Summary

- GeoInvesting blows the lid off of the MGT Capital Investments promotional circus and encourages the SEC to investigate all parties involved, including stock promoters paid by MGT

- Calls to the company on 5/25 were not returned because they were greeted by a recorded line stating “you have reached a number that is not currently set up to take calls.”

- We think McAfee’s involvement is hardly the beacon of hope that MGT is making it out to be. As far as we can tell, McAfee had little (or nothing) to do with the sale of McAfee to Intel

- Two MGT investors have extremely suspect backgrounds, have been outed in several pump and dump articles prior, and we believe are signs of a coming stock dump

- “Management consultants” were paid by MGT for the stock price rising above $1.00 and $2.00, as detailed in the company’s May 9, 2016 8-K referenced herein

The Circus Needs to Stop

First and foremost, we want to comment that there was no MGT available to short. Before we are accused of writing this simply for being short, we want to make that abundantly clear. If we had the opportunity, we would have shorted shares aggressively, but we still think that despite not having a position, this information will be extremely beneficial to the investment public and SEC for portfolio protection and regulation purposes.

By the way, even though we are not short, there is a case that draws the conclusion that the CEO could be selling his stock into a company funded paid promotion.

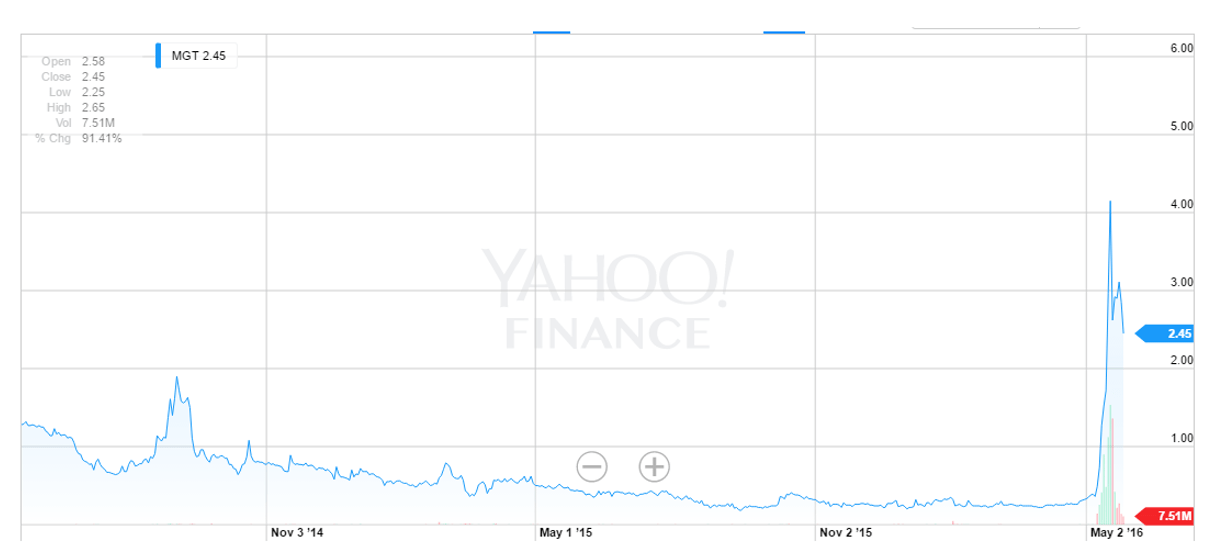

It has been hard to ignore the circus around MGT Capital Investments (MGT) over the last 3 weeks. The well recognized name of John McAfee, combined with the stock purchases of strategic “investors” has caused a spike in the stock — a spike that already appears to be on its way down.

This is stock spike that, based on the facts as we see them, should not only end, but should be investigated by the Securities and Exchange Commission.

Trading volume in MGT has gone from a paltry couple thousand shares a day to millions of shares per minute now that the market has digested news of John McAfee’s involvement, combined with new investors and a new business model for the company. We believe this run up, however, is a result of an orchestrated effort by two seasoned “investors” who have run this play book in the past. We also believe McAfee’s involvement in the company is hardly as important as long investors would like to think.

To the untrained eye, such price action might be explained away with the simple notion that announcing a contingent asset purchase agreement for a free app along with a consulting agreement with a relatively unknown company and a proposed appointment of a future CEO should cause more than a billion dollars to trade hands inside 3 weeks while sending the price of the target stock up by more than 1,500%. We suppose that is one possible scenario.

