Summary

- Anavex is being touted as the potential next biggest thing in biotech; consequently, its market cap ballooned to over $200M; Anavex’s former President was involved in several pump and dumps.

- Recent pumps that the stock got from Australian news outlets and its Orphan Drug Designation are meaningless, with the latter debunked thoroughly by The Street’s Adam Feuerstein.

- The promotion of Anavex’s story is eerily reminiscent of our 2014 exposé on Stellar Biotechnologies, which sold off by more than 60% in the weeks after our article.

- AVXL has used the Primoris Group for investor relations, a group tied to other pump and dump outfits.

- A penny stock newsletter received $200,000 to “promote” AVXL, supporting an environment for Anavex to raise cash dilutive capital. We contend Anavex is worth its book value: $0.36.

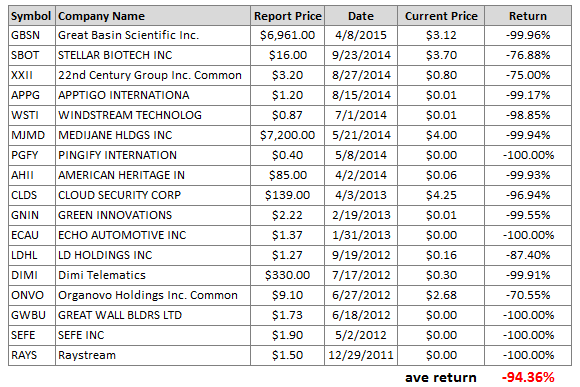

It has been a while since we published a pump and dump exposé. Between 2011 and 2015 we published articles on 17 pump and dumps. The average subsequent decline was over 90% over the course of the long term, with many stocks succumbing to an immediate downward reaction in price. As seen below, every stock eventually plummeted, destroying shareholder wealth.

GeoInvesting Pump and Dump Report Returns

Note that many of the report prices are split adjusted.

To put it simply, we have a knack for sniffing out pump and dumps, and the smell coming from AVXL is anything but pleasant. The Anavex Life Sciences (AVXL) pump campaign is almost identical to another Alzheimer “miracle” stock we outed back in 2014 that has fallen over 60% since our exposé.

Our subscribers need to be aware of the risk in shorting biotech stocks, so get ready for a wild ride. Management teams of shady biotech operations play on the gullibility of everyday investors that have little to no scientific knowledge on the subject matter by pumping out “technical” press releases that sound great on paper. Many of these stocks can pump hard before they ultimately crash. Our findings should help to show that AVXL is full of hot air, hopefully protecting investors from future investment losses we see in this equity.

In Biotech, We Wouldn’t Bet Against Martin Shkreli

Anavex Life Sciences, we believe, is not likely to be one of the biggest things ever to happen in the rapidly growing Alzheimer’s Disease (“AD”) treatment market. Instead, we believe the company is perfectly positioned as just another pump and dump that will likely have little to no residual equity value as the story plays out. As usual, we looked at all of the available evidence, consulted with experts, and carefully weighed the facts before arriving at our decidedly negative opinion. This opinion also happens to be shared by none other than famed biotech “bad boy” and short seller, Martin Shkreli:

We know that the AVXL controversy has been ongoing for months now, so we don’t want to rehash what has already been said. In this article, we’re simply going to look at the promotional nature of the stock, we’ll take a quick look at the science, and we’ll draw the conclusion that this pump is likely to end in the near term with a substantial dilutive stock offering, likely at much lower prices.

