While insiders and related parties skim cream off the top…

Chuys Holdings (NASDAQ:CHUY), through its wholly owned subsidiary, Chuy’s Opco, Inc., owns and operates Chuy’s, a full-service restaurant offering a distinct menu of authentic, freshly-prepared Mexican and Tex Mex inspired food. The menu has few items over $10 and the average check is around $13. The company launched its business in Texas in 1982 but did not start to expand its operations until 2006. CHUY has added 22 restaurants since 2009, including 8 in 2012 and currently operates 39 restaurants in 8 states. The company’s management plans to add another 8 to 9 restaurants in 2013 and have 75 operating by 2016.

Chuys Holdings (NASDAQ:CHUY), through its wholly owned subsidiary, Chuy’s Opco, Inc., owns and operates Chuy’s, a full-service restaurant offering a distinct menu of authentic, freshly-prepared Mexican and Tex Mex inspired food. The menu has few items over $10 and the average check is around $13. The company launched its business in Texas in 1982 but did not start to expand its operations until 2006. CHUY has added 22 restaurants since 2009, including 8 in 2012 and currently operates 39 restaurants in 8 states. The company’s management plans to add another 8 to 9 restaurants in 2013 and have 75 operating by 2016.

The company completed the initial public offering (“IPO”) of its common stock in July 2012. CHUY issued 6,708,332 shares, including 874,999 shares sold to the underwriters pursuant to their overallotment option. The company received net proceeds from the offering of approximately $63 million after the $19 million one-time special dividend to preferred shareholders (mainly insiders). The net proceeds from the offering were also used to repay approximately $60 million of outstanding debt under its old bank credit facility. Since the IPO, the company secured a new $25 million revolving credit facility and drew on it to pay off the $5.0 million balance on its old credit facility.

In this article we discuss factors that led us to conclude that CHUY’s current valuation, partly supported by little liquidity for its stock, does not take into account significant risks, all of which should give current or prospective investors pause.

- Insiders are liquidating most of their stock holdings;

- CHUY boasts a P/E of 49X estimated 2013 EPS despite that fact that it expected to report flat 2013 non-GAAP EPS growth;

- CHUY trades at 25X its EV/EBITDA while its peers trade at 8 to 12X;

- P.F. Chang’s, with better metrics and product offerings, went private in early 2012 at an EV/EBITDA multiple of 8.5X;

- EV/restaurant of $14.4 million is 5X the capex and start-up costs of the average restaurant; and

- CHUY is now a public company that in many ways is still managed as a privately held business. No less than 20 related transactions are disclosed in SEC filings, many of which we feel should have been renegotiated or terminated as part of the IPO (cleansing) process.

CHUY’s Share Price Is Supported by Relatively Few Shares in the Float and Low Liquidity

Since going public on July 25, 2012 (priced at $13.00), CHUY has benefited not only from a very favorable market environment for the restaurant sector but, perhaps more importantly, a low public float and little liquidity for its shares. The circumstances, however, changed when in January of 2013, the company registered 5,175,000 shares in a Form S-1 filing that became effective on January 24, 2013. Those shares, priced at around $25.00, will likely find their way into the market as purchasers look to lock in profits, given the recent rise in the share price to over $30. More telling is that JP Morgan, CHUY’s underwriter of the IPO, used the secondary offering to sell most of its stake in the company, and insiders liquidated roughly 50% of their equity positions. JP Morgan and insiders are not done selling yet. As part of a proposed 3.5 million share secondary offering filed on April 8, 2013 JP Morgan and insiders plan to sell more shares.

To sum it up, in less than a year, upon the closing of the April 2013 secondary, insiders will have essentially blown out of most of their common stock:

- After the July IPO, the insiders beneficially owned approximately 62.6% of outstanding common stock; and

- Following the January 24, 2013 secondary offering, insiders owned approximately 31.4% of outstanding common stock.

The April 8, 2013 prospectus discloses that insiders will only own 9.9% of CHUY common stock following the offering. When insiders are selling this much stock should we be buying?