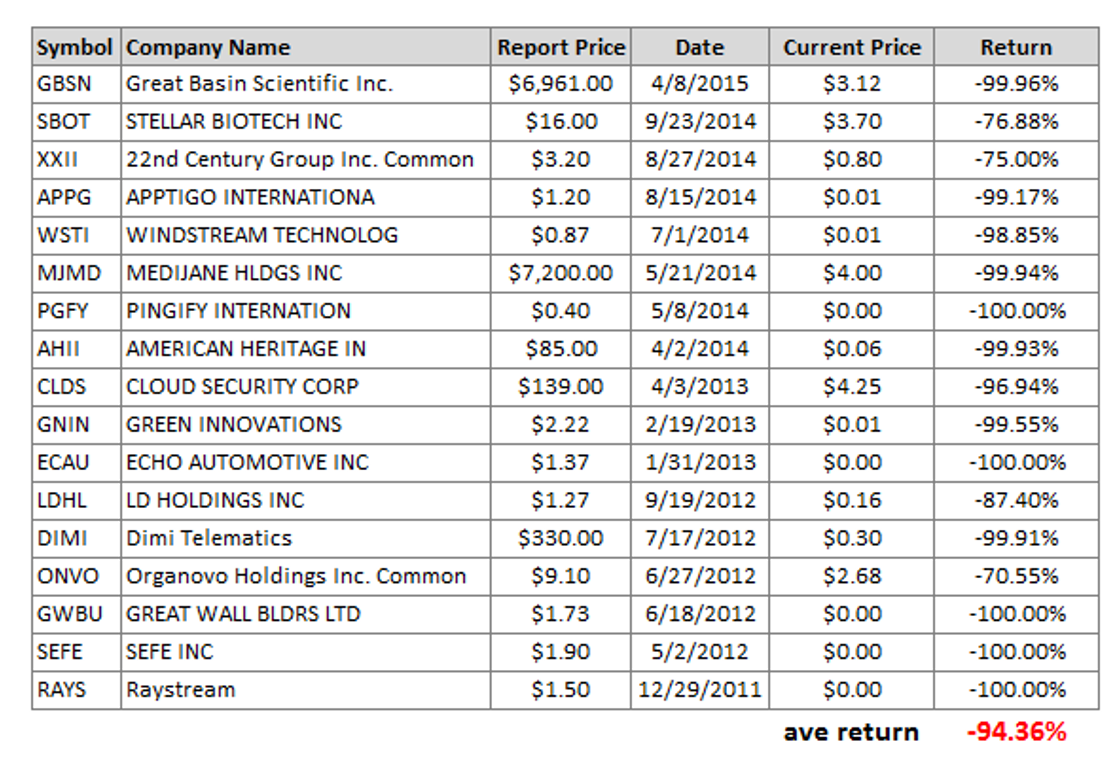

But GeoInvesting’s experience with pump and dumps runs far and wide, and the players and circumstances involved with MGT lead us to believe this stock pump could end in an ugly fashion. This is hardly the first of these situations we’ve written about. In fact, between 2011 and 2015 we published articles on 17 pump and dumps. The average subsequent decline was over 90% over the course of the long term, with many stocks succumbing to an immediate downward reaction in price. As seen below, every stock eventually plummeted, destroying shareholder wealth.

Geo founder Maj Soueidan recently commented on his personal blog about about a firm promoting MGT that blatantly admits it is in the business of “touting” stocks for compensation. In this article, we cite several entities and an 8-K that admit through disclaimers that MGT is compensating them for what we deem as promotion.

GeoInvesting Pump and Dump Report Returns

Our latest pump and dump article, published on AVXL on May 2, has already netted gains of 16% for those who shorted the equity around $5.05. We think in time, just like with AVXL and our other pump and dump stories, MGT will “dump” and retail shareholders will be left holding the bag of investors like Michael Brauser and Barry Honig. The short game has been undoubtedly tough over the last few years, but the “pump and dump” short well never seems to run dry.

Not only are we convinced that this move is unwarranted, we believe that the SEC needs to step in and look at not only the players involved, but the manner with which some of these transactions took place.

Why Should the SEC Step In?

First things first — on 5/25/16, we tried to reach MGT at the number provided on their contact page.

This is also the number they list on some SEC filings. Instead of eager workers, excited to be part of a new project set for unencumbered success, we got the following electronically voiced message:

“You have reached a number that is not currently set up to take calls.”

Not a great start for our due diligence into MGT. We encourage you to phone the company at the same number and, if greeted with a person, inquire to them as to why the phone lines weren’t set up 16 days after making “earth shattering” announcements about their business.

Now, let’s canvas the chain of MGT events as they’ve occurred over the past couple weeks. On May 9th, MGT put out the following press release that started it all. The “big money” lines were as follows:

“In conjunction with the acquisition, MGT is pleased to announce the proposed appointment of John McAfee as Executive Chairman and Chief Executive Officer. Mr. McAfee, the visionary pioneer of internet security, sold his anti-virus company to Intel for $7.6 billion, and is actively involved in the development of new measures to protect individual freedoms and privacy.”

What’s not to love — visionary founder with track record of selling a $7.6 billion company? Not quite.

We immediately take issue with a couple points of this release:

- Potential investors are tasked with making investment decisions based on this language.

- However, the press release mentions a proposed appointment that hasn’t even taken place yet. McAfee was not executive chairman or Chief Executive Office at the time of the announcement.

- It throws around a $7.6 billion number that prospective investors might hang onto, despite us believing this statement is misleading. We’ll explain why.

That press release was attached to the following 8-K that was filed with the Securities and Exchange Commission. Among other things, this May 9th 8-K provides language on bonuses for management consultant Future Tense Secure Systems, Inc. if the stock gets pushed over certain levels (hereinafter referred to by Geo as “the stock pump bonus”).

-

Value Bonuses. If, during the first twelve (12) months of the initial Term of this Agreement, the volume weighted average price (“VWAP”) of the Company’s common stock is equal to or greater than $1.00 for each of ten (10) consecutive trading days on the NYSE MKT exchange, then Consultant shall be entitled to receive a cash bonus in the amount of $250,000 to paid within thirty (30) days of such triggering event. If, during the first twelve (12) months of the initial Term of this Agreement, the VWAP of the Company’s common stock is equal to or greater than $2.00 for each of ten (10) consecutive trading days on the NYSE MKT exchange, then Consultant shall be entitled to receive an additional cash bonus in the amount of $350,000 to paid within thirty (30) days of such triggering event.

These press releases claim that McAfee was the guy who got his company sold to Intel for billions, but it seems to us that McAfee really didn’t have much (if anything) to do with McAfee, Inc. when the sale announcement was made on August 18, 2010.

It is true that John McAfee founded the original McAfee Associates in the late 1980’s. However, it is also true that McAfee Associates changed names to Network Associates nearly 20 years ago, and part of the assets were spun off as McAfee.com in 1999. While Network Associates did change their name back to McAfee, Inc in 2007, to suggest that John McAfee started a small company (similar to what MGT is today) and then built that company to a point that it could be sold for $7.6 billion decades later is to suggest that this is a track record that could be duplicated. Investors relying upon this information (and there is plenty of social media chatter out there to suggest that people are relying upon that information) could be making an investment decision based on a misrepresentation of facts as presented by MGT.

