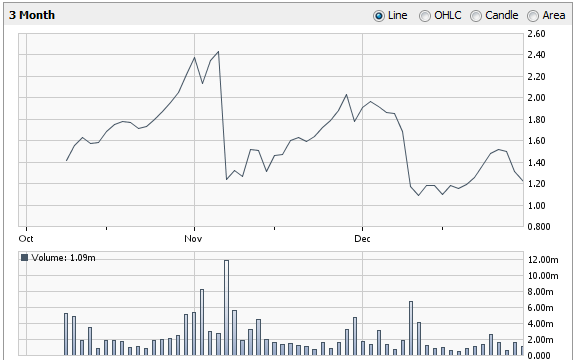

The Raystream (OOTC:RAYS) story has it all – a too good to be true product, excessive company sponsored paid promotional campaigns and ties to promoters of other companies that have been pumped before they were dumped. The stock has gone from $1.00 to $2.51 at its high since completing its “corporate restructuring” on October 4, 2011 and has already been exposed by two well-known research sites: The Street Sweeper (Dec. 1) and PumpsandDumps.com (Dec. 5). We also believe that TimothySykes.com views the RAYS story in negative light.

RAYS 3 Month Chart

We believe that RAYS is worth no more than what it would claim as a shell company or at most about $0.004 to $0.01. ($200k to $500k divided by 50M outstanding shares). Even when applying RAYS’s claimed shareholder equity (which virtually consists solely of goodwill) as shown its October 2011 10Q, a price target of just $0.19 can be derived.

Some of the red flags which you may already be aware of and others that have certainly flown under the radar:

Raystream’s Technology is not a Secret

The company’s claims of a proprietary high definition video compression technology, related to AVC/H.264 video codecs, are flat out misleading. In fact, it is and has always been available as free and open-source software on other sites. Furthermore, RAYS claims “No other company specializes in HD compression technology.” To verify Raystream’s claims, we decided to do a simple web search. As expected, we found several companies that specialize in HD video compression technology.

Excessive Promotion

Raystream has spent millions of dollars on a self-promotion campaign just to disseminate details of its story. Over a dozen sites have joined the pump train to fuel what we believe is a sensationalistic campaign designed to dupe investors who are none-the-wiser about exactly how ubiquitous the technology really is. In fact, Go Daddy suspended the Smauthority.com domain, a pumper for RAYS.

The Usual Suspects

The people involved with Raystream include a cast of characters that have had a long and lurid history with rogue development stage companies that eventually failed. The same people are continually tied to one another with each new venture. (Evidence to be sent to SEC Task Force.)

Dilution Imminent

Investors are likely to get slammed with massive dilution due to Raystream’s need for capital. RAYS admits it will have to raise funds within the next 3 to 12 months, depending on which SEC filings are referenced, just to sustain operations.

Loss of Customers

Exactly who are Raystream’s customers? We contacted one of three alleged RAYS customers only to find out that it no longer has a relationship with RAYS? Does this sound like someone who was excited about a technology that would revolutionize the way things are done?

RAYS has no problem name-dropping when it comes to large players like Netflix Inc.(NASDAQ:NFLX) and YouTube possibly lining up to use their product, but they fail to recognize that these and other notable names are already AVC/H.264 licensees, as you will learn.

Investors who have placed long bets on Raystream (OTC:RAYS) should know that the SEC is stepping up its efforts to get in front of pump and dump schemes taking place on U.S. shores…

Dec. 20, 2011

SEC Charges California Company, Co-CEOs, and Attorney in Series of Fraudulent Schemes Pumping Company Stock

[…] Mitchell J. Stein was controlling most of the company’s business activities, hiring promoters to tout Heart Tronics stock on the Internet, and reaping nearly $8 million from secret trades that he orchestrated unbeknownst to investors. […]

Dec. 16, 2011

SEC Charges Daniel “Rudy” Ruettiger and 12 Others in Scheme to Pump Stock in Sports Drink Company

Some issues referenced in this case include:

- False and misleading statements in press releases, SEC filings, and promotional materials

- A product claimed to be “something special” and to outperform the other competitors

- Selling unregistered shares to investors

- Panamanian companies that sold shares during the scheme

- A person who has inspired a motion picture (Daniel Ruettiger)

In addition to the fact that RAYS has not disclosed that is has already lost one of its three alleged customers, we could not help notice the parallels that each one of the points above has with the RAYS case.

