If you are a premium member make sure you sign in to see All the exclusive content In This Issue.

This week’s Microcap Information Arbitrage Weekly Wrap-Up is ready — spotlighting the most important developments across our 1,500+ microcap coverage universe built since 2009, including high-impact earnings reports, information arbitrage discoveries, contract announcements, and model portfolio updates. We also highlight insights from our investor and CEO interviews (Skull Sessions).

See all emails sent during the week here.

The feature highlight last week was a Fireside Chat Skull Session we hosted with Rhone Resch, Chief Strategy Officer of Toyo Co., Ltd (NASDAQ:TOYO), co-moderated and led by GeoInvesting Research contributor “Jev” (@MicrocapDr), covering surprisingly positive Q1 earnings results, the competitive advantage it has vs comps like First Solar, Inc. (NASDAQ:FSLR), the company’s plans to expand capacity to scale production, and the unique risks involved with investing in the solar industry. Can we see a re-rate in the company’s low P/E ratio?

This week, I also had my usual small-cap earnings review where Sebastian Krog (@treasurehunting on Substack; @SebKrog on X), Diego La Torre (@Diego_La_Torre_) and I went through 10 of our favorite small-cap and microcap names from the Q1 earnings season. We also made sure to cover the main risks in each case.

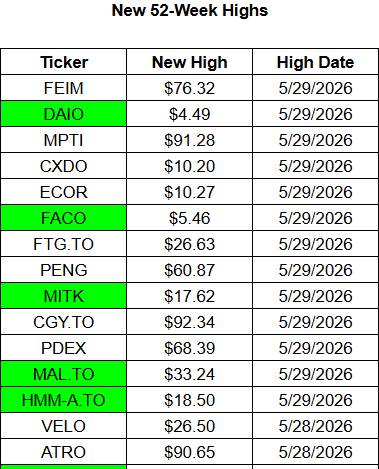

Moving on, as usual, we highlight the stocks we want to watch most in our big movers and losers list of the week, included at the end of this post. We’re searching for stocks gaining momentum for all the right reasons and for those that are falling for all the wrong reasons.

For example:

The full list of tables and “green” highlights are available at the end of this post.

Stocks discussed at Geoinvesting last week:

Feature Stocks (from webinar with Sebastian Krog): SIF FALC BIRMF (TSXV:BRM) CVU ICCC LEAT TZOO NDLS FECCF (TSX:FEC) IDXG

Research Screen Updates: WEBC added to Data Center Screen

Earnings: WEBC OOMA MOV OLNCF (TSXV:OML)

InfoArb Tear Sheets: LEAT BWEN SYZLF (TSX:SYZ) ACCS IPM ARKR SGRP BIRDF (TSX:BDT) ALT CLPT KSIOF (TSX:KSI) TGEN DERM ITMSF (TSX:IMP) MDXH AMPG OBGRF (TSX:OGD) SWAG ROMJF (TSXV:ROMJ) AMAT CLBT NINE BKTI CURI LGCY RCEL FTLF IFABF (TSX:IFA) NTWK NSYS INLX DAIO XBP XELB AMS FSI CREX KLNG HKHC IRIX EDUC TATT CVALF (TSXV:COV) VNPKF (TSX:NPK SEED YTRA OLNCF (TSXV:OML) APEUF (TSX:AEP)

Skull Sessions: Fireside Chat with TOYO Management, moderated by Geoinvesting Subscriber and Research Contributor, “Jev” (@MicrocapDr).

Feature Highlight From Our Microcap Coverage Universe

Last Thursday, during our May 2026 Small Cap Earnings Review, Sebastian Krog (@treasurehunting on Substack; @SebKrog on X), Diego La Torre (@Diego_La_Torre_), and I went through a group of small-cap and microcap stocks that we found particularly interesting during the Q1 2026 earnings season.

Sifco Industries, Inc. (NYSE:SIF) (aerospace metal forgings)

- Q2 2026 Revenue: $26.4 million vs $19.0 million

- Q2 2026 EPS: $0.43 vs loss of $(0.23)

I opened with SIF, which is probably one of my favorite aerospace turnaround names right now. Recall that we just added the stock to our Focus Model Portfolio based on a breakout earnings report. The company has been around for a long time, but after years of losses and stalled revenue, the inflection finally looks real.

Gross margins expanded sharply, earnings have flipped positive, backlog is growing, and the defense/aerospace setup gives us a real reason to believe the momentum can continue. You can see the full report on Geoinvesting here.

Falconstor Software, Inc. (OTCID:FALC) (data backup software)

- Q1 2026 Revenue: $4.3 million vs $2.5 million

- Q1 2026 EPS: $0.12 vs loss of $(0.06)

I also talked about FALC, a company that is starting to show the payoff from its move toward recurring revenue. The quarter was strong, with revenue and earnings moving in the right direction, and with a run-rate P/E of 6.0x, the stock still looks inexpensive for a software name. The big caveat is the preferred stock structure and ownership overhang, but if investors get more comfortable with that, this could be an interesting rerating story.

Biorem, Inc. (OOTC:BIRMF) (TSXV:BRM) (air pollution control systems)

- Q1 2026 Revenue: $6.8 million vs $4.7 million

- Q1 2026 EPS: $0.01 vs $0.00

Another name I highlighted was BIRMF, which has a strong backlog and a cleaner balance sheet. The business can be lumpy because much of its revenue is project-driven, but we like the growing recurring revenue opportunity tied to dry scrubber and filter replacement products, which is slowly becoming a very significant piece of the company’s contract bid book. If that recurring piece keeps building, the market may start to re-rate BIOREM’s P/E.