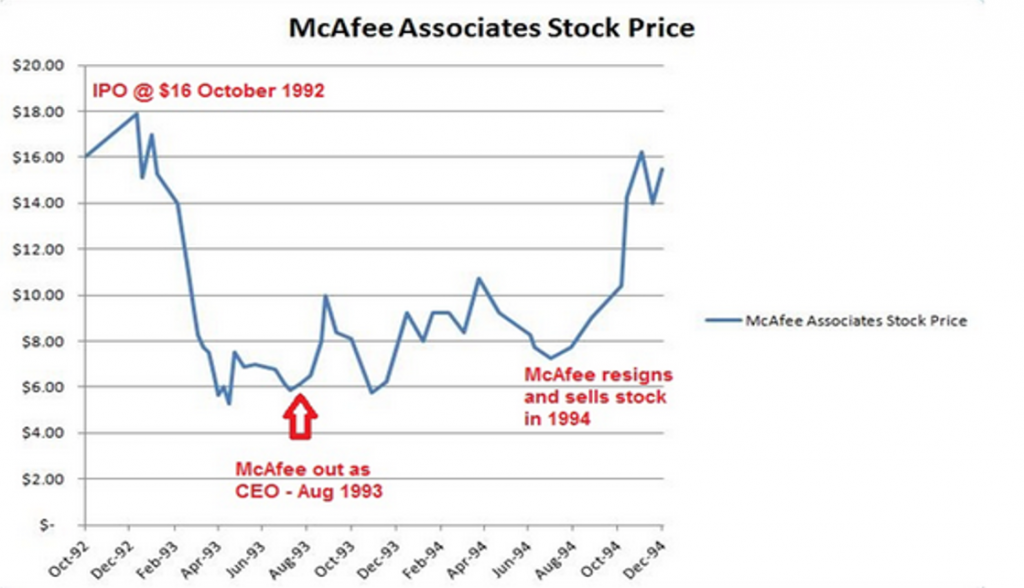

To prove this point, let’s take a trip back in time. It is October 1992, and McAfee Associates is coming off the heels of a spike in sales due in part to John McAfee’s hyping of the Michelangelo virus — he said it could affect up to 5 million PC’s, but stories show that the virus only affected 20,000 to 40,000 systems.

The IPO was to be at $16, a price that would make CEO McAfee a rich man. However, it took only a few months after the IPO for McAfee Associates to realize that John McAfee’s personality might not be the right fit for a public company, a theme our research will re-visit in due time.

Here is an old periodical clipping that narrates what happened around August 1993:

Now removed from his CEO position, it did not take John McAfee very long to cash out of his remaining shares of McAfee Associates. He gave an interview to a New York Times reporter in 2009, who explained:

“Mr. McAfee is, by his own description, an atypical businessman – easily bored and given to serial obsessions. As a young man, he traveled through Mexico, India and Nepal and, more recently, he wrote a book called, “Into the Heart of Truth: The Spirit of Relational Yoga.” Two years after McAfee Associates went public, he was bored again. So he sold his remaining stake, bringing his gains to about $100 million.”

The same article from 2009 notes that in 2007, McAfee later found himself, according to his own words, “broke”:

In 2007, Mr. McAfee sold a 10,000-square-foot home in Colorado with a view of Pike’s Peak. He had spent $25 million to buy the property and build the house. He received $5.7 million for it. When Lehman collapsed last fall, its bonds became virtually worthless. Mr. McAfee’s stock investments cost him millions more.

One day, he realized, as he said, “Whoa, my cash is gone.”

His remaining net worth of about $4 million makes him vastly wealthier than most Americans, of course. But he has nonetheless found himself needing cash and desperately trying to reduce his monthly expenses.

He has sold a 10-passenger Cessna jet and now flies coach. This week his 5.34-acre oceanfront estate in Hawaii sold for $1.5 million, with only a handful of bidders at the auction. He plans to spend much of his time in Belize, in part because of more favorable taxes there.

Next week, his New Mexico property will be the subject of a no-floor auction, meaning that Mr. McAfee has promised to accept the top bid, no matter how low it is.

“I am trying to face up to the reality here that the auction may bring next to nothing,” he said.

In the past, when his stock investments did poorly, he sold real estate and replenished his cash. This time, that has not been an option.

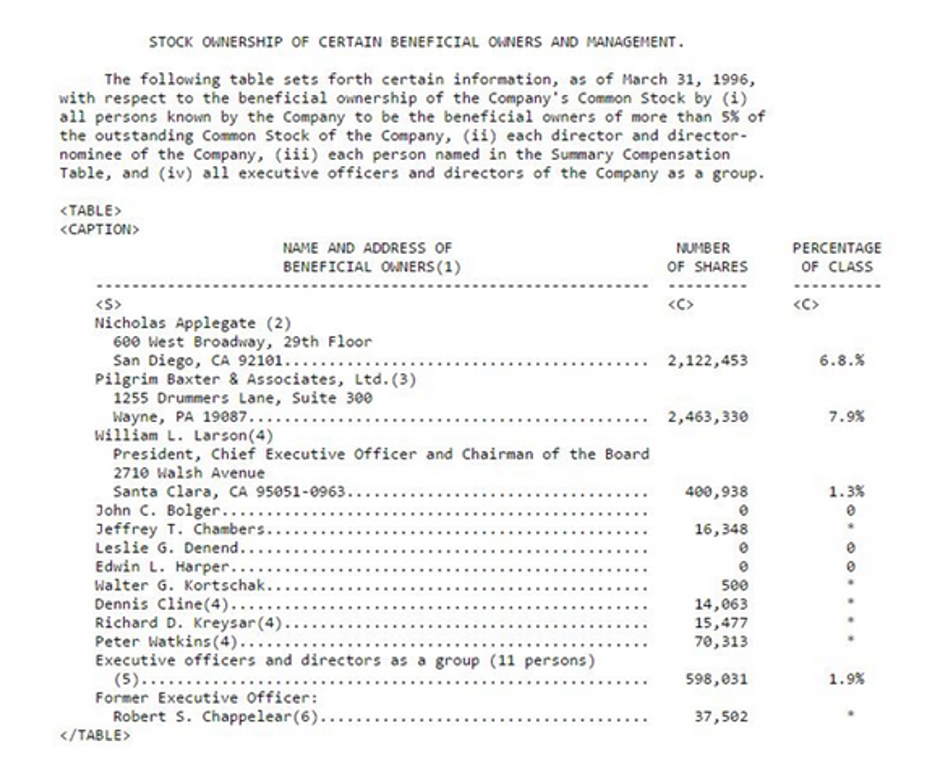

Going a step further down the rabbit hole, just to be sure that the NY Times wasn’t just taking his word for it, we dug up the filing for the annual shareholder meeting for McAfee Associates that took place in 1996. In it, not in the 10-K, is where you will find the list of beneficial owners:

John McAfee is not on the list.