False and Misleading Statements

Again, RAYS clearly stated in its SEC filings that “No other company specializes in HD compression technology.” We found this to be false.

Special Product

RAYS is portraying itself to be a pioneer in video compression when it is in fact relying on already existing technology.

Unregistered Shares / Convertible Loan

On September 19, 2011 after only two months of possession of its loan and with essentially no trading market for RAYS shares, Unlimited Trade (largest and newest shareholder) opted to convert its loan into 5 million (unregistered) shares of common stock at $0.40 (equal to $2 million or the amount of their original loan), well below the going market price of RAYS at the time.

Famous Character

There was a movie made about Tan Siekmann, an individual tied to Unlimited Trade, Raystream’s largest shareholder. Siekmann’s past is checkered with failed businesses, one of which eerily shows characteristics of a pump and dump scheme of its own.

Panamanian Company Ties

Information on Panama-based Unlimited Trade brings to light questionable share transactions seemingly structured to line the pockets of various parties.

While other truth seekers have already touched upon the RAYS story, we have gone a step further to point out information that investors MUST read to learn about the web of deceit constructed by RAYS and certain parties. Because we know that RAYS will continue to assault the public with information on its role in “revolutionizing” video compression technology, we intend to go step for step with the company so they cannot escape the legal consequences of their actions.

What now?

So now it seems that the jig is up for RAYS. Of no surprise, one of the company’s only three named “customers” (not clear whether or not they are paying) has already severed ties with them, as discussed later. It appears that the company’s large campaign to inform investors of a “proprietary” and “revolutionary” technology, claimed to have the ability to compress video like never seen before, has finally backfired on them. Investigations into the morality and intentions of their dealings, present and past, has uncovered disturbing truths and historical events shady enough to make even the most risk-tolerant investors run for the hills.

In a revealing commentary, The Street Sweeper released a column that discussed questionable business practices, delving into RAYS’ botched and weak attempt to fool what they obviously thought were naïve investors, presenting to them a product put together from free and open-source software and calling it their own. PumpsandDumps.com counted twelve stock promoting sites that were engaged in touting RAYS, but something tells us that this number is conservative.

The Street Sweeper’s article also covered a brief look into the intertwined cast of characters charged with molding the RAYS fraud into what it is today and the cast’s evident conflicts of interest in doing so. We decided to go a step further and uncovered eye-opening instances of recurring relationships tied to failed ventures and brazen pumps.

The fact that GeoInvesting was concurrently looking into RAYS speaks volumes to the extent of the “company’s” pump tactics. In fact, on October 21, 2011 we stated on one of our premium blog pages (Open Short Positions) that we were already short RAYS.

What follows is our assessment on RAYS, an effort to supplement the research of prior authors with additional information.

Going Public Details

The history of RAYS is quite brief.

November 4, 2010

A “real estate development company”, Interdom (stock symbol prior to RAYS:ITRD), with no revenues went public through an S-1 filing. Interdom Corp was incorporated by Igor Rumiantsev in Nevada on December 8, 2009 with an authorized share count of 75,000,000. Interdom never progresses with its strategy but still has an asset as a public vehicle.

June 14, 2011

A change in the control of Interdom occurred when Igor Rumiantsev sold all of his 3,500,000 common shares (83.8% of the Company’s outstanding and issued common stock) for $200,000 in a private share purchase transaction toUnlimited Trade Inc.

The Raystream Connection is Born

On the same day (and SEC filing) Igor Rumiantsev resigned and Interdom appointed Roman Rumpf as its new President, CEO, Principal Executive Officer, Treasurer, CFO, Principal Accounting Officer, Secretary, Treasurer and as Director.

The 8K filing offers the following biographical information about Roman Rumpf:

Currently, Mr. Rump is the general manager of Raystream GmbH, a private technology company, a position he has held since March 2011. From April 2010 to February 2011, Mr. Rump worked as a technical consultant at Elogic GmbH, a private electronic FX Trading company. From March 2008 to March 2010, Mr. Rumpf worked as Head of Development for Burg Lichtenfels GmbH & Co. KG, a private IT-Security company. From June 2006 to February 2008 Mr. Rumpf was Project and Product Manager at Qnective Inc. a private Social Networking company.