AVXL Reminds us of Another Pump and Dump

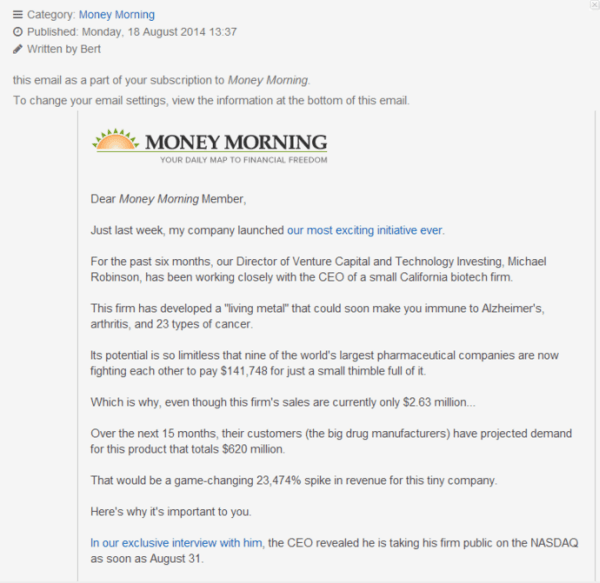

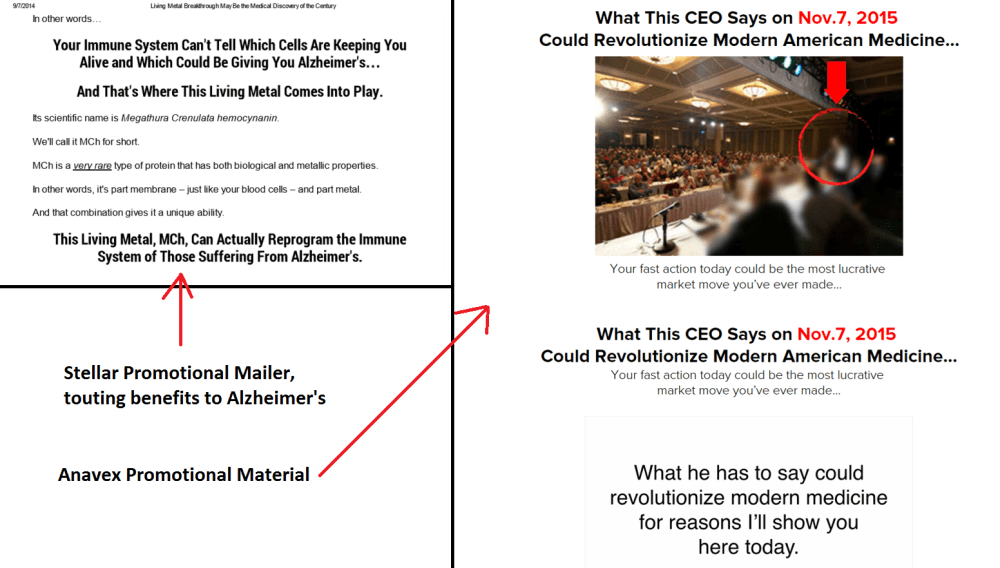

The promotional nature of this company reminds us very much of Stellar Biotechnologies (formerly SBOTF now SBOT), another biotech stock that we wrote about in 2014. Our article raised awareness about stock promoters promising retail investors fascinating amounts of wealth from a little-known niche that could help with Alzheimer’s. Their promotional material included letters that looked like this one:

Note that this letter lays out a couple of recurring themes we will see with AVXL:

- The potential for a treatment of Alzheimer’s disease

- Pointing to comments from a CEO as a catalyst

- Inflated projected financials

- The “most exciting initiative ever”