Cpi Aerostructures, Inc. (NYSE:CVU) (aircraft structures)

- Q1 2026 Revenue: $17.4 million vs $15.4 million

- Q1 2026 EPS: $0.09 vs loss of $(0.10)

I also brought up CVU, another aerospace turnaround, though I’m less confident in this one than SIFCO. The setup is similar in some ways: margins are improving, a bad contract appears to be fading from the numbers, and the aerospace backdrop is favorable. But CVU still has more risk tied to liquidity, customer concentration, and the large unfunded backlog. Two of the last three earnings reports have been really strong. I think if we see one more, we can probably assume that the turnaround has shifted to a different level that might be more consistent.

Immucell Corporation (NASDAQ:ICCC) (animal-health biologics)

- Q1 2026 Revenue: $10.4 million vs $8.1 million

- Q1 2026 EPS: $0.21 vs $0.16

Diego jumped in with an analysis on ICCC. The story got cleaner after the company killed its cash-burning Re-Tain program in December 2025 and went all-in on First Defense, its profitable scours-prevention product. Q1 was strong, with sales up 28% and EPS of $0.21, putting it near 12x run-rate, but management guided to softer coming quarters.

A quality microcap with real tailwinds (calf values up sharply, capacity expansion underway), but we saw it as roughly fairly valued after a big run. This is a name we are keeping on our watchlist; it could be interesting if the stock pulls back on softer Q2 numbers.

Leatt Corp. (OTCQB:LEAT) (motorcycle protective gear)

- Q1 2026 Revenue: $19.5 million vs $15.4 million

- Q1 2026 EPS: $0.27 vs $0.17

Sebastian started with LEAT, which we both know well and is a stock that could easily move into the favorite category for Geo. The company has moved from being mostly a motocross/neck brace story to a broader head-to-toe protective gear company, with motocross, mountain biking, and now ADV motorcycle gear. The big point is that LEAT may be able to exceed its old COVID-era revenue peak because the product base is broader today, the balance sheet is loaded with cash, and the company has a buyback in place.

Travelzoo (NASDAQ:TZOO) (travel deals)

- Q1 2026 Revenue: $24.3 million vs $23.1 million

- Q1 2026 EPS: $0.23 vs $0.26

He then discussed TZOO, which is an interesting earnings inflection story tied to the shift from an advertising model to a recurring paid subscription model. The accounting made the transition look ugly at first because customer acquisition costs hit the P&L upfront while subscription revenue gets recognized over time. Now that renewals are starting to come through, the model should look better, but we still have concerns around governance and whether the market will give it a full multiple.

Noodles & Company (NASDAQ:NDLS) (fast-casual restaurant chain)

- Q1 2026 Revenue: $123.8 million vs $123.8 million

- Q1 2026 adjusted EPS: loss of $(0.44) vs loss of $(1.59)

Sebastian also brought up NDLS as more of a special situation than a classic growth story. Bruce Galloway is involved, the company is in a strategic alternatives process, and management is working through restaurant portfolio optimization. The upside would likely come from a sale, refinancing, or some other action that helps unlock value from a business that has already shown improved EBITDA.

Frontera Energy Corporation (OTC:FECCF) (TSX:FEC) (oil and gas)

- Q1 2026 Revenue: $26.8 million vs $25.1 million

- Q1 2026 EPS: $0.18 vs $0.14

He also covered FECCF, which is becoming more of an infrastructure story after the sale of its Exploration and Production (E&P) business. Once the expected special dividend is paid, the remaining company should mainly be tied to a Colombian pipeline stake and the Puerto Bahia port. The market may still be treating it like an oil company, but the remaining asset base could attract a different investor base if the cash flow profile becomes easier to understand.

Interpace Biosciences, Inc. (OTCID:IDXG) (cancer diagnostics): Still profitable after losing reimbursement tied to one of its prior tests, with the current focus on the remaining cancer diagnostic testing portfolio.

- Q1 2026 Revenue: $9.0 million vs $11.5 million

- Q1 2026 EPS: $0.03 vs $0.06

Sebastian closed with IDXG, which has been in rebuild mode after losing reimbursement support tied to one of its prior tests. That hit the old revenue base and hurt the stock, but the company still has other diagnostic tests, has cut costs, cleaned up the balance sheet, and is guiding for growth from the remaining business.

The reason it is interesting is that IDXG still looks inexpensive for a profitable diagnostics company if the remaining tests can grow, but the reason we have to be careful is just as important: this is still a narrow-product story, and any reimbursement issue or test-specific disruption can have an outsized impact.

You can watch the full discussion here.

Inside this Week’s Report:

- Research Screen & Model Portfolio Updates

- Earnings Reports Worth Monitoring

- Latest InfoArb Tear Sheets

- Skull Sessions

- Coverage Universe Stats: Big Movers & Losers and New Highs & Lows

research Screen Updates

——

Sorry, the full post is only available for paying subscribers. If you are already a paying subscriber, please make sure you are logged in. To become a paying subscriber please click on the link below

(We also offer a new very popular monthly subscription option).

gain Exposure to our expanded coverage on Our 1500+ Microcap Universe, Subscribe below.

200+ multibaggers and counting

GeoInvesting is a premier research platform for microcap investors, dedicated to uncovering high-potential stock ideas in undervalued companies across various sectors. With over 30 years of investing experience, GeoInvesting has covered more than 1,500 equities, providing often actionable proprietary research. The platform has been instrumental in identifying 200+ multibagger stocks, and offers investors exclusive access to over 600 management interview clips, allowing for deeper due diligence and understanding of the microcap stocks, many of which make it to market-beating premium Model Portfolios. Join the GeoInvesting community for the best stock research and microcap insights to help you stay ahead in the market. To learn more about our Premium Services, go here.. (https://geoinvesting.com/premium-research/)