Note: GmbH is the German equivalent of LLC.

We’ll examine this information later. For now, just remember the bold items in the excerpt above and note that this is the first time (June 14, 2011) that the name “Raystream” was referenced.

On July 12, 2011

The company appointed Brian Petersen to executive positions.

On July 18, 2011

As its new controlling shareholder, Unlimited Trade lent the company $2 million via a convertible loan, due in July 2013, (we will revisit this item). (Related party loan) (see July 21 8k)

On August 22, 2011

Interdom completed a 37 for 1 forward split and changes its name to Raystream as it prepares for the inevitable acquisition of Mr. Rumpf’s affiliated company, Raystream GmbH.

On September 19, 2011

Raystream Inc. acquired Raystream GmbH in a ZERO cash transaction using 20 million shares as consideration.

Also on September 19, 2011 after only two months of possession of its loan and with essentially no trading market for RAYS shares, Unlimited Trade (largest and newest shareholder) opted to convert its loan into 5 million (unregistered) shares of common stock at $0.40 (equal to $2 million or the amount of their original loan), well below the current going market price of RAYS.

Let the Pumping Begin

On October 4, 2011 RAYS issued its first press release.

After trading a combined volume of 5 thousand shares in recent trading sessions prior to this release, volume exploded to 5.2 million shares on October 10, 2011 and never looked back.

Shortly thereafter, the company sponsored a $3.25 million promotion campaign.

This story smells of a classic shell game. Take control of a public shell and develop a “sexy” business plan. Next, enter into a related party convertible loan where potential shares will cover the cost of the “riskless” loan that you essentially control. Next, instead of having to spend cash which the company does not have, the company purchases non-patented “ground breaking technology” from (Raystream GmbH) using stock, where the R&D capital has allegedly been spent. Finally, create enough trading volume to sell your unregistered shares. At the stocks high the company’s convertible loan shares were valued at $12.5 million. This easily covers the cost if the $3.25 million promotional campaign. Better yet, the 20 million shares that were so graciously given to Raystream GmbH were worth $50.2 million. Not a bad day for a company with essentially no revenues.

What Happens Next?

Ultimately, we surmise that the stock will plummet:

- as investors realize that RAYS may not be what it purports itself to be.

- as investors realize that even if some legitimacy exists, the company will have to tap the equity markets.

- if the company just goes dark after selling its convertible shares and the promotional capital dries up.

As you will read later in the report and what has not yet been discussed by other authors, RAYS admits it will have to raise funds within the next 3 to 12 months, depending on which SEC filings are referenced, just to sustain operations. This deadline is approaching fast and has likely accelerated now that it has a “revolutionary”, unpatented product to market. At best, substantial dilution, an investor’s worst enemy, is around corner and should continue well into the future. Investors who purchase RAYS shares now could soon be blindsided with an equity offering and a sharp hit to the share price.

These are some of the Red Flags encompassing the RAYS story, often shared by other P&D’s:

- Sexy story,

- Possible exaggeration of “proprietary’ product function or technology,

- Insignificant customers relations

- Promotional activities

- Usual Suspects of fraudulent accomplices

- Dilution

Claims of a “Disruptive Technology”

Rays is a small development stage software company founded on March 21, 2011 which allegedly owns a “proprietary” ground breaking online video compression technology. According to their website this “technology drastically decreases bandwidth costs by reducing the file size of HD videos up to 90 percent, with an average of approximately 70 percent, and with no loss in clarity or quality — so they can be streamed online without buffering or stopping.”

According to a recent article by Streetsweeper.com: RAYS of Sunshine … or Clouds of Doom?

They appear to be selling open-source software — available at no charge — to anyone who wishes to use it. That software, known as “x264,” can be downloaded here for free” which is given away as shareware.

While we are by no means video technology compression experts, it was easy enough to substantiate Street Sweeper’s claims that the x264 encoder (one of the many implementations of the proprietary H.264 format) used to compress video is “free and open-source software” (defined) licensed as GNU GPL. Just follow this link you can clearly see that the technology can be characterized as such.

