Welcome to The GeoWire , your Source for a Peek into GeoInvesting’s Research Coverage, Microcap Stock Education, Case Studies, Recommended Reading From Around the Web, Important Tweets of the Week, Premium Weekly Wrap Ups, Featured Videos, and More. Please hit the heart button if you like today’s newsletter and reply with any feedback.

If you are new or this was shared with you, you can join our email list here. Or you can click here to get all of our premium content.

When you think of individuals such Carl Icahn, Ronald O. Perelman and Nelson Peltz, you might think of their knack for business acumen, successful fund management and even philanthropy. However, there is one aspect of these personalities’ exploits that might get overshadowed by the overarching themes of their achievements – a specialty in turning businesses around.

The reason it is a specialty is because not everyone has the means or frankly, the guts, to put plans in place to take a failing company and turn it around.

Last week’s foray into the world of executives and portfolio managers at activist fund 180 Degree Capital Corp. (NASDAQ:TURN), Kevin Rendino (CEO) and Daniel Wolfe (President), touched on the reasons why companies consider and ultimately agree to shift the innards of their businesses around. In the end, it really comes down to making them attractive enough for investors to put their money into. We’d suggest that you catch up with that column after reading what we have lined up today.

So, speaking of turnaround specialists, we wanted to bring attention to a few famous ones who excelled at buying or taking a stake in underperforming or struggling companies to try to help them achieve profitability in various ways.

Carl Icahn

We all know Carl Icahn for his activist approach to investing and his role as a turnaround specialist. He also has no problem going head to head with other famous investors like he did when dueling with Bill Ackman who was short Herbalife Nutrition Ltd. (NYSE:HLF). Icahn runs his activism through Icahn Enterprises L.P. (NASDAQ:IEP).

One of Icahn’s most notable early investments was in the airline company TWA (Trans World Airlines), previously owned by Howard Hughes

Carl Icahn was viewed as a corporate raider in the TWA deal because of his aggressive tactics in acquiring a controlling stake in the company and his focus on short-term gains for himself and his investors rather than the long-term health of the company. Basically, a greedy approach, or as Michael Douglas might say…

In 1985, Icahn launched a hostile takeover bid for the company, which he eventually succeeded in acquiring for $469 million.

He bought multiple smaller regional carriers to leverage the airline’s increased size for greater profitability. By 1988, Icahn used a $650 million stock-buyback plan to take TWA private.

However, this move also burdened the company with $540 million in debt. Subsequently, TWA’s most valuable routes were sold to competitors, resulting in the company’s weakened state and eventual filing for Chapter 11 in 1992.

Icahn resigned from his position at the company the following year.

Icahn’s actions were controversial and even though his mission was to reduce costs, improve efficiency, and modernize the company’s fleet during his tenure, they led to significant job losses at TWA as well as a decline in the airline’s overall profitability.

His reputation as a corporate raider was further cemented by his aggressive tactics in other corporate takeovers, including his hostile takeover of USX Corporation (now known as United States Steel Corporation) in 1986.

Although TWA was an ultimate bust of a turnaround, when looking at some of the aspects of the company’s original goals and applying them to what we do in the microcap world, especially when dealing with the BigCapMicro theme we’ve been talking about lately, we’re drawn to the modernization aspect of the story.

We find that many of these companies get comfortable with the status quo and require a new management team or activist to bring a company up to date in terms of technology and product development.

Operational and product modernization are great ways to improve margins internally through running a more efficient ship and offering new, higher margin products to current customers and finding new customers.

Ronald O. Perelman

Ronald O. Perelman was an American businessman, investor, and philanthropist who was best known for his role in the turnaround of cosmetics giant Revlon in the 1980s before the company went public (1996).

When he orchestrated the turnaround of the financially struggling Revlon in a deal that made headlines around the world, Perelman used junk bonds to acquire a controlling stake in the company in a leveraged buyout. He then set about revamping the company’s product line and repositioning it in the marketplace, which eventually led to a significant increase in profits.

While it did take the company several years to make a turnaround as a result of debt load stemming from Perelman’s purchase of the company, the company eventually turned a profit in 2007.

Perelman’s success with Revlon made him a legend in the business world, and he went on to achieve even greater success in the years that followed. He also invested in a number of other companies, including the cosmetics brand Elizabeth Arden and the entertainment company Marvel Comics.