CHUY is a Prime Short Candidate — Valuation is Stretched by Any Reasonable Measure

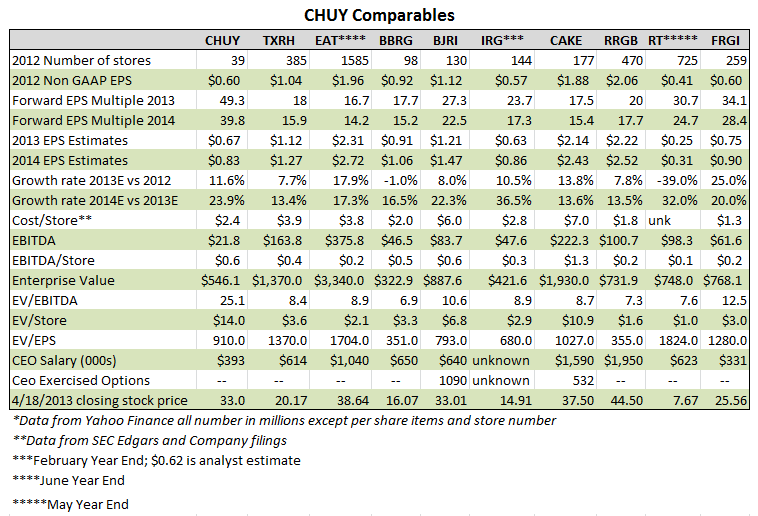

We view CHUY as extremely overvalued. Using any reasonable measure, whether by EPS multiples or enterprise value, the same result is attained. At a P/E of 49 and 40 on 2013 and 2014 analyst EPS estimates, respectively, we believe CHUY is trading at a large premium to its fundamentals and all of its peers – especially when one considers that CHUY’s 2013 non-GAAP EPS growth is expected to be unexciting from 2012 and that its overall growth profile is in line with several of its top performing comps. CHUY’s EV to EBITDA of 27 vs. peers’ EV to EBITDA ranging from 8 to 12 is the most glaring valuation metric that points to CHUY’s overvaluation. We believe that CHUY’s premium valuation is in part being supported by euphoria stemming from a cult-type following that it has been able to garner from its patrons, as evidenced from numerous positive reviews on sites like Yelp.com. However, it is only a matter of time before the market will price CHUY on par with some of its peers. We don’t think the company’s shares will be able to sustain the current trading price of over $30. It wouldn’t surprise us if CHUY ultimately settled in a trading range at half of its current price. As an overview, consider the following business metrics and how CHUY stacks up against other restaurant chains such as Texas Roadhouse (NASDAQ:TXRH), Brinker International, Inc. (NYSE:EAT), Bravo Brio Restaurant Group (NASDAQ:BBRG), Bj’s Restaurants, Inc. (NASDAQ:BJRI), Ignite Restaurant Group (NASDAQ:IRG), Cheesecake Factory (NASDAQ:CAKE), Red Robin Gourmet Burgers, Inc. (NASDAQ:RRGB), Ruby Tuesday, Inc. (NYSE:RT) and Fiesta Restaurant Group (NASDAQ:FRGI):

EPS Multiples Are High vs. Industry Peers’ Projected Performance and Multiples

CHUY’s lofty 49X forward EPS, based on the recent share price of around $33.00 and management’s 2013 EPS guidance of $0.66 to $0.69, is not sustainable.

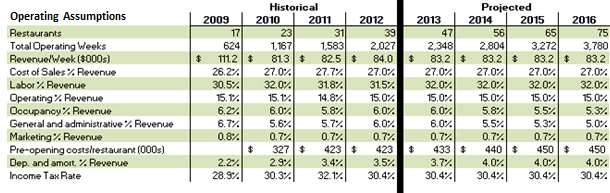

Our own modeling of CHUY’s business indicates modest EPS growth despite the anticipated increase in the number of restaurants from 38 to 75 by 2016. The modest EPS growth is due to CHUY’s high operating costs as a percentage of revenues. From 2009 to 2012, operating costs ranged from 90% to 93% of revenues.

