its investments in marketing related assets. CGA’s marketing investments are simply wiping out cash and greatly reducing reported earnings.

The hit to earnings will get worse. For fiscal 2014, CGA amortized and expensed $27,390,957 of the marketing related deferred assets. For fiscal 2015, CGA estimates another $41,807,390 amortization expense of the deferred assets, far more than management’s sales growth forecast, resulting in a huge negative impact to earnings.

The huge cash outflow to marketing related deferred assets has virtually wiped out CGA’s reported cash position from $75,031,489 at June 30, 2013 to $26,890,321 at June 30, 2014. Subtracting $25,700,586 of customer deposits, leaves CGA with only $1,189,735.

We conclude that CGA’s reclassification of PP&E and purported investment of over $113 million in marketing related assets makes no sense given that such an enormous amount seems unlikely to ever be recouped from CGA’s limited growth in sales. We question whether any of this investment was real, or was it merely a way to move cash off of CGA’s balance sheet? Did this cash even exist in the first place?

Now Let Us Tell You What You Already Know

The irony behind GeoInvesting publishing this piece on what we believe to be another brazen China hustle is the fact that we were such bulls on China in 2009. If you go back to our articles throughout 2009, you can see that we were once bullish on names like CGA and LLEN. We were bullish on China’s economic stimulus in general.

U.S. listed Chinese companies are intricate cases, cloaked by a significant language barrier, murky disclosures and inaccessibility due to geography. It is much more difficult for U.S. based investors to perform due diligence in China than it is for them to do so domestically, a fact that Chinese companies understand.

Once we established our own on-the-ground due diligence team in China, our assessment of U.S. listed Chinese companies was diametrically opposed to our previous sentiments. Our intentions from the beginning have always been solely driven by our desire to learn the truth, good or bad, and we’ve found indisputable overwhelming evidence of fraud in China-based companies since we’ve begun doing our on-the-ground research there (see names like Longwei Petroleum (LPIH), Sino Clean Energy (SCEI), Yuhe Int`l (YUII), Puda Coal (PUDA) and more recently L&L Energy Common and FAB Universal (FABU). PUDA, YUII and FABU eventually admitted to their deceit. Further, the Chinese press validated our findings pertaining to SCEI, LLEN, LPIH and FABU.

We’ve come to expect some initial skepticism and pushback to our reports. We understand the reasons why investors do this and we welcome it, as we know our reports are backed by primary source on-the-ground evidence. In the case of CGA, we offer indisputable time-lapse video surveillance of the Jinong factory, conducted over a period of one year that simply speaks for itself. Once again we hope our readers can use the evidence to make better investment decisions in the future.

As usual, we are submitting all of our evidence to the NYSE and SEC. Based on our investigation, we see no way that CGA can survive as a listed company.

We’ll also offer to present our evidence to CGA’s auditor, Kabani & Company. However, Kabani showed no interest in reviewing our evidence on L&L Energy , the last Kabani audited fraud we exposed. In fact, Kabani only stopped providing positive audit opinions for LLEN after LLEN stopped paying them and after LLEN’s CEO Dickson Lee was arrested and charged with fraud (Lee recently pled guilty to two counts of fraud).

In his 1990 Letter to Shareholders, Warren Buffett warned:

” The term “earnings” has a precise ring to it. And when an earnings figure is accompanied by an unqualified auditor’s certificate, a naive reader might think it comparable in certitude to pi, calculated to dozens of decimal places.

In reality, however, earnings can be as pliable as putty when a charlatan heads the company reporting them.”

Disclosure: Short CGA

Disclaimer:

You agree that you shall not republish or redistribute in any medium any information on the GeoInvesting website without our express written authorization. You acknowledge that GeoInvesting is not registered as an exchange, broker-dealer or investment advisor under any federal or state securities laws, and that GeoInvesting has not provided you with any individualized investment advice or information. Nothing in the website should be construed to be an offer or sale of any security. You should consult your financial advisor before making any investment decision or engaging in any securities transaction as investing in any securities mentioned in the website may or may not be suitable to you or for your particular circumstances. GeoInvesting, its affiliates, and the third party information providers providing content to the website may hold short positions, long positions or options in securities mentioned in the website and related documents and otherwise may effect purchase or sale transactions in such securities.

GeoInvesting, its affiliates, and the information providers make no warranties, express or implied, as to the accuracy, adequacy or completeness of any of the information contained in the website. All such materials are provided to you on an ‘as is’ basis, without any warranties as to merchantability or fitness neither for a particular purpose or use nor with respect to the results which may be obtained from the use of such materials. GeoInvesting, its affiliates, and the information providers shall have no responsibility or liability for any errors or omissions nor shall they be liable for any damages, whether direct or indirect, special or consequential even if they have been advised of the possibility of such damages. In no event shall the liability of GeoInvesting, any of its affiliates, or the information providers pursuant to any cause of action, whether in contract, tort, or otherwise exceed the fee paid by you for access to such materials in the month in which such cause of action is alleged to have arisen. Furthermore, GeoInvesting shall have no responsibility or liability for delays or failures due to circumstances beyond its control.