This data seems to suggest that John McAfee sold his stake and resigned from McAfee Associates some 16 years prior to the date that Intel announced it would be acquiring McAfee, Inc. This fact was brought up on social media, and was more than likely seen and analyzed by MGT’s legal team. We say this because MGT just filed a 10-Q, which holds a newly worded statement regarding McAfee and Intel that differs markedly from the previous statement made in the 8-K filing:

The language from the 8-K previously stated:

“Mr. McAfee, the visionary pioneer of internet security, sold his anti-virus company to Intel for $7.6 billion.”

But the 10-Q now states:

“He founded McAfee Associates in 1987, which was acquired by Intel Corporation for $7.6 billion in 2010.”

The difference means everything — here’s another look:

“McAfee (subject) sold (verb) his (ownership) company”

Compared to…

“McAfee (subject remains the same) founded (verb change) a company, and that company was later sold (omission of ownership).”

The fact that MGT’s legal department went out of their way to change what looks like a few nuanced details says it all. GeoInvesting has analysts that have worked with PR and IR professionals alongside securities lawyers in drafting these documents — take it from us, these changes are made for very specific reasons and words are chosen very carefully.

Now that it appears that John McAfee had neither ownership of stock nor a seat on the board for the 15+ years leading up to Intel’s acquisition of McAfee, Inc., let’s take a look at the performance of McAfee Associates during his stint at the company.

The IPO occurred in October 1992. There are no charts that can be generated on the Internet dating back that far. Luckily, we found a chart posted on the Internet that used closing price print material from financial periodicals during that time. Annotations had been added, which we found to also be material.

Why do we believe the annotations are material?

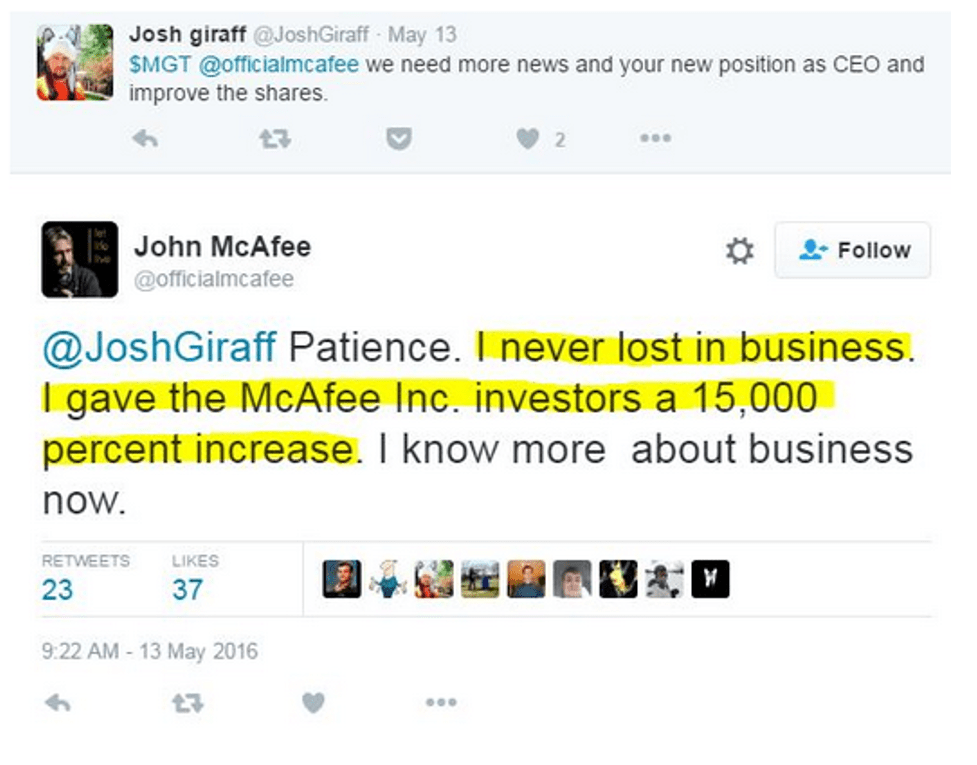

Well, it seems that John McAfee, or someone pretending very well to be John McAfee, has been making public comments about John McAfee’s past performance. Here is an example:

Obviously, the comment “I never lost in a business” doesn’t seem to reconcile well with McAfee’s tenure at McAfee Associates, where the stock plunged from near $16 to $6 under his watchful eye, prior to him leaving the company.

We just showed that John McAfee seemingly had little to nothing to do with McAfee, Inc.’s positive performance leading up to its buyout. In fact, the performance of McAfee Associates from IPO through 1993 (when McAfee departed as CEO) actually under-performed the benchmark average of the NASDAQ. So, for this “John McAfee” on Twitter to state that he produced a 15,000% return for McAfee, Inc. investors is highly questionable.