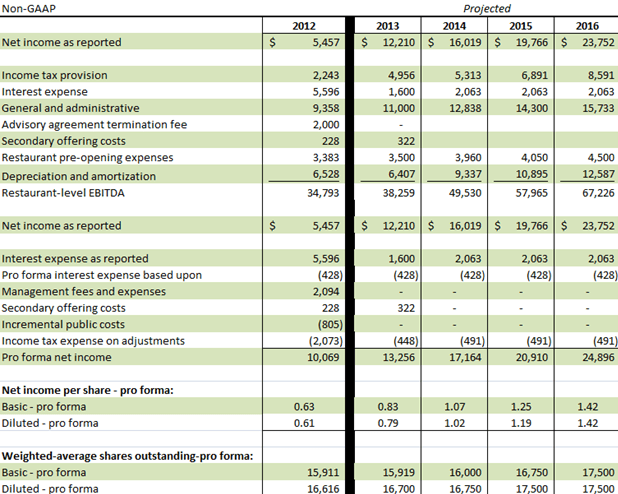

The following table shows our projections. Keep in mind that they do not fully account for risks such as increased food and labor costs, nor do they consider the prospect of future share issuances to raise capital to pay down debt that may accumulate as the company incurs capex for new restaurants (assuming around $2.4 million per restaurant). Overall, we were conservative in our assumptions, leading to a better bottom line growth profile than those communicated by analysts. But the conclusion is still the same; CHUY is trading well ahead of its growth.

Although the accuracy of future financial projections cannot be assured, CHUY’s business metrics are pretty well locked in and predictable to a great extent. However, as previously noted there are variables in the business model that will likely work out to be worse than one might logically assume today. For example, will the proposed increase in the minimum wage from $7.25 to $10 be approved? Even a lesser adjustment in the minimum wage would increase CHUY’s labor costs and negatively impact margins. Not only would CHUY’s direct labor costs increase but input costs for food and other consumables used in the business would increase as well. Of course the company could raise prices to offset higher costs, but that might reduce traffic given that the average check is already around $13 and has remained relatively stable in recent years. It is therefore inevitable that costs will rise over time, and we doubt the company has pricing power to fully offset increased costs.

CHUY’s $500+ Million Enterprise Value

Enterprise value, or EV, measures a company’s value based on market cap plus debt, minority interest and preferred shares, minus total cash and cash equivalents. This is the theoretical takeover price of the enterprise since an acquirer would have to take on and eventually pay the company’s debt, but would keep its cash. CHUY’s enterprise value is currently around $546 million based on the recent market price of $33 and projected shares outstanding for 2013 of around 16.7 million. In CHUY’s case debt and cash more or less offset one another.

The Ratio of Enterprise Value to EBITDA Far Exceeds Peers

CHUY is currently trading at 25X its EV/EBITDA while its peers trade at 8 to 12.5X. We are hard pressed to think of any market sector, other than perhaps biotech, that would trade at such multiples. Even if we use projected 2016 EBITDA, when CHUY will be operating twice as many restaurants, it will still have an EV/EBITDA ratio of 12X…and keep in mind that is three years down the road.

Enterprise Value per Restaurant Excessive

CHUY boasts an enterprise value of $15.6 million per restaurant based on $546 million EV divided by 35 equivalent/full year restaurants (assuming the 8 added in 2012 were operating for 6 months each). Management reports that EBITDA at the restaurant level is 20% of revenue which implies $1.0 million based on average revenue of approximately $5.0 million per location. That means investors are paying nearly 15X EBITDA for each restaurant. A truer measure of earnings per restaurant, though, would be achieved by factoring in unallocated corporate overhead costs that totaled nearly $15 million in 2012 or over $430,000 per location. Using an EBITDA/restaurant after allocating overhead costs yields $570,000 EBITDA/location meaning the market is really paying 25x EBITDA for each location. Either way, paying 15X or 25X EBITDA per location is excessive.