Even more startling is there is a list of companies that have already registered as licensees to use AVC/H.264 — some of which are the same companies named in the P&D material that claims they will be lining up to become RAYS customers! Among them are Netflix and Google (NASDAQ:GOOG). RAYS needs to offer more clarity on this issue.

Too Good to be True?

As the pumpsanddumps.com states:

Beware if the company claims to be an industry leader (do you really think a penny stock can be a leader in anything except possibly scams?) or has made a breakthrough discovery. A company with legitimate breakthrough technology is unlikely to be promoting itself on the penny stock market and will most likely have funding available to it within a variety of partnerships with major companies. These same companies will not likely be interested in dealing with a penny stock company. Also, question the likelihood of a fairly new company being the leader in anything other than schemes.

Let’s see what RAYS declares to be…

From the company profile on Yahoo!Finance:

Raystream Inc. provides proprietary video compression technologyto businesses and consumers worldwide. Its technology reduces the file size of high definition (HD) videos with no loss in clarity or quality. The company enables HD video over Internet connections through its online video platform. Its automated content management system enables users to manage uploading, editing, conversion format, and queue management, as well as storage, analytics, and client side utilities. The company offers commercial conversion for large-scale content owners, content distribution networks, advertising groups, and telecommunications companies; personal conversion for smaller video content developers, individuals, and person users; and live-streaming for large and small businesses, news organizations, sporting clubs, and individuals.

From the “About Raystream” in a recent press release:

Raystream Inc. is bringing its proprietary video compression technology to businesses and consumers worldwide. This technology drastically decreases bandwidth costs by reducing the file size of HD videos up to 90 percent, with an average of approximately 70 percent, and with no loss in clarity or quality — so they can be streamed online without buffering or stopping. Raystream’s technology puts high definition video in the reach of nearly every Internet user on the globe.

In their October 2011 10Q, RAYS makes what we thought looked like an absurd statement coming from a company with no financial backing from industry giants or venture capital firms

Raystream is the first company to offer HD compression technology…No other company today specializes in HD compression technology.

Wow. It seems they have discovered one of the most disruptive video technologies of the century, with the potential to revolutionize the entire web.

To verify RAYS’s claims, we decided to perform our own simple web search. As expected, just by conducting simple web searches, we found several companies that specialize in HD video compression technology. You can do the same.

Interestingly enough, in a recent development on Reel SEO’s website, freelance writer Christopher Rock published a glowing follow-up to his originally skeptical column about Raystream’s technology. Well, we have only to read the second sentence of his first paragraph to maintain a skeptical eye on the results that Mr. Rock publishes further down in his column:

I sent them a 271MB video file and asked them to do that voodoo that they do to it and send it back.

This is where we again say that Raystream’s secret sauce is no secret. Of course they can show that an existing technology works, but what they fail to do is show, by technical example, how they have added any value to x264. Anyone familiar with x264 can pretty much see this, as described in Lucian Gregory’s blog post, Raystream (RAYS): Trying to Market Essentially Free Techology?, that came out after Reel Seo’s column. An excerpt that we whole-heartedly agree with follows:

In any case, the measurements here appear to show that Raystream’s technology does not offer a compelling solution for video compression over the freely-available x264 encoder. The test of this was easy to put together and shows that Raystream’s claim that “before Raystream,” compressions such as the ones Raystream achieves were not possible, is patently false. Virtually the same compression ratios are achievable using a free product.

So why hasn’t Raystream protected its only asset with patents? On the company’s website, the answers to this frequently asked question sheds light on this issue:

Q: Does Raystream have a patent or patent pending on its technology?

A: Raystream did not apply for a patent for its HD video compression technology due to a number of factors, most specifically as a measure to protect its proprietary nature and maintain it as a trade secret claim. Other factors include:

-

- Applying for patent protection of our various technologies requires disclosure and full description of how the technology works. If accepted, the patent details would be published, opening our technology to possible replication by competitors without patent infringement even if minor modifications were made.

- Securing a patent for software takes a long time, is expensive, requires government action and approval, and involves a significant amount of uncertainty.

