- CBAK lost a primary operating asset to foreclosure, which should result in the company reporting little to no revenue when it files its Q4 2014 September results.

- Loss of asset speaks volumes. CBAK hoped to sell assets to fund future growth and repair its balance sheet sporting Q2 negative equity of $56.5M, up 16% vs. Q1.

- We don’t think many investors buying CBAK are aware of recent developments since the company has not issued any formal related press releases on major news wires.

- We question CBAK’s viability to continue as an operating entity unless it raises substantial capital, which the company admits has been challenging.

- CBAK is now essentially a start-up, which we believe should be valued on shareholder equity. Our best case scenario puts CBAK’s new book value per share at around $0.10.

China BAK Battery (CBAK), together with its subsidiaries, engages in the manufacture, commercialization, and distribution of standard and customized lithium ion (Li-ion) rechargeable batteries. However, as of Q2 2014, all of China BAK’s producing assets have been repossessed by creditors. The company has one remaining facility which is still under construction. CBAK’s shares have been on a tear since the end of June reaching a 52-week high of $5.00 on July 2, 2014. According to an article at ZDNet, the run-up was influenced by LG Chem’s intention to invest hundreds of millions of dollars in China to build an electric vehicle battery factory.

Misplaced Investor Optimism

Investors may not know that when CBAK reports its financial results for Q4 ending September 30, 2014 it will likely report little to no revenue and have minimal to possibly negative shareholder equity. Why? CBAK just lost its primary operating asset, BAK International, to a Mr. Jinghui Wang due to July 2014 foreclosure proceedings when it defaulted on an $86 million loan obligation it executed with Wang just around six months ago via two transactions. Mr. Wang then collected on his debt by selling his BAK international interest to a “third party.”

Investors are now left with a company that is in the process of building a new battery facility in Dalian that probably won’t even begin to generate revenue for several months. And there is no guarantee that management will be successful in growing its new business, given that it seems to have failed in its prior attempt to successfully grow a similar business with past due debts to suppliers and creditors. In fact, the new factory, intended to target sexier and higher margin battery segments (like EVs) than CBAK’s legacy business, has not even met the minimum required $6 million registered capital to legally begin operations.

At best, assuming that the transfer of BAK International included all of its assets and liabilities, we estimate that CBAK’s shareholder value per share is a paltry $0.09 per share. This generous analysis assumes that the “third party” acquired a business with negative net equity of $55 million.

Finally, investors that are excited about subsidies CBAK received to fund certain initiatives should know they were not provided carte blanche, as these subsidies have to be repaid.

Basically, CBAK is now a development stage, near $50 million market cap, company with little if any revenue and minimal book value. Unfortunately, investors buying CBAK shares who don’t scrutinize SEC filings may not be aware of these developments since the company has not issued any formal press releases via major news wires.

Foreclosure Development Is No Joke; Dilution On The Table

The foreclosure of CBAK’s primary asset should not be taken lightly. Prior to the foreclosure management had hoped to sell this asset to reduce debt and raise cash to fund its new growth initiative. So it appears that the potential sale of the asset would have been integral to CBAK’s sustainability. Here are passages from CBAK s Q2 2014 report that was filed around 40 days before the foreclosure of Shenzhen occurred:

“We intend to sell part of our low efficiency assets and appreciating land and properties to repay our short term debts and to provide cash for the development of more promising products such as high power batteries and Electric Vehicle batteries”

As we have been suffering severe cash flow deficiencies, we intend to sell part of our low efficiency assets and appreciating land and properties to repay our short term debts and to provide cash for the development of more promising products such as high power batteries and Electric Vehicle batteries. We transferred our 100% equity interest in Tianjin Meicai to an unrelated party on August 27, 2013. We also intend to dispose of our 100% equity interest in BAK International and its subsidiaries (including all their assets and liabilities), and the properties in Tianjin.

Now it appears CBAK will have to rely on other types of financing “for the development of more promising products such as high power batteries and Electric Vehicle batteries” which, given the financial condition of the CBAK and the lending environment in China, may not be in the bag. From the Q2 2014 filing:

“In addition, as we are facing a more challenging business environment and the Chinese government has placed tightening lending policies on state-owned banks in China, we encountered more difficulties in obtaining funds from local banks, and have a number of past due liabilities to suppliers and third party creditors.” [Emphasis added]

CBAK was already facing challenges raising capital when it STILL HAD its primary operating asset. And now the situation has gotten substantially worse.