Enterprise Value/Cost per Restaurant

CHUY invests around $2.4 million in capex and over $430,000 in pre-opening costs for each new restaurant. So each new location costs $2.8 million to build, promote and get up and running. The market is currently valuing that investment at $15.6 million or over 5X the company’s average restaurant capex and startup costs. As points of comparison, consider the following EV/Cost per restaurant ratios; EAT (0.5), CAKE (1.5) and FRGI (2.2). What does CHUY possibly have that makes its restaurants so much more valuable than its peers’ establishments? We see nothing to justify such a valuation.

What would a Potential Acquirer Pay for CHUY’s Business?

To put CHUY’s current valuation into perspective, we looked at a recent transaction that took a restaurant chain private. P.F. Chang’s went private in early 2012 at an EV/EBITDA multiple of 8.5X. At that time, they received a 30% premium over the market price of the shares. P.F. Chang’s had 400 stores operating and averaged EBITDA/Store of $350,000, significantly less than the $570,000 EBITDA/Store (adjusted for overhead allocations) Chuy’s restaurants generate. P.F. Chang’s also had more infant revenue streams when it went private, including frozen food items made available in grocery stores and another restaurant chain.

Giving due consideration to its growth prospects, if we assume a higher 10x (EV/estimated 2013 EBITDA) valuation for CHUY, then with 16.7 million shares outstanding we calculate an enterprise value of $260 million and an implied share price of $15.00. Even if we use the 2016 forecasted EBITDA with the same assumptions we get an enterprise value of $429 million, implying a share price of $25.70, and that’s nearly three years from now. It seems a stretch given the risks inherent in the business model of any restaurant chain to assume CHUY can “grow” into its current valuation.

CHUY’s Principal Stockholders Exert Great Influence Over Corporate Matters and Transactions

Prior to the recent secondary offerings, Chuy’s was defined as a “controlled company”, meaning that is was not required to have an independent board because a majority of the shares were not aggregated in the public float. In fact, the board controlled the majority of voting shares. CHUY is no longer considered a controlled company after certain insiders and related parties sold 5,175,000 shares in a public offering made effective in January 2013. Although CHUY is no longer a controlled company, principal stockholders still influence significant control over the company. Cutting to the chase, what is in their best interest may not be in the interest of public stockholders. The following is from the Form S-1/A that became effective in January 2013:

“As of January 18, 2013, Goode Chuy’s Holdings, LLC, our controlling stockholder, and its affiliates, and MY/ZP Equity LP, which is controlled by our founders Mike Young and John Zapp, own approximately 49.6%, and 5.6%, respectively, of our outstanding common stock. Our controlling stockholder also has the right to vote an additional 1,340,791 shares of our common stock under a voting agreement entered into among us, our controlling stockholder, MY/ZP Equity LP and other stockholders, which will terminate upon consummation of this offering. Upon the completion of this offering and the termination of the voting agreement, Goode Chuy’s Holdings, LLC and its affiliates and MY/ZP Equity LP are expected to own approximately 25.6% and 2.9%, respectively, of our outstanding common stock, or 22.7% and 2.6%, respectively, if the underwriters’ option to purchase additional shares is fully exercised. Because Goode Chuy’s Holdings, LLC will collectively own less than 50% of the total voting power of our common stock, we will no longer be a controlled company within the meaning of the Nasdaq listing standards upon completion of this offering. See “Risk Factors–Although we will not be a controlled company within the meaning of the Nasdaq Marketplace rules upon the completion of this offering, during the phase-in period we may continue to rely on exemptions from certain corporate governance requirements that provide protection to stockholders of other companies.” However, as a result of their significant ownership and voting power with respect to our common stock, Goode Chuy’s Holdings, LLC and MY/ZP Equity LP will continue to have significant influence over corporate matters and transactions and may have interests that differ from yours. See “Risk Factors–Our Sponsor will continue to have significant influence over us after this offering, including over decisions that require the approval of stockholders, which could limit your ability to influence the outcome of key transactions. Our Founders may also continue to exert significant control over us.”