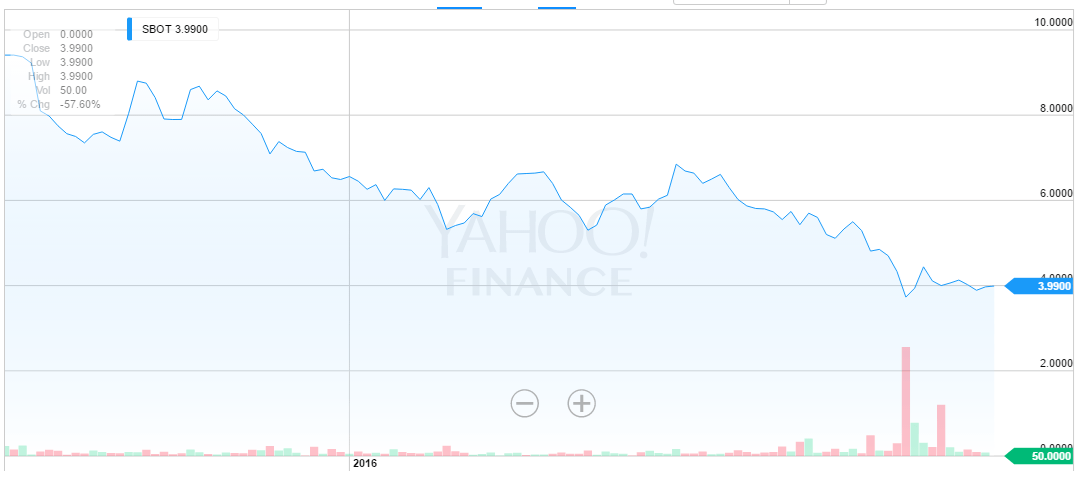

Stellar, similar to what we believe will happen to AVXL, was unable to produce anything meaningful since its promotional campaign and the stock went from over $2 to about $0.50 before SBOTF underwent a 1-10 reverse split and uplisted to the Nasdaq, where it now trades with a pre-split value of about $0.39. Similarly, AVXL also enacted a reverse split on October 7, 2015 to uplist to the NASDAQ.

Since uplisting, SBOTF’s price has been cut in half.

All in all, not quite the success story it was touted to be in its mailers and promotional material.

To draw further comparisons, on the left is a piece of Stellar promotional material, next to a piece of Anavex promotional material (on the right) we recently discovered. Both companies seem to be leveraging the public’s awareness of Alzheimer’s and both companies looking to lure investors into the stock promising massive potential returns and a “disruptive” technology.

They are alarmingly similar in both content and presentation.

With regard to Anavex, this write-up is a must read, as it appears to show how the promotion got started and it documents all of the promotional material that was put out about the company:

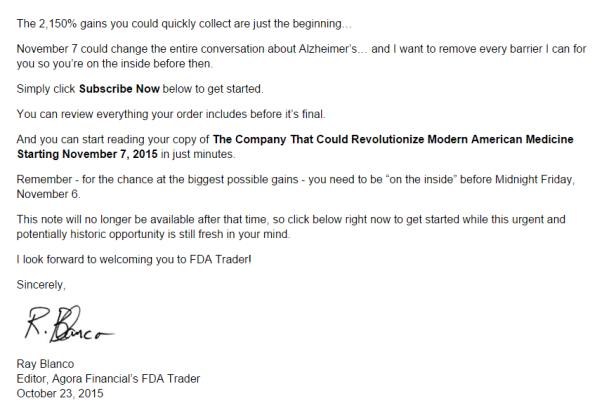

During the week of November 2nd, 2015, a promotional “newsletter”, run by a site claiming to sell stock “research” and investment advice named Agora Financial, was sent around urging investors to jump on a little known stock, trading for about $9, that was about to, with almost complete certainty, rocket overnight to $200, or a gain of 2150%, and even further hinting that the stock could be worth as much as $900 or a 10000% gain. In true infomercial fashion the promotion encouraged the audience to act now to not miss the chance to “be in for the wealth-ride of a lifetime.”

Enter Anavex Life Sciences, a tiny company with less than 10 employees (until recently had only 1 employee) based in New York City, trading under the symbol AVXL, and the subject of this promotion.

According to the Agora Financial author the value of AVXL was about to rise overnight to $6.5 billion, if not $30 billion(!), a staggering amount for such a small entity that has never generated any revenues, has virtually no assets, and was trading for $0.60 per share(worth about $20 million in total) in early 2015.

Here is some of the additional promotional material we were able to locate and find using this link.

You can also view the full transcript of the promotional video here:

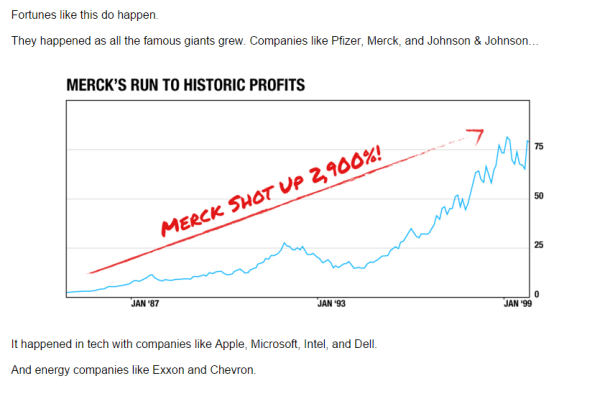

The material follows through comparing Anavex to companies like Merck and Johnson & Johnson, claiming that “fortunes do happen”.