- Trade secret protection is quicker and less expensive, aligns with our strategy, and is more certain.

- Patent protection offers only civil (monetary) remedies. Trade secret protection offers federal criminal remedies.

- For these reasons, we have made the strategic decision to use trade secret protection instead of patent protection.

You can judge yourself, but in our opinion these considerations are simply unconvincing. How do you explain the fact that practically all the other major proprietary codecs are patented (Exhibit 8)?

Another important reason to patent video codec is that their underlying algorithms are easy victims of “reverse engineering”. The hackers Jerome Rota and Max Morice (Link 1, Link 2) needed only a week to reverse engineer Microsoft’s MPEG-4 Version 3 video codec!

On November 8, more evidence was provided supporting the argument that RAYS technology may not be what they claim it to be. A simple test was published here, reproducible by anyone with a minimal Linux OS expertise. The author was able to reach the same rate of compression claimed by Raystream – even 3 MB less — with the freely available tool mencoder and the H.264/AVC codec. By the way, one only needs to download the RAYS showcase video to see that it was also compressed with this codec. Opening the file “ray_480p.mp4” with a video player and looking for its properties will show you that the RAYS proprietary codec is in reality a common H264 (Exhibit 2)

A few days after that test was published, RAYS modified the see-for-yourself-page, removing the section on the left (“Watch original version – 686 MB”) and on the right (“Watch standard compression 214 MB – 214 MB”). The only video that remained was that one with the text “Watch Raystream version – 28 MB”. One of our investigators tried to reconstruct the page’s previous appearance, shown in the Exhibit 3. At any rate, the old code was not removed (just commented) and it’s still visible in the page “source view” (Exhibit 4).

By now, it should be obvious that this story is too good to be true.Investors need to ask themselves a question that is often asked by ChinaHybrid skeptics such as Muddy Waters and Citron. Why would a company with such a game changing technology choose to go public via a transaction with a shell without assets? The answer – we believe it is unlikely that the company has some game changing technology and in the slim chance it does it will have to spend millions of dollars just cultivate it, diluting shareholder value along the way.

We find it impossible to believe that the firm that claims to possess unique technology could not raise substantial capital as a private firm, culminating in partnership arrangements with reputable industry giants or in an impressive IPO debut when it could maximize its return on its investment. They instead chose to come to the market with a public shell company (where their reputation would surely be tarnished) that has limited funds to enhance or market the alleged Raystream “product.” This is a very important point to understand. That would have been like YouTube choosing to go public via an RTO transaction as opposed to combining forces with Google. If you have revolutionary technology the giants will find you, and you will want to partner with a firm that can back you. You will not want to go public and then embark on massive dilution activities to fund your business plan, nor will your shareholders prefer this scenario. RAYS already has 50 million outstanding shares and to date has barely raised any capital.

| SIDEBAR — All too Familiar Story How the big boys with game changing technology do things |

To this point, we suggest investors read the story of DiVx Inc., a company in the same business RAYS claims to be that after several initial rounds of investment and funding by some venture capitalists went public with an IPO price of $16.

The company started with an initial investment as they began their journey to NASDAQ, with an initial investment of $5 Million in 2000, growing to $35 million in invested capital by 2005.

They solidified their position in the market place in 2006 by having their software downloaded with over 180 million downloads and over 50 million DivX Certified devices shipped. Their partners included Samsung, Sony, Toshiba and Philips, working in multiple devices such as DVD Players, Blu-ray Players, Televisions, Game Consoles, Mobile Phones, Media, Streamers, Multimedia Storage Devices, Portable Media Players and In-car Players.

They went public in September 2006 with annual revenues tracking at about $60 million. The registration statement covered 9,100,000 shares of common stock at $16.00 per share, raising proceeds for the Company, before expenses, of approximately $111 million. They closed at $18.70 per share, giving the San Diego-based company a market value of $625 million.