However, it seems things have come full circle for Revlon, Inc. New (OOTC:REVRQ). The company is once again facing troubles and is currently in bankruptcy proceedings. Too bad Perelman is not around to help them this time around, as he passed away in 2021

The Chapter 11 restructuring theme is one we’ve been discussing lately since we want to capitalize on instances where companies may be entering bankruptcy during a tougher operating environment, but can come out of the restructuring in better shape. You can see our last post on this subject here.

Nelson Peltz

Nelson Peltz is an American billionaire businessman and investor who is known for his work as a turnaround specialist in the consumer goods and food industries.

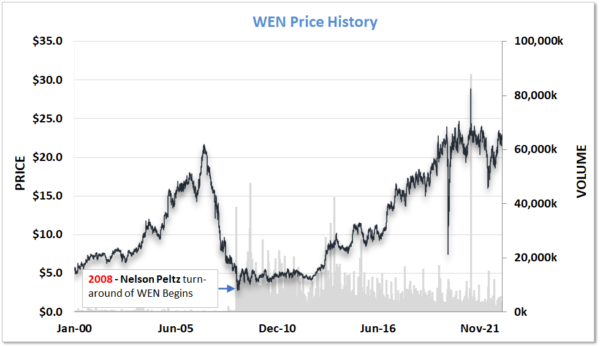

One of Peltz’s most notable investments was in the fast food company The Wendy’s Company (NASDAQ:WEN). Peltz successfully pushed for changes in the company’s management and strategy. Under his leadership, Wendy’s streamlined operations in 2008, improved its marketing, and invested in new menu items, which helped turn the company around and generate strong growth and profits.

As a result of Wendy’s financial performance improvements, the company’s stock price increased from a low of $2.63 in 2008 to today’s price of around $23, or 774%.

The value of Peltz’s investment in Wendy’s is estimated to have increased by several hundred million dollars.

Interestingly, Meritage Hospitality Group Inc (OOTC:MHGU) has been in our model portfolio since June 2015. MHGU‘s original business plan centered around acquiring under-performing Wendy’s locations and turning them around by modernizing the technology around ordering and inventory management, as well as upgrading the menu.

Today, the company has expanded its restaurant expertise to launch restaurant concepts outside of Wendy’s focus.

Another Expert’s Perspectives on Turnaround Strategy

The above investments required a combination of strategic thinking, operational expertise, and a willingness to take calculated risks, which helped turn around struggling companies and generate substantial returns for investors.

In fact, David Ratner, the CEO of cyber security company HYAS and an expert in company turnarounds, appeared on a podcast by SBI TV to share his insights on how a turnaround CEO diagnoses problems that a company faces and why it is failing:

He explains that there is no one turnaround playbook, no formula that can be applied to all failing companies.

He conveys that the key to identifying the root causes of a company’s problems is to embed yourself into the organization – attend the meetings, talk to the employees, sit in on customer visits, and observe the organization from top to bottom.

He then uses a combination of the data he gathers from his exposure to the company and his intuition to identify the underlying causes of the company’s problems and to determine the steps to take to facilitate a successful turnaround.

So, in the end, it’s clear that the specific amount invested by an investor is not always the most important factor in determining the desired outcome.

The Investor’s strategy, operational expertise, and ability to effectively implement changes in the company can be just as important, if not more so, in determining the success of the investment.

Hi, part of this post is for paying subscribers

SUBSCRIBE

Already a paying member? Log in and come back to this page.

Our premium members also…

Get Access all Model Portfolios

Receive GeoInvesting Premium Alerts

Access to all stock pitches and Research Reports

Attend live interviews and fireside chats

Interact with the GeoTeam in Monthly Forums

Get in-depth stock research on 1000’s of microcap stocks

Thanks for joining thousands of other investors who follow GeoInvesting

Your free subscription includes first access to:

- Monthly publication of “The GeoWire” Newsletter sent to you the first Tuesday of every month, covering case studies, stats and fireside chats.

- Weekly emails highlighting the past week’s coverage at GeoInvesting sent 3x a month.

Get more out of GeoInvesting by trying us our premium package for free.

Step 1 – Receive quality research investment Ideas, model portfolios and education

Step 2 – Interact with us about our favorite ideas and the research that supports it; gain insight through all tools geo offers

Step 3 – Decide to build portfolios based on our research and Model Portfolios and updates including convictions, additions and removals of holdings.