CBAK Defaults On Loan Payment

LG Chem’s plans have largely overshadowed what was unquestionably grave news disclosed in a CBAK 8-K filing on July 3, 2014 announcing the loss of substantially all of the Company’s BAK International Limited operating assets to foreclosure. We will show that BAK International Limited accounted for nearly 100% of CBAK’s 2013 and 2014 revenue. Although CBAK’s shares have since retraced some of the July 2 surge they are still in our opinion substantially overvalued at around $4.00.

On April 24, 2014, China BAK received a default notice from Jinghui Wang, who loaned the company about $86 million dollars in two loan agreements dated December 17, 2013 and January 8, 2014. As part of the loan agreements, the company pledged 100% of its equity interest in wholly-owned Hong Kong subsidiary BAK International Limited. In an April 30, 2014 8-K, the company warned that Mr. Wang could foreclose on the ownership of BAK International if a settlement could not be reached. CBAK noted that BAK International constitutes a substantial portion of the company’s assets.

After the market close on Friday July 3, 2014, the company revealed in an 8-K filing that they could not reach a settlement with Mr. Jinghui Wang, having defaulted on loans he made to CBAK. The 8-K stated,

“On June 30, 2014, the Company received from Mr. Wang notice that due to Shenzhen BAK’s default under the Loans, he had foreclosed his security interest in and sold and transferred to a third party the Pledged BAK International Equity for a purchase price of RMB520 million.” The statement made in the 8-K follows:

“ITEM 8.01. OTHER EVENTS.

As previously disclosed, to repay its overdue bank loans, Shenzhen BAK Battery Co., Ltd. (“Shenzhen BAK”), a wholly-owned subsidiary of China BAK Battery, Inc. (the “Company”) borrowed from Mr. Jinghui Wang an aggregate of RMB520 million (approximately $85.9 million) (the “Loans”) in December 2013 and January 2014. To secure the repayment of the Loans, the Company and the Company’s wholly-owned Hong Kong subsidiary, BAK International Limited (“BAK International”) separately entered into a corporate guarantee with Mr. Wang, under which each of the Company and BAK International irrevocably and unconditionally guaranteed to the lender timely performance by Shenzhen BAK of its obligation to repay the Loans. In addition, the Company pledged 100% of its equity interest in BAK International to the lender as security for Shenzhen BAK’s repayment of the Loans (the “Pledged BAK International Equity”).

On June 30, 2014, the Company received from Mr. Wang notice that due to Shenzhen BAK’s default under the Loans, he had foreclosed his security interest in and sold and transferred to a third party the Pledged BAK International Equity for a purchase price of RMB520 million.

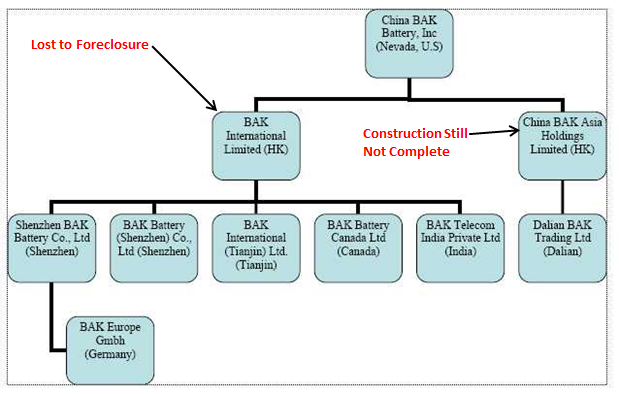

As a result of the above foreclosure, the Company currently owns a Hong Kong subsidiary, China BAK Asia Holdings Limited, which in turn wholly owns two Chinese subsidiaries, Dalian BAK Trading Co., Ltd. and Dalian BAK Power Battery Co., Ltd. (“Dalian BAK Power”). Dalian BAK Power is engaged in the business of developing, manufacturing and selling new energy high power batteries, which are used in electric cars, light electric vehicles and other high power applications.”

We believe that it is currently a bit of stretch for CBAK to state that…

“Dalian BAK Power is engaged in the business of developing, manufacturing and selling new energy high power batteries, which are used in electric cars, light electric vehicles and other high power applications.”