The promotional material finishes with a plea to investors to subscribe to its newsletter. It also states that gains of 2150% are possible. The material touted November 7th as the day when the “conversation could change” about Alzheimer’s.

Here’s what the stock has done up to, and since, November 7th. The conversation changed, alright — to the tune of about 70% losses for those that were buying into mid November. We think it will now be a slow burn closer and closer to $0 as the company dilutes to support operations going forward.

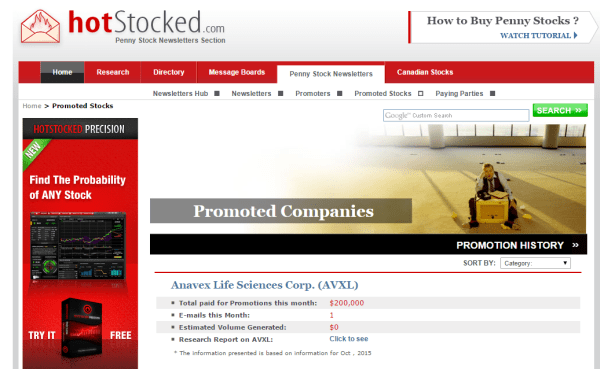

We also found this website, which appears to show that a penny stock newsletter was paid $200,000 to “promote” AVXL back in October of 2015.

Further, we discovered that one of the contact numbers listed on AVXL’s press releases leads to the Primoris Group in Canada.

This outfit from Canada has been involved with several other companies that were pumped, including HiEnergy. HiEnergy was a company that reverse merged in 2002 into SLWE and changed its ticker to HIET. Following fraud charges from the SEC, it was subsequently delisted in 2011 and revoked by the SEC in 2013. As you can see from this lawsuit, Primoris was the firm that was “responsible for HiEnergy’s investor and public relations” and that they were allegedly granted stock options for their services.

And while message boards aren’t the best source of information, this German forum talks about Primoris potentially being behind the Argentex pump and dump, as well.

This chart was graciously provided to us by Argentex’s website:

Case in point is that Primoris does not have a track record to hang its hat on.

Further, when we go back to 2007, when AVXL engaged Primoris group, we can see that AVXL’s president at the time was Harvey Lalach.

Lalach also had ties to San Telmo Energy, based on this news release:

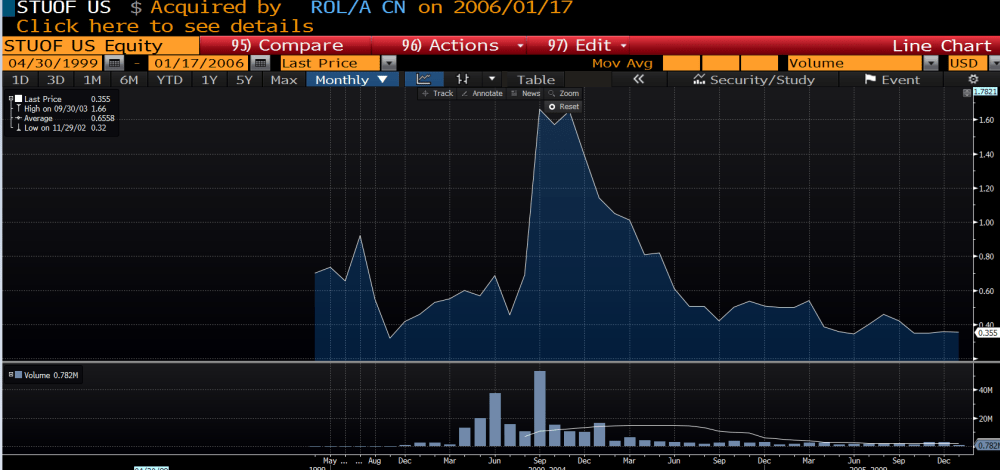

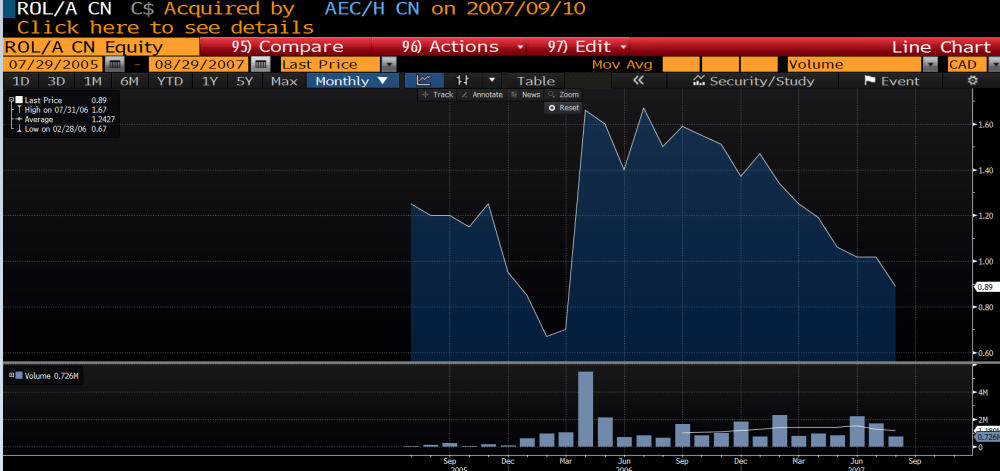

Judging by the chart below, before it was acquired, it also seemed to have a period of “optimism”:

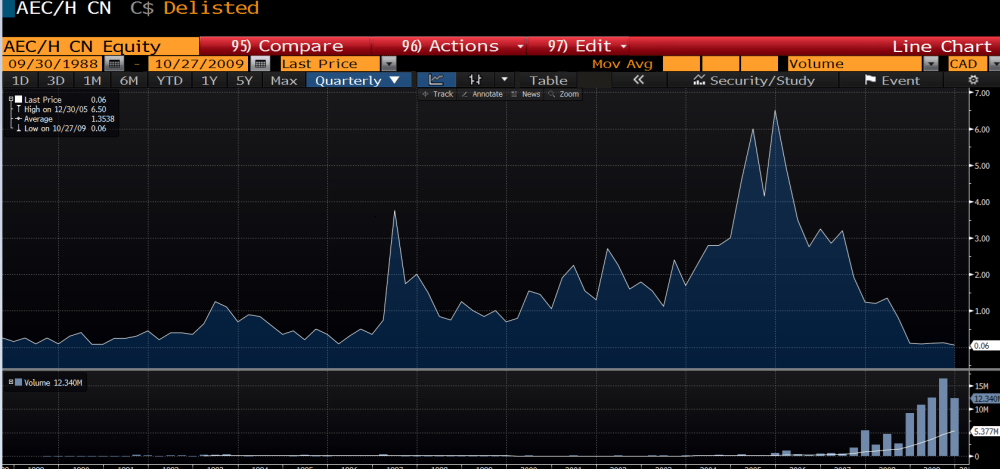

The company was acquired on 1/17/2006 by ROL/A CN, but only after it lost about 80% of its value. From there, ROL/A was acquired by AEC/H CN, but only after they had lost 50% of their value.

And from there — you guessed it — AEC/H CN was delisted, but after it lost 99% of its value.

As you can see, there seems to be several degrees of separation between AVXL and companies with a history of pumping and dumping. At best, this is an interesting coincidence that needs to be on the radar of everyone that owns AVXL stock. At worst, this presents a disturbing connection between the genesis of AVXL and other failed companies.

AVXL Will Eventually Just Be Distant Memory

What we do not contest is that Alzheimer’s Disease is going to be an enormous market in the future. However, we think that paid stock promoters may be playing to the emotions of the American public and people that have been affected by Alzheimer’s disease in order to sell them the dream of buying a stock that, on paper, appears to be worth about $0.31 per share, at best. Furthermore, all of the major drug companies, including Eli Lilly, Pfizer, and Johnson & Johnson are looking to address Alzheimer’s disease. Collectively, they represent stiff competition to Anavex’s six person full time employee roster.

These companies, collectively, have tens of thousands of employees along with research and development budgets in the hundreds of millions. The National Institute of Health spends about $480 million a year on Alzheimer’s research. It seems that even if you want to believe in AVXL, the dilutive capital it will have to raise makes it an unattractive investment in current levels. AVXL is a six person company with very limited clinical data and limited resources. In the case of who is going to develop the breakthrough in Alzheimer’s disease first, we are going to put our money on somebody other than Anavex.