Principle Stockholders who effectively Control CHUY:

- Goode Partners

Goode Partners was co-founded by Joe Ferreira and David Oddi. Messrs. Ferreira and Oddi are also board members of Chuy’s. Mr. Ferreira is the Chairman of the Board, Treasurer, Chairman of the Compensation Committee, and on both the Audit Committee and Corporate Governance Committee. If he obtained the majority vote from the board he could then take control of Chuy’s or influence and even control the CEO through his role as Chairman of the Compensation Committee. Michael Stanley is the Vice President of Goode Partners and also serves on the board of Chuy’s.

- Three Star Management GP, MY/ZP IP Group, Ltd, Three Star Management, Ltd

Three Star Management (“TSM”) is an entity owned by Chuy’s co-founders John Zapp and Michael Young. Mr. Zapp is a Board Member, Chairman of the Corporate Governance Committee, and on the Compensation Committee. Mr. Young is also a Board Member, on the Audit Committee, Compensation Committee, and is also Chairman of the Corporate Governance Committee.

The Ability of Insiders and Related Parties to Influence Key Transactions Matters

It is human nature for people to do what is perceived to be in their own best interest (which may or may not be in your best interest). Given Chuy’s long operating history before the IPO and the influence that co-founders, insiders and other related parties had over the company and its operations, there is a long list of legacy transactions that are not in the best interests of CHUY’s current stockholders. The following is a list of such transactions imposed, as disclosed in the recent Form S-1A filing (descriptions of transactions available on pages 98 — 102 in filing):

“…

CERTAIN RELATIONSHIPS AND RELATED PARTY TRANSACTIONS

The following is a summary of transactions that occurred on or were in effect after January 1, 2009 to which we have been a party in which the amount involved exceeded $120,000 and in which any of our executive officers, directors or beneficial holders of more than 5% of our capital stock had or will have a direct or indirect material interest.

- Voting Agreement

- 2012 Stock Repurchase

- 2010 Stock Sale

- Purchase of Common Stock by our Executives

- Acquisition Related Transactions

- Stockholders Agreement

- Advisory Agreement

- Bonus Payments and Related Note Payable to Founders

- Purchase of Arbor Trails Restaurant

- Default License Letter Agreements

- Intellectual Property

- Recipe License Agreement

- Management Agreement

- Management System License Agreement

- Cross-Marketing License Agreement

- Parade Sponsorship Agreement

- Loan Agreement with our Chief Executive Officer

- Leases

- Settlement Agreement

- Indemnification Agreements”

…”

To illustrate our point further, the following are the particulars of two of the related party transactions listed above:

“…

- Loan from related party with excessive interest: TSM loaned Chuy’s Holding Inc. $1.7 million in September 2007 @ 15% interest per annum, amortized monthly. Over the 26 month term of the loan TSM collected $322,000 interest. That’s nearly $150,000 more than the company would have paid under their existing credit facility. See “Bonus Payments and Related Note Payable to Founders” listed above.

- Properties leased from related party at above market rents: TSM owns the building that Chuy’s leases for their headquarters and six of the “Heritage” Chuy’s Locations. The following from the recent Form S-1A filing noted above; “We lease our corporate office space as well as our North Lamar, River Oaks, Highway 183, Round Rock, Shenandoah and Arbor Trails properties from subsidiaries of Young/Zapp, a company owned 47.5% by each of our Founders and 5.0% by Sharon Russell. In 2012, we paid Young/Zapp $112,598, $229,912, $434,778, $490,676, $457,046, $288,476, and $308,548, which includes rent and a percentage of gross sales in excess of our base rent, with respect to our headquarters, North Lamar, River Oaks, Hwy 183, Round Rock, Shenandoah and Arbor Trails locations, respectively.