… since Dalian BAK Power was established in 2013 with a yet to be fully constructed manufacturing facility that has not raised the registered capital to operate.

CBAK Now a Development Stage Company

After the loss of BAK International, CBAK now owns only two Chinese subsidiaries; Dalian BAK Trading Co., Ltd. and Dalian BAK Power Battery Co., Ltd. As seen in the chart below, the company lost a substantial portion of its assets with the forfeiture of BAK International.

That leaves Dalian BAK Power and Dalian BAK Trading Co., Ltd. CBAK’s Q2 2014 filing carries the following information:

“Dalian BAK Trading Co., Ltd. (BAK Dalian), a wholly owned limited company established on August 14, 2013 in the PRC; vii) Dalian BAK Power Battery Co., Ltd. (Dalian BAK Power), a wholly owned limited liability company established on December 27, 2013 in the PRC;”

According to SEC filings, BAK Dalian was only just established as a company on December 27, 2013 and has not raised the $6 million needed to begin operations.

“Up to the date of this report (May 20, 2014), the Company is in negotiation with the Business Administration Bureau of Dalian District for extension of payment of the initial capital of $6,000,000.” Page F-5 Q2 2014 SEC filing

Combine these findings with the fact that the Dalian BAK manufacturing facility is still not complete, and it appears safe to assume that Dalian BAK Power did not have any substantial business as of May 20, 2014. We believe this is still the case and is supported by on-the-ground due diligence indicating that Dalian BAK Power manufacturing facility is not yet fully constructed and that construction will not be completed by the end of CBAK’s Q4 2014 ending September 30. Furthermore:

- The facility will likely have to go through several months of testing (assuming construction is ever completed).

- CBAK will likely have to convince banks or investors to provide it with capital to complete construction and manufacture product.

- CBAK could have lost a good deal of its customers that deal or have dealt with Shenzen BAK International, its main source of revenue before BAK international was lost to foreclosure.

Still, there is no guarantee that customers will wait around for CBAK to potentially launch Dalian in a market with capable competitors such as Highpower (HPJ). CBAK Q2 2014 filing states:

“The light electric vehicle market was becoming more competitive. We intend to give up low value customers while trying to retain high-end customers.”

Investors deserve far more information from CBAK management than what has been provided to date.

Valuation

Currently, since CBAK is essentially a zero revenue producing asset, we believe that book value analysis is the appropriate way to value CBAK, that is until it is assured that the necessary capital can be raised to complete the construction of the Dalian facility to be in a position to generate revenue.

Investors may be assuming that CBAK is in good shape now that it is not burdened with BAK International’s debt load which resulted in CBAK sporting shareholder equity of around negative $56 million. However, even after considering the aggressive assumptions we used to value CBAK, we calculate its post-BAK International equity per share to be around $0.10. At around $4.00, CBAK is currently trading well above this value.

To value CBAK post-BAK International we assumed that all of its assets and liabilities were transferred to Mr. Wang, ultimately ending up with the “third party.” We also erred on the side of caution and retained assets we could not identify as belonging to BAK International. Likewise, we were aggressive by moving liabilities from the balance sheet, which we could not easily identify.

Ultimately, we believe our calculation could be overly aggressive since we assumed that the net assets transferred out of CBAK to the “third party” amounted to negative $55 million, for which the “third party” paid Mr. Wang $83 million. So we believe that in the end a good portion of that negative $55 million could have remained with CBAK. Or perhaps there is more to this transaction than meets the eye. Who is this third party? We urge management to provide more details to investors on what was actually transferred to the “third party.” We know that Mr. Wang once was a shareholder in CBAK. Why did he force foreclosure so quickly as opposed to giving the company time to sell BAK International assets (some land) that may have been able to cover debts and provide working capital for CBAK? Recall that company filings indicate that CBAK’s land (use rights) had appreciated:

“We intend to sell part of our low efficiency assets and appreciating land and properties to repay our short term debts and to provide cash for the development of more promising products such as high power batteries and Electric Vehicle batteries”

Our best-case reconciliation of CBAK’s balance sheet can be seen below:

(click to enlarge)

Additional assumptions with respect to above table:

- According to SEC filings BAK Shenzen and BAK Tainjin accounted for 80% and 20% of facility square footage, respectively.