According to an excerpt from the DIVX 8-K filed Oct 30, 2006, third quarterconsolidated revenues were $15.4 million, an increase of 83 percent from the third quarter of 2005. Non-GAAP Net income in the third quarter of 2006 was $3.6 million, or $0.12 per diluted share, compared to net income of $821,000, or $0.02 per diluted share, in the third quarter of 2005. Revenue for the nine-month period ended September 30, 2006 was $42.7 million or 90 percent more than the comparable 2005 period. Non-GAAP net income for the nine months ended September 30, 2006 was $9.15 million, or $0.33 per diluted share, as compared tonet income of $373,000, or $0.01 per diluted share, for the nine months ended September 30, 2005.

They were acquired four years after the IPO in September of 2010 for $323 million by Sonic (SNIC), developer of digital media software (its flagship brand is Roxio). The price amounted to $9.25 a share. At the time DivX employed 371 workers worldwide.

Sonic in-turn was then purchased three months later in January 2011 by Rovi Corp.for $725 million.

So what did Raystream GmbH sell its ground breaking technology for? Well they certainly did not require any cash or follow the route that a respected firm like Divx took.

From the SEC Filing dated 09/23/2011:

On September 19, 2011, Raystream Inc. (the “Company”) entered into an agreement whereby it acquired 100% of the issued and outstanding shares of Raystream GmbH in exchange for the issuance of 20,000,000 shares of common stock of the Company. The acquisition of Raystream GmbH makes it a wholly-owned subsidiary of the Company.

They paid Raystream GmbH with 20,000,000 common shares. How much was it in U.S. Dollars? The answer to this question isn’t so easy because at that time the stock was not actively traded in the market. Anyways, considering that about a month before (August 22, 2011) Interdom Corp (ITRD) affected a 37:1 forward split and that all the shares issued in the past had a value of $0.03/share, it’s reasonable to estimate a value of $0.0008. That means, that Roman Rumpf, the 29 year old founder of Raystream GmbH and inventor of this breakthrough technology gave it away for $16,000 in stock, and no cash!

Where/Who are RAYS Customers?

If you had a revolutionary product wouldn’t major companies like Netflix, Youtube, Hulu and the like be chomping at the bits to access your products? The RAYS promotional campaign wastes no time tossing these names around as potential RAYS customers. So who are RAYS customers? Well surprise,these big boys are not customers of RAYS. What is interesting is that if you visit the site that hosts the free and open-source software that RAYS applies to its product you will notice that all the big names have registered to this site and are keenly aware of AVC/H.264. These include Google (who owns YouTube), Netflix and YouTube. Apparently, this technology is not a secret.

So far, Raystream has only named three customers, one of which is here in America called EdgeFactory OmniMedia. We called and spoke with a representative and discovered they had already severed ties with Raystream and will no longer do business with them.

The second is Laterna Magica located in Germany. We called and left several messages, stating that we wanted to find out more about RAYS video compression technology and how effectively it was working for them. We were clear in conveying that we were considering RAYS as a potential investment and thought that speaking with a client like Laterna, named by RAYS on their website, was a good start. We did not receive a call back. Our last attempt was successful in getting in touch with the CEO, who would not comment regarding their relationship with Raystream.

Finally, RAYS just recently announced the Christian Broadcasting Network as a “customer” who will be using the technology on a trial basis for 60 days. We take this to mean free of charge. Are all of their “customers” on a trial basis?Is this why there is no revenue stream?

Massive Pump Campaign: So Where is the Money Being Spent?

So far we have confirmed that RAYS largest shareholder, Ultimate Trade, has spent at least a grand total of $3.25 million on a promotional campaign to disseminate the RAYS story. RAYS management should be advised to put that money to better use by spending capital to develop its market and customer relationships. We find this unbelievable. RAYS is not even hiding the fact that it is essentially as we see it, pumping its own stock. Per its 2011 second quarter 10Q the company has spent no capital on R&D and only$6,774 to market its revolutionary product. We plan to send information on this and more to the SEC Special Task Force.

This is not the first time Ultimate Trade has been involved in a stock promotional campaign.

The RAYS-LEXG Connection

The original change of control filing mentioned earlier in our report says nothing else about Unlimited Trade Inc, but we will learn though some subsequent filings (on September 23, 2011) that it is an offshore entity.

Before the September 23 filing, an iHub user posted the addresses associated with the domain unlimited-trade.com:

Unlimited Trade Inc.