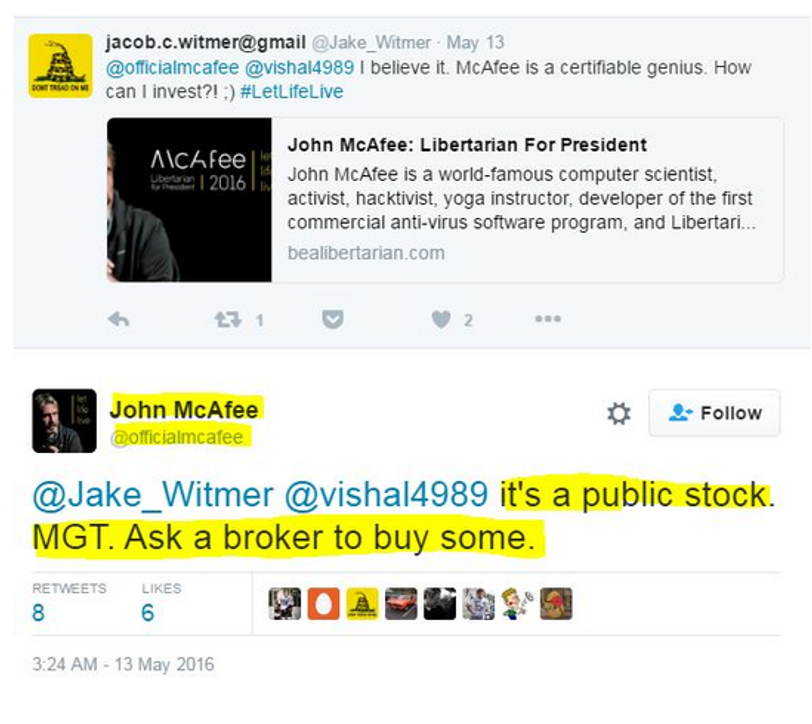

Moreover, we are not sure if it is legal for an incoming CEO to make a public comment like this. While we might be unsure of that comment, we are quite certain that an incoming CEO should not be making a public statement where he instructs potential investors to purchase stock in the target company, like it appears McAfee does here:

At this point, let’s take a breather and pretend that we are drawing a picture for the SEC:

- Unusual volume

- Price volatility

- A PR and 8-K with what appear to be materially misrepresented information

- An incoming CEO that appears to be on social media instructing people to buy the stock and making questionable comments about his past

Moving forward, what would make all of this especially relevant from the standpoint of a potential stock halt? More stock promotion, of course.

The same day that the May 9th PR came out, there was also an email blast that apparently went out from a promoter by the name of StockBeast.com. If you want to know who allegedly paid for this stock promotion, then look closely at their disclaimer:

MGT was also promoted by the SCS, LLC network (OTCBB Journal, Small Cap Traders, etc ). A close look at their disclaimer:

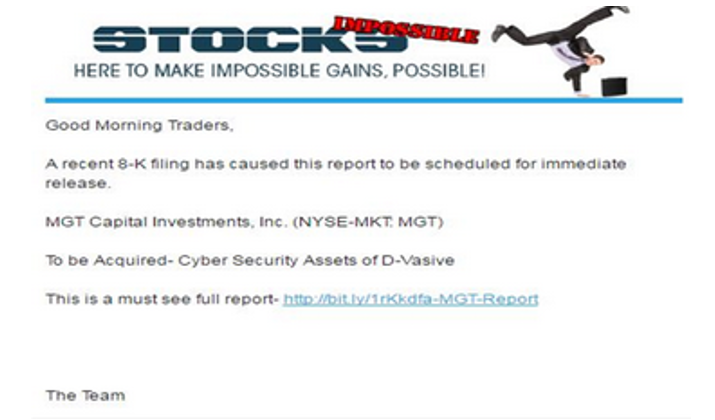

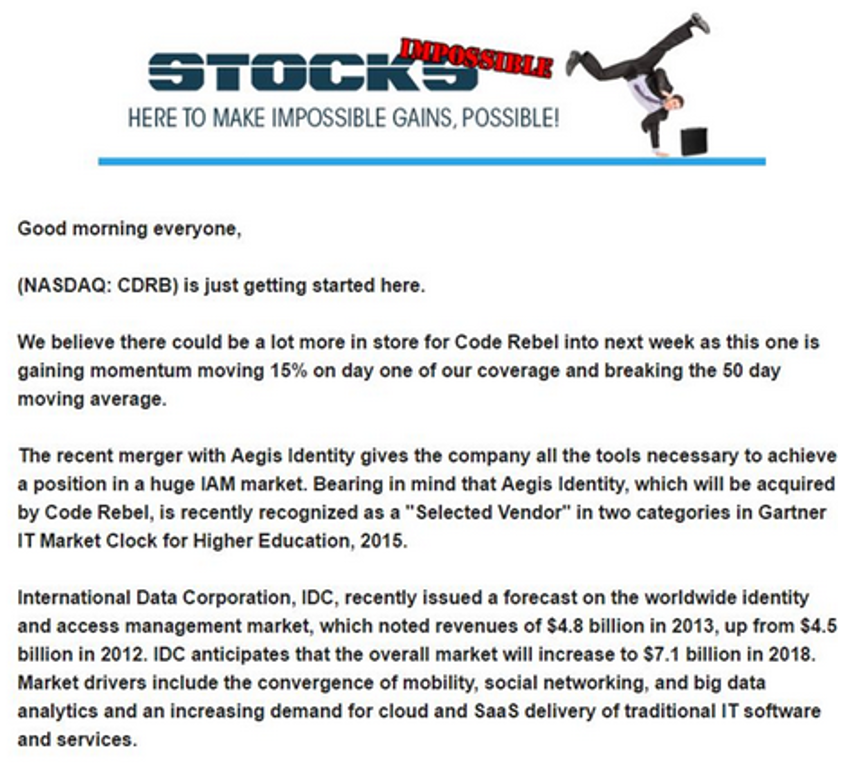

Also part of the SCS network is Stocks Impossible. It appears that they, too, sent out some blasts on MGT:

Their hyperlink now sends you to a PDF that is no longer available.

Why are we dwelling on Stocks Impossible and the SCS network? You might remember some of their recent handiwork, Code Rebel (CDRB), which was recently the subject of an SEC halt. Here is what could be one of several pump jobs of CDRB by Stocks Impossible:

Why on earth would anyone need to pump Code Rebel stock? If you really want to read why, then we defer to the wonderful team over at IBankCoin and their report on CDRB.

This all then begs the question that if the news is so great, then why are people and the company, itself, paying these tout groups to pump the stock of MGT in similar fashion to CDRB?

Our SEC halt checklist now looks like:

- Unusual volume

- Price volatility

- A PR and 8-K with what appear to be materially misrepresented information

- An incoming CEO that appears to be on social media instructing people to buy the stock and making questionable comments about his past

- Possible paid stock promotions funded by the company, and another paid for by “DF Media”

“Why should we care if the company paid for the stock promotion?”, you might ask. “There could be a logical explanation for that, too!”

