This week’s Skull Session was a real special one for us. We brought in Dean Pernas, co-founder of Pernas Research, alongside analyst Lukas Milosic (@Pixelresearch_ on X) for what turned into another wide-ranging, genuinely useful conversation we’ve been having on Skull Sessions.

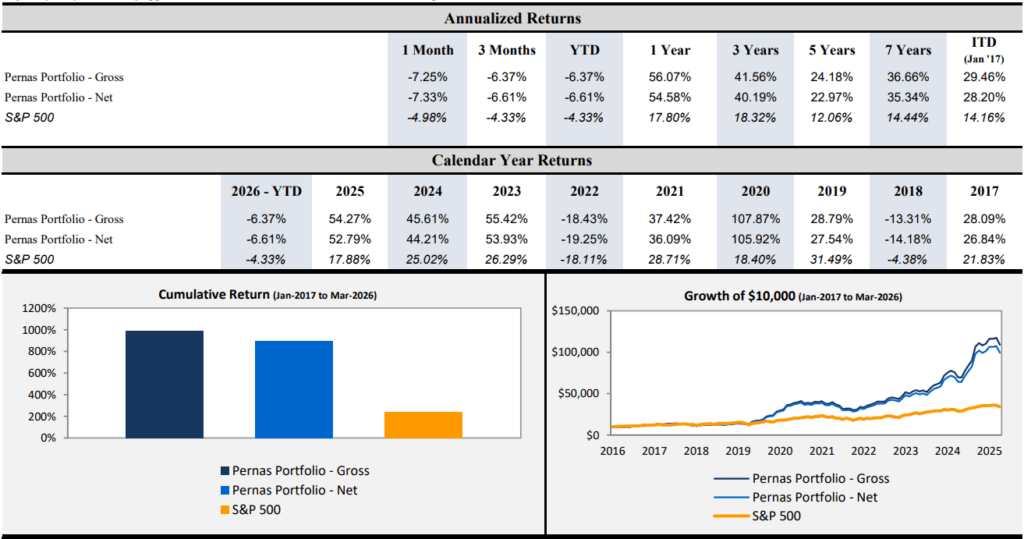

Dean is a chemical engineer by training who spent five or six years at companies like Monsanto, Schlumberger, and Procter & Gamble before making the jump to full-time investing alongside his brother in 2020. Together, they launched Pernas Research in 2023, and what immediately sets them apart is something you don’t see often in the research shop space: a fully audited track record going back to 2017, verified by a third-party auditor.

The returns speak for themselves: multiple years of strong double-digit outperformance, including a 105% year in one of the more productive stretches. They invest their own money, write about what they own, and publish everything transparently.

Motor Investing: A Framework Worth Understanding

The centerpiece of Dean’s investment philosophy is something he and his brother have codified as “motor investing.” Just like a motor drives a car, the motor of a company drives its future financials. Dean frames it as the interplay between internal execution and external demand conditions: Is the company’s strategy improving? Is the management team executing? How are customers and competitors evolving?

He contrasts this explicitly with Buffett’s moat framework, arguing that “moat” implies something static and competitor-focused, whereas motor investing captures the dynamic, directional nature of a business and, importantly, brings customers back into the picture. The sweet spot for Pernas Research is where the motor is clearly strengthening but the financials haven’t yet reflected it. Most of their time is spent investing in stocks with market caps between $300 million and $5 billion.

I love this framing because it aligns closely with how we think about the quality at GeoInvesting and the Microcap Investing Cliff Note Substack. People sometimes assume that means we only have this strict adherence to investing in high-quality companies. That’s not it at all.

We love investing in companies that are moving toward quality, because that’s where you find the best setups being ignored and the ability to buy stocks cheap relative to what they might look like two or three years from now.

Dean put it similarly: they are quality-agnostic by design. They’ll invest in a bad company moving toward okay, an okay company moving toward good, or a good company moving toward great, as long as the trajectory is improving and the market hasn’t figured it out yet. He commented that his brother likes to point out there’s no universally agreed-upon definition of quality anyway, and honestly, I think he’s right.

How They Find Ideas and Where AI Fits In

Dean and his brother run dynamic quantitative and qualitative screens that change depending on the market environment, layer in significant thematic and industry reading, and supplement both with AI tools they’ve built in-house. One standout example that I found pretty cool: they built a scraper in roughly a week, around 8,000 lines of code assisted by Claude, that monitors every 8-K filing and classifies companies by whether they’re pursuing volume-led or price-led growth strategies.

Dean described it as a genuinely magical moment, giving them a completely orthogonal source of idea generation that pure screening or reading simply cannot replicate. ChatGPT and AlphaSense are both part of the toolkit as well, with AlphaSense’s AI functionality on top of expert call libraries being particularly useful for deep industry diligence.