Frankfurt Office

Bockenheimer Landstraße 17/19, 60325 Frankfurt/Main, Deutschland/Germany

P: 0049 69 710 455Panamá Office

Edificio Century Tower, Piso 4, Oficina 401-2141, Panamá, República de Panamá.info@unlimited-trade.com

We also learned that Unlimited Trade Inc. is a sort of German-Panamanian entity. To be more precise, there is no entry about Unlimited Trade in the German Company Register, and the address above is a virtual office — not the first one that we will reference in this story.

Looking at the Panamanian Company Register, we have more luck in finding some interesting information.

The company was created on October 5, 2010 and the following persons are its officers (or more likely straw persons):

- Marcos Antonio Gomez Sanchez (President)

- Francela Ivonne Findlay Silva (Treasurer)

- Orlando Zamet Reyes Saldaña (Secretary)

Thanks to a very useful site (http://ohuiginn.net/panama) we can do a search with these names and quickly discover that there is another Panamanian company with two of the same officers:

Gekko Industries Inc.

- Manuel Mauricio Monge Acuña (President)

- Orlando Zamet Reyes Saldaña (Treasurer)

- Francela Ivonne Findlay Silva (Secretary)

The name of Gekko Industries came into the public eye in relation with one of the most successful pump-and-dump promotions of the year: Lithium Exploration Group Inc. (OTCPK:LEXG) (A story discovered by The Street Sweeper when LEXG traded at $4.02, and now trades for less than $0.70).

But this is not the only link between RAYS and LEXG. In looking at the Html code of any Raystream web page, there was a small piece of commented code that referred to LEXG.

<!–

<div class=”fright stockquote”>OTCBB: LEXG <span class=”greenText”>1.00 + 0.00</span><a href=”#None” class=”header_butt”>STOCK QUOTE</a></div>

–>

This appears to be clear the evidence that RAYS webmaster used the same Html Template that was used for the LEXG site. It was removed on November 28, 2011 after the connection became public on a forum but it’s still visible in this video.

Strange coincidence, isn’t it? But this isn’t the last one. RAYS and LEXG are heavily pumped by many paid stock promoting newsletters and on many message boards like those one of Yahoo! Inc.(NASDAQ:YHOO) and iHub. Starting on October 12, 2011, RAYS was promoted by more than 19 paid newsletters and in the first week of November was among “The Most Promoted Penny Stocks This Week” according to stockpromoters.com.

By far, the most well paid RAYS campaign was one orchestrated by The Stock Market Authority (smauthority.com, now a dead link). In their Disclaimer they say that they have indirectly “received and managed a total production budget of $3,250,000” to provide public awareness for RAYS. According to the disclaimer, the campaign was financed by Unlimited Trade. Recall that Ultimate trade is the controlling shareholder of RAYS. During its short life, Smauthority promoted only one other stock, LEXG. The LEXG campaign was also expensive, with a total production budget of $3,296,800 and was financed by Gekko Industries. We believe that it’s not beyond the realm of reason that whoever controls Gekko Industries, Unlimited Trade, RAYS and LEXG are also tied to Smauthority.com.

On November 22, 2011, Go Daddy suspended the domain Smauthority.com for SPAM-AND-ABUSE.

As if the newsletter promotion hasn’t been massive enough (More info on this – Link 1, Link 2, Link 3), the company has just embarked on a prolific IR campaign. On October 6, 2011 they “announced it has retained Halliburton Investor Relations (“HIR”), a Dallas-based, full-service investor relations firm”. Since that alert until the end of November 2011, they released 8 announcements on Business Wire with a lot of not-so-detailed claims or announcements.

For example, in a recent release (“Compression of Full High Definition 3D Videos”) they use the “sexy” term “cloud-based architecture”. This is exactly the same term used by a substantial fraud we busted earlier this year, the Chinese RTO Subaye (OTCPK:SBAY).

In another recent press release, they were pleased “to announce our office in Paris, France, opened on November 10, 2011” but as of now no Paris address is available on the contact page of the RAYS website.