To understand why a company might pay for this stock promotion, we need only go back to some old SEC filings. Namely, an 8-K from October 2015. It is here that you will find that MGT sold stock at 25 cents, and attached 2 warrants to each unit at an exercise price of a quarter:

On October 8, 2015, MGT Capital Investments, Inc. (the “Company”) entered into separate subscription agreements (the “Subscription Agreement”) with accredited investors (the “Investors”) relating to the issuance and sale of $700,000 of units (the “Units”) at a purchase price of $0.25 per Unit, with each Unit consisting of one share (the “Shares”) of the Company’s common stock, par value $0.001 per share (the “Common Stock”) and a three year warrant (the “Warrants”) to purchase two shares of Common Stock at an initial exercise price of $0.25 per share (such sale and issuance, the “Private Placement”).

The document goes on to explain that these warrants can be exercised via a cashless option, an option that would allow the investors to receive what would be essentially free stock in the future:

The Warrants may be exercised by means of a “cashless exercise” following the four month anniversary of the date of issue, provided that the Company has consummated a Qualifying Transaction and there is no effective registration statement registering the resale of the shares of Common Stock underlying the Warrants (the “Warrant Shares”).

Later in the document, we see that a man named Barry Honig was the Lead Investor:

“The investment was led by Barry Honig, a private investor and a specialist in corporate finance.”

The shares were subsequently registered and that registration statement was declared effective – 2.8 million shares for the initial investment plus 5.6 million more via the warrants, for a grand total of 8,400,000 brand new shares.

We will not get into the reverse split that took place in 2012, and the subsequent dilution that has come since then. But, there is another heap of shares that are unaccounted for as they have all gone to people under the 5% rule.

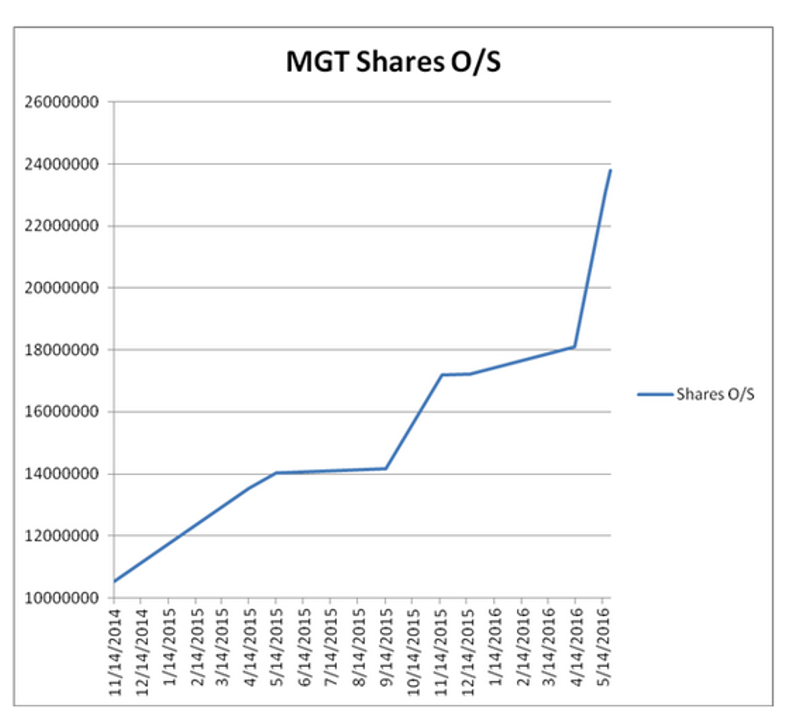

Next, we will take a look at the outstanding share count of MGT stock over the past 18 months or so:

As you can see, the printing press was conveniently turned on a couple weeks prior to the May 9th press release. Also, in the 6 months leading up to the stock promotion, MGT diluted its shareholders to the tune of roughly 68% – Increasing the shares outstanding from 14.157 million in September 2015 to 23.798 million in May 2016. This chart does not count a coming 20M share increase that will now also happen as a result of an acquisition announced this morning. We will comment more on that later.

This is where the train begins to derail.

During this stock promotion campaign, possibly paid for by the company, a 424b3 filing was made that showed Barry Honig as a selling stockholder – The same Barry Honig who was the Lead Investor in a sizeable transaction just 7 months prior.

Note the following:

- According to this 10-K, MGT had only $359,000 in cash on December 31, 2015.

- According to this 10-Q, MGT had only $189,000 in cash on March 31, 2016.

Also in the 10-Q are these two statements:

“In May 2016, the Company issued 5,280,296 shares of common stock in connection with exercise of warrants, resulting in gross proceeds of $2.2 million.”

“Subsequent to March 31, 2016, and through the date of filing the Quarterly Report on Form 10—Q, the Company granted and issued a total of 430,000 shares to non—employees for services rendered. The shares were recorded at $718 using the closing market value on respective dates of issuance.”

This begs the questions:

1) Who got those 430,000 shares and what did they do for MGT in exchange for payment of stock which, at the time, represented more than 3% of the entire company?! Why would MGT give away more than 3% of their company to a non-employee for “services rendered”?

2) If the company was close to being out of money in March 2016, and if warrants were exercised and money was given to the company in May 2016, and the company used money to pay for a stock promotion in May 2016, and the original holders of the warrants are dumping stock into the paid promotion in May 2016, then what is really going on here?

Making matters possibly worse is this 144 filing that was made by MGT’s CEO, who might be getting in on the stock selling action:

LADD ROBERT B, Chief Executive Officer of MGT Capital Investments Inc [MGT], filed a Form 144 on May 13, 2016 with the Securities and Exchange Commission proposing to sell restricted securities: Approximate Date Of Sale Shares Broker 5/30/16 382,863 TD Ameritrade Prior to the sale of restricted stock, owners must file a Form 144 with the SEC. Upon submission of the filing to the SEC the owner is permitted to sell the shares, or any fraction thereof, within 90 days

Is the CEO really dumping stock into a promotion for which he is authorizing the company to pay? More importantly, did he recently print more shares for himself? According to the latest 10-K filing, as of April 11, 2016:

Mr. Ladd owns 273,603 shares of Common stock directly. Mr. Ladd may also be deemed to be the beneficial owner of an additional 622,471 shares of Common stock held by Laddcap Value Partners III LLC, a Delaware limited liability company (“Laddcap”), by virtue of his ability to vote or control the vote or dispose or control the disposition of the shares of Common stock held by Laddcap through his position as Managing Member of Laddcap.