…”

Based on an average square footage per restaurant of 8,000 sq. ft., we can calculate that the $2.2 million paid to TSM for six restaurant locations in 2012 works out to $46.00/sq. ft. Separately, we derived that the rents paid for CHUY’s other locations averaged around $27.50/sq. ft. That means the company is paying related parties excess rent of as much as $18.50/sq. ft. Assuming 6 stores with 8,000 sq. ft. X $18.50/sq. ft., the company might be paying $888,000/year in rents over fair market price.

Company Intends to Implement Controls over Related Party Transactions — But the Horse is Already out of the Barn!

Now that CHUY is a public company management intends to adopt a written policy regarding related party transactions, but the horse is already out of the barn. Management’s noble declaration of intent to control related party transactions is no doubt due to heat from shareholders who are aware of the long laundry list of transactions. The following is from page 102 of CHUY’s recent S-1A filing:

“…

Related Party Transactions Policy

We intend to adopt a written policy relating to the approval of related party transactions. Our audit committee will review certain financial transactions, arrangements and relationships between us and any of the following related parties to determine whether any such transaction, arrangement or relationship is a related party transaction:

- any of our directors, director nominees or executive officers;

- any beneficial owner of more than 5% of our outstanding stock; and

- any immediate family member of any of the foregoing.

Our audit committee will review any financial transaction, arrangement or relationship that:

- involves or will involve, directly or indirectly, any related party identified above and is in an amount greater than $120,000;

- would cast doubt on the independence of a director;

- would present the appearance of a conflict of interest between us and the related party; or

- is otherwise prohibited by law, rule or regulation.

The audit committee will review each such transaction, arrangement or relationship to determine whether a related party has, has had or expects to have a direct or indirect material interest. Following its review, the audit committee will take such action as it deems necessary and appropriate under the circumstances, including approving, disapproving, ratifying, cancelling or recommending to management how to proceed if it determines a related party has a direct or indirect material interest in a transaction, arrangement or relationship with us. Any member of the audit committee who is a related party with respect to a transaction under review will not be permitted to participate in the discussions or evaluations of the transaction; however, the audit committee member will provide all material information concerning the transaction to the audit committee. The audit committee will report its action with respect to any related party transaction to the board of directors.

…”

In our view management is giving lip service to the issue of related party transactions. Those who personally benefit from the transactions have too much influence and control over the company for us to take management’s declaration seriously. If management truly wants to win the confidence of public stockholders we would suggest that they not only adopt the specified policies but also renegotiate some of the more material related party transactions that remain in force, starting with the leases with TSM for headquarters and six operating locations. Anything short of that will not sway our view that the interests of CHUY’s public shareholders are being trumped by the interests of insiders and related parties.

Other Issues

CHUY’s Unable to Use Chuy’s Brand in Nevada, California and Arizona

Reading RISK FACTORS in SEC filings might make most investors eyes glaze over. Many dismiss risks as unlikely events that public companies are forced to disclose. Investors might, however, want to take a look at CHUY’s risk factors detailed on pages 15 to 34 in a recent Form S-1A that became effective in January 2013. Among the disclosures is the following that notifies investors that the company may not use the brand “Chuy’s” in Nevada, California and Arizona. It seems to us that these are three prime states where CHUY’s should want a presence.

“…

“We may not be able to adequately protect our intellectual property, which, in turn, could harm the value of our brand and adversely affect our business.

Our ability to implement our business plan successfully depends in part on our ability to build brand recognition in the areas surrounding our locations using our trademarks and other proprietary intellectual property, including our brand names, logos and the unique ambience of our restaurants. We have registered or applied to register a number of our trademarks. We cannot assure you that our trademark applications will be approved. Also, as a result of the settlement agreement with an unaffiliated entity, Baja Chuy’s, we may not use “Chuy’s” in Nevada, California or Arizona, which may have an adverse effect on our growth plans in these states. Additionally, our brand value may be diluted as a result of their use of “Chuy’s” in these states. Third parties may also oppose our trademark applications, or otherwise challenge our use of the trademarks. In the event that our trademarks are successfully challenged, we could be forced to rebrand our goods and services, which could result in loss of brand recognition, and could require us to devote resources to advertising and marketing new brands.