You can tell simply from the stock’s meteoric rise and subsequent fall that AVXL is a day trader’s paradise, with likely very few buyers holding with long-term intentions. We classify AVXL as purely a “momentum” stock here, as the price of the equity is disconnected from any and all fundamentals.

A recent pump from the $4 region to back over $5 came as the result of the company declaring orphan drug status for its ANAVEX 3-71 drug for frontotemporal dementia. Per the FDA’s website,

“the Orphan Drug Designation program provides orphan status to drugs and biologics which are defined as those intended for the safe and effective treatment, diagnosis or prevention of rare diseases/disorders that affect fewer than 200,000 people in the U.S., or that affect more than 200,000 persons but are not expected to recover the costs of developing and marketing a treatment drug.”

This is most pertinent when a drug is approved, and obtaining this status is hardly a difficult task.

This pump was debunked quickly by The Street’s Adam Feuerstein, who promptly took exception with the company’s statement that:

“We believe that Orphan Drug Designation for Anavex 3-71 for the treatment of frontotemporal dementia is a significant achievement.”

Feuerstein retorted:

Sure, if you consider answering eight questions on a standardized Food and Drug Administration form to be a “significant achievement.”

Answer eight questions on an FDA form. Do it correctly. Make two copies of the form. Send to FDA. That’s all it takes for any biotech and drug company to secure orphan drug designation from the FDA. It’s really that easy.

Is that a “significant achievement”? No, except if your ulterior motive is to hoodwink gullible retail investors into buying your stock.

The company also saw its shares pump slightly on the morning of April 25, 2016, in response to an article in the Australian press detailing the story of a woman who was able to “regain the ability to play piano” after taking AVXL’s drug. Feel good stories like these have often foreshadowed less than stellar results in clinical trials, where AVXL’s drug will be put to the only test that matters. We believe that pumps that occur on the back of “news” that’s anything other than clinical trial data is an opportunity to short.

We know that the AVXL argument has been going on for some time now, so we don’t want to rehash what has already been said. In this article, we are simply going to look at the promotional nature of the stock, we will offer our take on the science, and we’ll conclude that this stock pump is likely to end in the near term with a substantial dilutive stock offering and a much lower share price.

Our Brief Take on the Science

One of the most important parts about AVXL is whether or not the science adds up. We’re certainly not convinced, and AVXL will have to spend 10’s of millions before anyone can even begin to have any confidence in the science.

While it’s true that AVXL appears to be moving forward with clinical trials, we are skeptical of these trials producing any type of meaningful clinical results when conducted in a controlled double blind environment.

Basically, we believe AVXL has all the hallmarks of being a company that has done, is doing, and will continue to take every initiative to drive its stock up, while delaying execution on the costly clinical development necessary to actually ever determine the efficacy of its drug and bring it to market or sell out to big pharmaceutical companies.

AVXL discloses very little of its clinical data and we believe the number of patients in AVXL’s trials are so small that the trials are almost – but not quite – meaningless. The outcome or just the teaser top-line results of their Phase 2a trial briefly swayed market sentiment but we doubt that any pharma company would think, based on this ‘new’ data, that they would make a decision to collaborate with AVXL or to buy them.

As others have pointed out, betting that what AVXL has is “the cure” is just that – a gamble based on very little objective knowledge.

To make matters worse, AVXL’s drug faces a host of AD drugs and drugs not specifically marketed for AD which work on mechanisms similar (if not actually the same) to the AVXL drug, targeting the sigma-1 receptor that could be used along with Aricept (which itself includes in its mechanisms of action being a sigma-1 receptor agonist).

Conclusion — Dilution Coming!

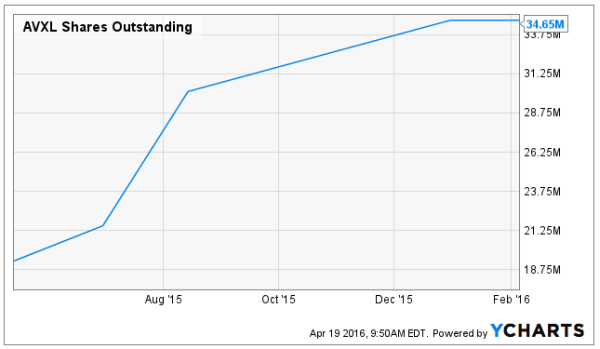

The company is going to be diluting to fund its operations. Here’s a look at the outstanding share count over the small course of the company’s recent history. At this clip, investors should be expecting dilution of about 50% every 12 months. As the equity price drifts lower, the dilution will likely get more pervasive.