Could his 144 be covering shares that he controlled via Laddcap Value Partners III, LLC, even though the 144 did not name that account directly? If that 144 was not covering shares held in the name of his LLC, then it appears as if Robert Ladd somehow acquired almost 110,000 shares in the past month, and that those shares could be part of that 144 filing.

Wait, it might get worse.

MGT, the sports-betting-company-going-Internet-Security-company decided to use the proceeds from those warrants to buy part of biotech company, Venaxis, Inc. – because that’s what you do when you are about to become an Internet security company. You might think a move like this makes no sense until you realize that it just so happens that both Barry Honig and MGT CEO, Robert Ladd were significant holders of Venaxis prior to this investment made by MGT, which caused the price of Venaxis stock to gap up by more than 50% once the filing was made.

Running it back for the SEC yet again:

- Unusual volume

- Price volatility

- A PR and 8-K with what appear to be materially misrepresented information

- An incoming CEO that appears to be on social media instructing people to buy the stock and making questionable comments about his past

- Possible paid stock promotions funded by the company, and another paid for by “DF Media”

- Warrants are exercised, money is paid to the company, shares are printed, and stock is possibly dumped by those who provided funding to the company and by the CEO, himself, into the stock promotion

- Company appears to use proceeds from the exercise of warrants to purchase stock in a company in which both the Lead Investor and the CEO had a vested interest

What has happened to MGT stock since the promotion began? Interestingly, the price and volume of MGT stock began to creep up a few days prior to the pump’s beginning. Coincidentally, this action began around the time that StockBeast.com would have been getting wind that they would receive payment to promote the stock.

Once the promotion kicked off, however, the real fireworks began. MGT went from roughly 30 cents to $5.58 in a matter of weeks, trading more shares in minutes than it had traded in an entire year. Then, in Awesome-Penny-Stock-Zero-Bid-Implosion-Fashion, shares of MGT fell from $4.90 to $2.65 inside 25 minutes. All of this, on a deal that has yet to be consummated – a deal that, in GeoInvesting’s opinion, stands on very shaky ground.

Finally, on May 26, 2016, the company announced that it was making an acquisition of Demonsaw, LLC.

In addition to issuing even more stock:

“Major terms of the deal include the payment to Demonsaw LLC members of 20.0 million restricted shares of MGT common stock.”

Not-yet-CEO McAfee made the following extremely forward looking statement:

“As a listed company with proper corporate governance and regulatory standards, MGT will be the vehicle I use to create wealth for all stockholders.”

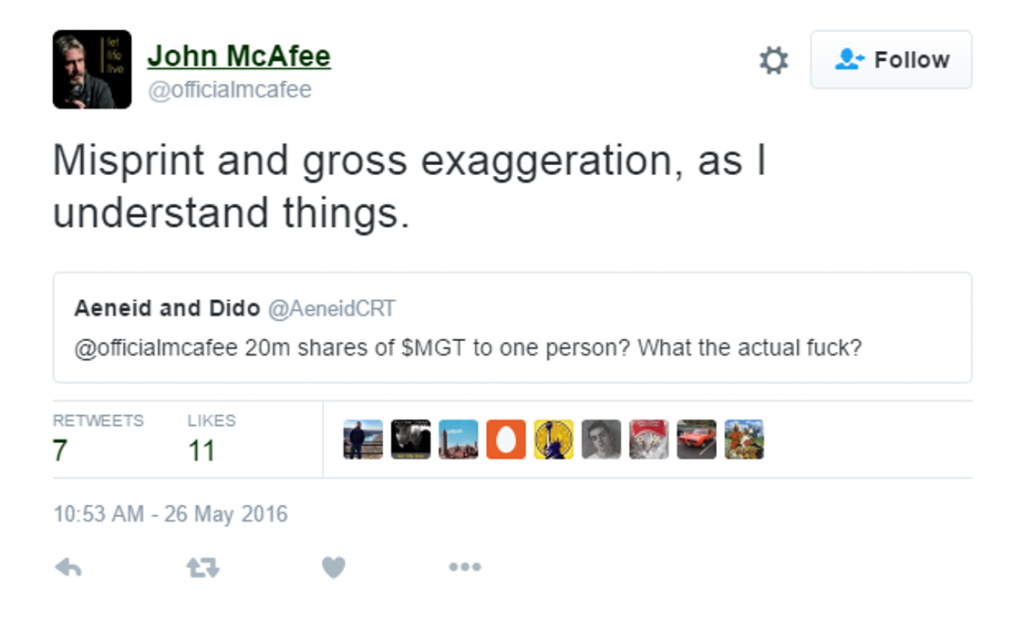

When McAfee was asked about this 20M share issuance on Twitter the day of the 8-K filing, it appears that he is telling the public that the 8-K is in error. He appears to call the MGT 8-K a “misprint and gross exaggeration”:

More to Come

We believe more acquisitions of former and failed McAfee ventures are going to be on their way.

This represents a small portion of what we’ve found during our initial due diligence.