…”

Conclusion

We have deep concerns about the valuation the market has placed on CHUY. The stock has recently been trading in the low $30 range, representing an unsustainably lofty 49X estimated 2013 EPS with EV that is 25X EBITDA.

As indicated in our report, insiders seem to agree that CHUY is overvalued and are dumping the vast majority of their holdings. According to the last 2 S-1 filings insiders have gone from owning 62.6% of company shares as of December 2012 to as little as 9.9% following the latest offering. As we have said, there is nothing wrong with insiders cashing in on their investments, but the magnitude of their exodus only gives us more reason to be bearish on CHUY at these very lofty valuations.

We are also concerned about obvious risk factors such as increased labor costs driven by an inevitable upward adjustment in the minimum wage. The only questions are when and by how much labor costs go up. Investors should note that increased wages will not only impact direct labor costs but other input costs for food and other consumables used in the business. We don’t believe the company has the pricing power to offset increased costs because of headwinds facing the economy as a whole, including the greater share of customers’ paychecks going to social security taxes and higher gas prices.

Furthermore, we think investors should be realistic about CHUY’s growth prospects. Management has the capacity to add 8 or 9 restaurants per year at capex cost of around $2.4 million and pre-opening costs of over $430,000. Cash flows from operations and a $25 million revolving credit facility will only take them so far.

Finally, both the number and nature of material related party transactions disclosed in CHUY’s SEC filings are troubling. The company had a long and successful history before it went public; insiders and related parties took care of themselves. Nobody can really fault them for that. Chuy’s, however, is now a public company and the scrutiny and rules regarding such transactions and relationships are clear. Frankly, we think many of the related party transactions disclosed in the company’s SEC filings should have been renegotiated or even terminated as part of the IPO process. We acknowledge that management intends to issue a written policy concerning related party transactions, but that strikes us as only lip service. One can’t help but sense that the interests of management and insiders are not totally aligned with those of public shareholders.

We can only conclude that CHUY is grossly overvalued based on its fundamentals, risk factors inherent in any restaurant chain’s business model and the apparent reluctance of insiders to let go of some of the privileges and benefits they enjoyed when Chuy’s was a private company. We believe that following the insider exodus it’s only a matter of time until the shares are marked down to more reasonable and sustainable levels.

Disclosure: Short CHUY

Disclaimer:

You agree that you shall not republish or redistribute in any medium any information on the GeoInvesting website without our express written authorization. You acknowledge that GeoInvesting is not registered as an exchange, broker-dealer or investment advisor under any federal or state securities laws, and that GeoInvesting has not provided you with any individualized investment advice or information. Nothing in the website should be construed to be an offer or sale of any security. You should consult your financial advisor before making any investment decision or engaging in any securities transaction as investing in any securities mentioned in the website may or may not be suitable to you or for your particular circumstances. GeoInvesting, its affiliates, and the third party information providers providing content to the website may hold short positions, long positions or options in securities mentioned in the website and related documents and otherwise may effect purchase or sale transactions in such securities.

GeoInvesting, its affiliates, and the information providers make no warranties, express or implied, as to the accuracy, adequacy or completeness of any of the information contained in the website. All such materials are provided to you on an ‘as is’ basis, without any warranties as to merchantability or fitness neither for a particular purpose or use nor with respect to the results which may be obtained from the use of such materials. GeoInvesting, its affiliates, and the information providers shall have no responsibility or liability for any errors or omissions nor shall they be liable for any damages, whether direct or indirect, special or consequential even if they have been advised of the possibility of such damages. In no event shall the liability of GeoInvesting, any of its affiliates, or the information providers pursuant to any cause of action, whether in contract, tort, or otherwise exceed the fee paid by you for access to such materials in the month in which such cause of action is alleged to have arisen. Furthermore, GeoInvesting shall have no responsibility or liability for delays or failures due to circumstances beyond its control.