We talk about this a lot here at GeoInvesting, and it was good to hear someone like Dean validate it from his own experience. Our team built our own real-time press release and document monitoring tool for exactly this reason, and it’s been surfacing ideas we would never have caught otherwise.

The “low quality” Energy Focus, Inc. (NASDAQ:EFOI) data center situation earlier this year that showed how you could have made it up ~200% in one day was a perfect example of that. You can read about the InfoArb Case Study we highlighted on GeoWire Weekly No. 235, where we covered EFOI. Dean’s one caution on AI, which I think is worth repeating: make sure it’s pressure-testing your thinking, not just agreeing with you. That’s something we keep top of mind too.

On Capstone and the Data Center Angle

One of Pernas Research’s most noteworthy recent calls was Capstone Energy+, Inc. (OTC:CGEH). I actually had a similar brush with Capstone myself, @GrumpierBTDay flagged it around the two-dollar range and I looked at it but just didn’t pull the trigger. Frustrating in hindsight. It’s now $10, although I did trade it a few times and still own a small amount right now.

Dean first highlighted it publicly at the MicroCap conference in Toronto when the stock was around three dollars, and it subsequently ran as high as twelve. The thesis was a classic motor investing setup: a company that emerged from a pre-packaged bankruptcy in 2024 with a billion dollars in NOLs, a new CEO bringing real operational discipline, and a demand environment that had fundamentally changed around it.

With AI driving explosive power demand onto the grid, the market for off-grid distributed generation solutions suddenly became far more interesting. Capstone’s microturbines, small natural gas-powered units ranging from roughly 100 kilowatts to 10 megawatts, fill a specific niche around time-to-market. With turbine backlogs stretching out years, Capstone can step in where a customer needs power quickly.

What I found particularly interesting during the conversation was Dean’s point about edge data centers. There are thousands of smaller facilities close to cities, and as AI voice and video applications scale, latency is going to become a much bigger constraint. Capstone’s solutions are sized right for those five- to thirty-megawatt deployments, and Dean thinks that angle is almost entirely overlooked by the market right now.

Gross margins have moved from negative 10% to roughly 20%, and the company posted its first positive adjusted year in its history. The motor is clearly running.

A New Microcap Idea: Last-Mile Fiber for Apartments

Dean also walked through a current speculative position in a microcap connecting last-mile fiber directly to apartment complexes, allowing tenants to have seamless internet access the moment they move in, no modem, no ISP setup required. The apartment owner benefits through a recurring revenue stream that can be borrowed against, effectively increasing property values.

What I didn’t know going into the conversation, and what changed my view on the setup, is that the company actually owns the last-mile fiber itself in these deployments. I had assumed they were renting infrastructure from competitors, but they’re not. That meaningfully changes the unit economics and the durability of the model.

Dean noted that contracts already under activation imply roughly $25 million in recurring revenue within a couple of years, and the stock is trading around two times that figure with no growth assumed. The chairman has done this before, having built and sold a similar business focused on student dormitories to Boingo in 2018 and 2019.

We think this is a three-to-five-year story with a long runway ahead of any serious competitive response from the Verizons and Comcasts of the world. Lukas flagged some related-party items in the balance sheet worth watching, which is fair, though after the IPO proceeds, the structure looks cleaner. It’s the kind of thing we keep an eye on, but it didn’t break the thesis for Dean’s team.

Lessons on Management and What We Keep Coming Back To

A few threads from the conversation stayed with me beyond the individual stock pitches. On management, Dean and I spent real time on the dangers of over-relying on site visits and management interviews, particularly in micro and nano-cap land where promotional tendencies run high and key-man risk is severe.

I’ve had my own experience with this, where I visited a company I owned, came away with real doubts about the culture and the CEO’s understanding of capital markets, sold the stock, and watched it go up more than ten times afterward. It’s a fine line. You can convince yourself you found signal when you’re really just building conviction through familiarity, and that can work both ways.

Dean’s cautionary tale from Endor, a German sim racing company that was wiped out by Chinese competition after a demand surge overwhelmed a CEO too focused on sponsorship deals to address the supply chain, was a vivid illustration of what happens when a founder-operator mistakes brand equity for operational capacity. It reminded me a lot of Peloton.

The lesson we both keep coming back to is that in microcap land, the CEO holds enormous power, and overconfidence combined with stubbornness can destroy a business faster than almost any external threat.

On the broader market environment, we both acknowledged the current frustration of watching low-quality names continue to run higher in pockets of the market. I track this internally through what we call our zombie index, basically a basket of genuinely poor companies we monitor as a sentiment gauge. When that index starts outperforming quality, it’s usually a signal that the market is getting frothy in certain corners. We’re seeing some of that right now.

Our shared view is to stay patient, stay in names where the motor is strengthening, and let time do its work. As Lukas put it at the end of the session, and I thought it was a pretty good note to close on: ain’t nothing gonna break my stride.