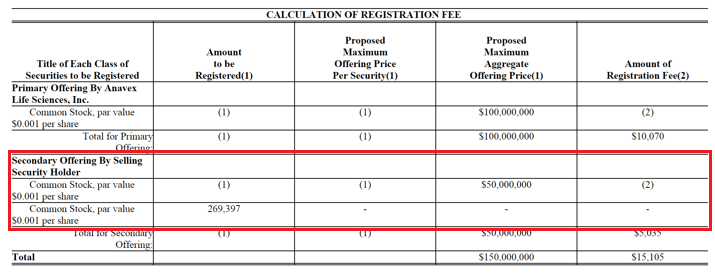

We also want to make note of an S-3 that was filed in late October 2015, which denoted that not only was the company was issuing new shares, but holders of the company’s stock were ready to liquidate and sell $50 million worth of shares to those ready to buy into the AVXL story. (This never actually materialized, but still raises a red flag).

So, in addition to the company potentially selling stock, its shareholders are also unloading onto the open market.

Why sell all the way back then if the best is still ahead for the company?

We would strongly caution retail investors to thoroughly and rigorously evaluate the science behind AVXL’s proposed drug and the backgrounds of those involved with the story.

In a situation like this, it is our job to evaluate all of the available evidence and come to a decision on how we want to invest. With basically zero fundamentals to act as support for the company, we are hard pressed to value this company at anywhere near over $1 per share, when, even if it turns out to be a success, there are going to be years of trials and significantly more data and work that needs to be done before monetizing such a drug.

Timelines for these types of trials getting to a point where they reach the market are not unlikely to be 5+ years. Will the market extend this incredible valuation onto a company that is worth over $200 million on paper for the next five years – let alone five months?

According to the latest available SEC data, AXVL produces zero revenue and has only about $13.85 million in cash. Its book value is close to about $0.36 per share. This doesn’t seem, to us, to be a leading candidate for a company with a market cap over $200 million.

In a best case scenario, the amount of capital that is going to have to be raised in order to push the company’s drugs through FDA trials is likely well more than $50 million. With just $13 million in the bank currently and a quarterly operating cash burn of between $1.4M and $3.2M, we can see only one way that the company can raise the necessary amount to push through trials, and that is through diluting its existing shareholders.

We find it more likely that this six person company has very little chance of making a significant impact on the Alzheimer’s market, let alone one that is going to justify a $200 million market cap, and we think that once retail investors that have been lured in by delusions of grandeur start to exit, along with momentum players and traders, the stock has significantly further down to move. In addition, the company is likely to raise cash relatively soon as long as its stock price can stay as high as it is. This cash will dilute current shareholders, further increasing the amount of distance between the company’s valuation and the company’s fundamentals.

Should the facts change, we will reevaluate them, but after researching the case at length, we are firmly on the short side of AVXL.

John Nelson

Anavex is bottom of the barrel trash. Missling receives over $9 million in compensation for diluting baggies.

Amor Mehta

This rag of an article has no value now nor did it have any value in 2016 when it was first published.

In the 5 years since this article’s publication, Anavex Life Sciences have proven that its pipeline of drug candidates all have shown amazing potential – starting with Blarcamasine (Anavex 2-73).

Anavex share price is now well into the $20s PPS.

This past Monday – Anavex published its findings in its Phase 2 parkinson’s disease dementia trial where both the primary and secondary endpoints were met. Same with Rett syndrome.

Anavex Life Sciences has exceeded its enrollment numbers for its Phase 2/3 pivotal Alzheimer’s disease trial which will end next year.

With its current share price in the $20s PPS – Anavex is looking a lot better.

All your “thoughts” have been disproven in the past 5 years.

YOU WERE SO WRONG!

Paula Nelson

Short at your own risk -Big Parma is looking “slowing the progress of the disease” by 2020. Anavex working on different tragets. Not all stock promos are paid for by the company. Partnership is likely, this is a hit piece.