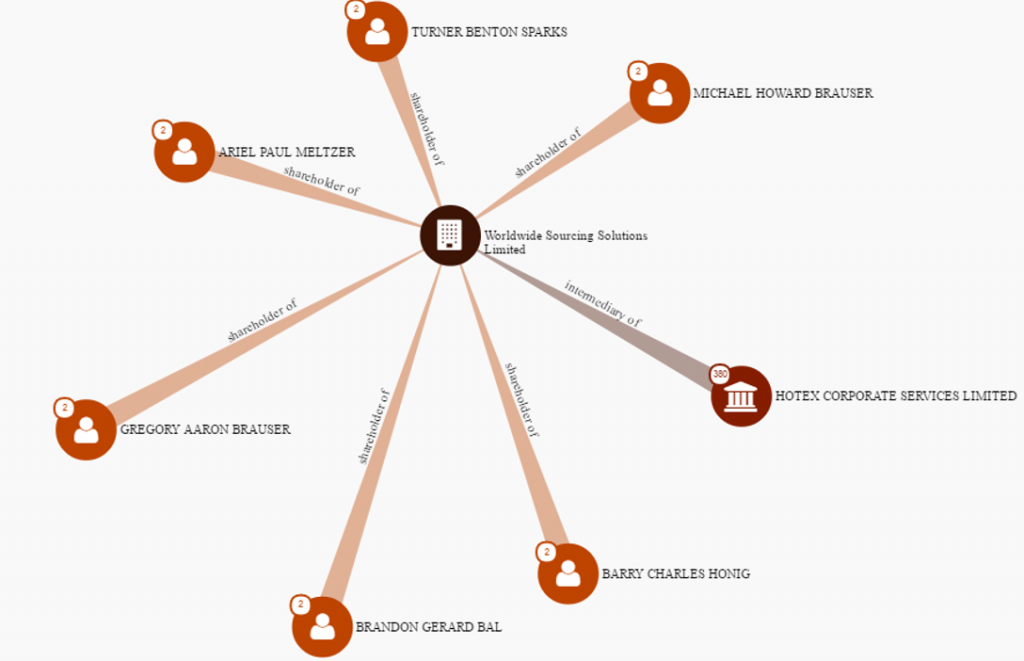

Those looking at MGT management and wondering whether or not the company has any type of pump and dump background to it should immediately be alarmed by the presence of Michael Brauser and Barry Honig.

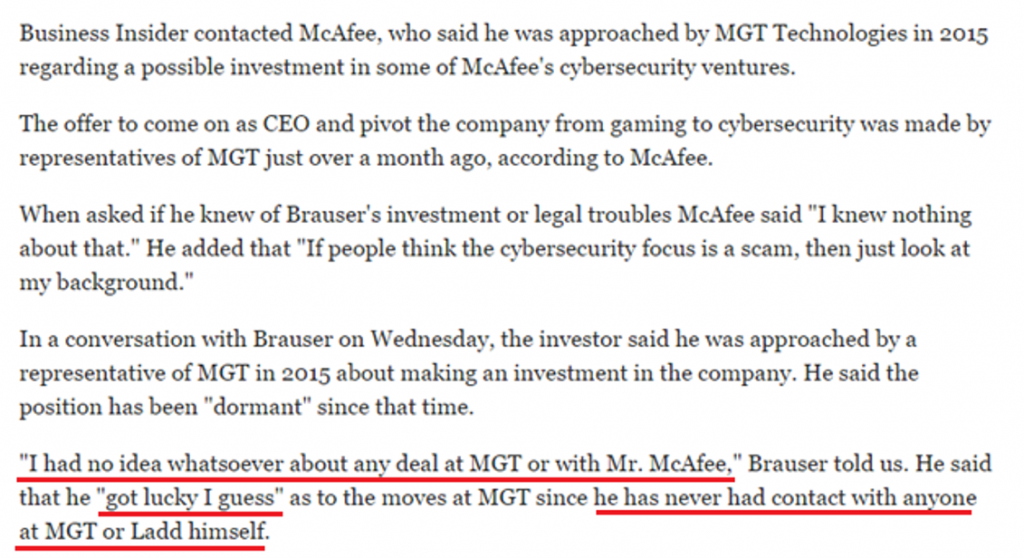

This Business Insider article from May 9th seems to suggest that there’s simply a lot of “coincidences” between Brauser, McAfee, and Honig’s involvement.

Brauser’s statement that he hasn’t had contact with Honig is especially surprising to us, given the long track record the two have working together. We find it absolutely astonishing and nearly unbelievable that these two had no contact involving this investment.

Surely, if one could prove that Brauser and Honig had contact with one another recently, it’d be easy to assume they’d discuss this transaction through the course of normal business, right?

Anyone that needs more information about the potential “shell games” that have been played in the past between Honig and Brauser should read this extremely comprehensive article detailing many of their past investments together. After reading that article, it is extremely difficult for us to believe that one doesn’t know what the other is doing.

In the meantime, we will leave you to ponder this link and this graphic:

Until then, will the SEC ever get around to looking into this situation? Only time will tell. The fact that they have not already speaks to how grossly undermanned they are in this war. However, if the SEC does begin to look into MGT with the same level of scrutiny that we have, then we believe that investors could be playing a game of financial Russian Roulette.

Disclosure: No Position in MGT at time of article

Full Disclaimer: https://geoinvesting.com/terms-conditions-privacy-policy/

Daniel Watkins

Buying in the low $1 is an easy buy and hold for MGT to sell upon the surge from D-vasive Acquisition news, whenever it finally comes.

Angelo

So it’s like saying I own the home my bank has a 90% loan on.

It’s really about who is in control.

Banks usually leave us alone to do as we like in our home, they mostly own.

McAfee created and ran McAfee AV until the company board agreed to sell. Potato…Potato (yeah doesn’t quite work the same typed out)…much like perspective.

This article is more “Hate John McAfee” ‘hit piece’ than factual, though I will give the author kudos for the dazzle them with superfluous details that prove nothing…facts yes!…Facts about what though? Are you a former Republican Party staff writer in their “Propaganda”…sorry Press Office?

This blitz of false ‘Pump & Dump’ news…where? I can’t seem to find anymore than maybe 1-2 articles or press releases per week, and Tiffany the new MGT PR person hasn’t released much more since coming onboard a few weeks ago

zeon

Very well-researched piece. You know you can submit a whistle blower signal through the SEC site, right? You can’t expect them to read every article on the net

zewill

Interesting and well presented. Will be following this very closely (no position and no intention to buy into or sell stuff I definitely dont understand)

Andy

What is the latest with this little Circus? 6/19/2016

GeoTeam

We are still monitoring the story and may provide an update based upon our latest research.

Joe

Are you short the stock? I don’t see your disclaimer.

GeoTeam

@Joe – Our position is and was always at the bottom of the article.

Luke Severino

I HAVE MADE A FOIA REQUEST WITH THE SEC FOR ALL EMPLOYEES POSITIONS IN MGT – LETS SEE WHAT IS ABUNDANTLY CLEAR

GeoTeam

@Luke – Ata boy. Good for you. We have nothing to hide. Ref. @Joe response.