- 100% of building asset transferred as a result of foreclosure

- 80% of machinery, office expense and motor vehicle assets transferred as a result of foreclosure since some of Tianjin assets had been in the process of being moved to Dalian since 2013.

Tianjin operations being wound down since its assets had been in the process of being moved to Dalian since 2013.Loans And Subsequent Foreclosure And Disposal Of Assets Raise Questions

The loans from Mr. Jinghui Wang in December 2013 and January 2014, the creation of Dalian BAK at the end of December 2013, and the subsequent foreclosure and sale of the assets on June 30, 2014 raise a number of questions and issues, enumerated below.

CBAK’s Operations And Financial Condition

- Substantially all of CBAK’s business operations were lost to the foreclosure on the BAK International assets. What is the plan of operations for the company and how will its financial condition be impacted during the period it takes to get the Dalian BAK operations up and running?

- We have to assume that business operations have been suspended until the Dalian BAK operations are online. Does the company have adequate working capital and financing to bridge the transitional period while operations are moved from Shenzhen and Tianjin to Dalian?

- Assuming the new Dalian facility eventually goes online, how long will it take to validate and ramp up production of market-ready EV batteries? Does the company have customers ready to take delivery of the batteries?

- Will CBAK be able to retain its BAK International customers or will some be lost in the transition? The battery business is highly competitive and customers will have little problem finding new sources of supply from companies that may be far more reliable and solvent than CBAK.

Government Advances And Subsidies Need To Be Repaid

- CBAK received a $24.1 million government advances to relocate its operations from Tianjin to Dalian. The advances will have to be paid back at some point.

- An $8 million subsidy was received for the automated high-power lithium battery project from the National Development and Reform Commission and Ministry of Industry and Information Technology. The company will have to earn the subsidy or pay it back.

- The company also has $15.3 million unearned subsidies for various lithium battery related projects from various government authorities. Are some or all of those subsidies now payable to the respective government authorities now that the Shenzhen operations and assets have been lost?

Conclusion

We believe that investors who are getting excited about CBAK’s near-term prospects probably have not properly interpreted recent developments. The fact that its main operating asset was lost to foreclosure means that CBAK cannot generate meaningful revenues AND cannot raise cash from the sale of this asset to fund its growth plan to participate in a “sexy” segment of the battery market. Concurrently, the foreclosure should raise CBAK’s need to raise capital, while at the same time making this task all the more challenging. These events make it difficult for investors who want to ride the EV hype to get excited about CBAK. Ultimately, we think CBAK shareholder equity remains negative and that it is worse off than before the foreclosure.

Disclosure: Short CBAK, Long HPJ

Disclaimer:

You agree that you shall not republish or redistribute in any medium any information on the GeoInvesting website without our express written authorization. You acknowledge that GeoInvesting is not registered as an exchange, broker-dealer or investment advisor under any federal or state securities laws, and that GeoInvesting has not provided you with any individualized investment advice or information. Nothing in the website should be construed to be an offer or sale of any security. You should consult your financial advisor before making any investment decision or engaging in any securities transaction as investing in any securities mentioned in the website may or may not be suitable to you or for your particular circumstances. GeoInvesting, its affiliates, and the third party information providers providing content to the website may hold short positions, long positions or options in securities mentioned in the website and related documents and otherwise may effect purchase or sale transactions in such securities.

GeoInvesting, its affiliates, and the information providers make no warranties, express or implied, as to the accuracy, adequacy or completeness of any of the information contained in the website. All such materials are provided to you on an ‘as is’ basis, without any warranties as to merchantability or fitness neither for a particular purpose or use nor with respect to the results which may be obtained from the use of such materials. GeoInvesting, its affiliates, and the information providers shall have no responsibility or liability for any errors or omissions nor shall they be liable for any damages, whether direct or indirect, special or consequential even if they have been advised of the possibility of such damages. In no event shall the liability of GeoInvesting, any of its affiliates, or the information providers pursuant to any cause of action, whether in contract, tort, or otherwise exceed the fee paid by you for access to such materials in the month in which such cause of action is alleged to have arisen. Furthermore, GeoInvesting shall have no responsibility or liability for delays or failures due to circumstances beyond its control.