In further dissecting the contact page, we noticed that the office in Germany is the medieval Cast of Lichtenfels (as we’ll see later, this cast dishes out a lot of surprises!) while the address in Orlando is a Da Vinci Virtual Office. Another Da Vinci Virtual Office is the address reported on every SEC filing but omitted on the web site: 219 Redfield Parkway #204, Reno, Nevada(Address of principal executive offices). Regarding the office in Texas, it is only 1.8 miles from another company that we will encounter later (it belongs to Raystream’s CEO Brian Petersen): Petersen – Hines, LLC, located in 15305 Dallas Parkway, Suite 300, Addison, Texas… another Virtual Office. But this time from Regus.

| SIDEBAR – The Classic “Pump and Dump” SchemeIt’s common to see messages posted on the Internet or sent by e-mail that urge readers to buy a stock quickly or to sell before the price goes down. Often promoters of the stock will claim to have “inside” information about an impending development or to use an “infallible” combination of economic and stock market data to pick stocks. In reality, they may be company insiders or paid promoters who stand to gain by selling their shares after the stock price is pumped up by the buying frenzy they create. Once they sell their shares and stop hyping the stock, the price typically falls, and investors lose their money.

On the following pages below are a few companies with the most recent pump and dump scheme. Lithium Exploration Group went from 12 cents to almost $4 a share in just under a month and at one point had a market cap of almost $200 million. LEXG 1 Year Chart

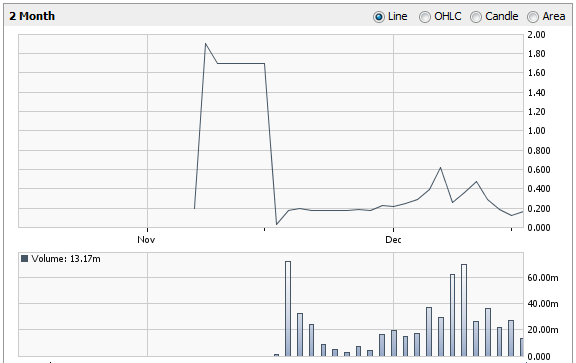

Amwest Imaging (AMWI.OB) is a cloud computing company. It has around 500 million shares outstanding, giving it a market cap of around $100 million. AMWI 2 Month Chart

Looking at both of these most recent examples will give you a feel to how pump and dumps work. The SEC is investigating these type of companies but it’s usually too little too late for the investor. Here are some recent actions by the SEC. SEC Charges N.Y.-Based Penny Stock Promoter with Fraud Washington, D.C., Jan. 14, 2011 – The Securities and Exchange Commission today charged an upstate New York-based penny stock promoter and his affiliated website with fraud for failing to disclose that he was paid by certain issuers to promote their stock while simultaneously liquidating millions of his own shares for profits of at least $2.95 million. The SEC alleges that Christopher Wheeler of Victor, N.Y., received compensation at various times in 2007 and 2008 to promote several thinly-traded penny stocks on his website, OTCStockExchange.com. Wheeler’s website claimed to “have compiled a long list of successful stock picks” and to afford investors the opportunity to “make a fortune.” SEC Freezes Funds in Trans-Atlantic “Pump and Dump” Scheme, August 15, 2008 –The Securities and Exchange Commission announced today that it obtained an emergency court order freezing the profits from an alleged $13 million international fraud involving a Seattle-area microcap company and a Barcelona stock promoter. The Commission charged Bremerton, Wash.-based GHL Technologies, Inc., and its CEO Gene Hew-Len with issuing a series of false press releases touting the company’s business dealings. The Commission also charged Francisco Abellan (also known as “Frank Abel”) of Barcelona, Spain with coordinating the scheme, sending glossy promotional mailers to over 2 million U.S. recipients and unloading over $13 million in GHL stock on unsuspecting investors. “The Street Stock Report,” a full-color glossy mailer sent to millions of U.S. addresses urging investors to purchase GHL stock quickly to see huge trading profits. Around the same time, Hew-Len issued nine press releases over a nine-week period hyping the company. Among other things, according to the SEC, the press releases made false claims about contracts with large customers, fraudulently touting millions of dollars in potential revenues. Following this concerted promotion campaign, GHL’s stock price doubled and trading volume spiked nearly 1500%. Abellan and his entities sold their GHL stock holdings for profits in excess of $13 million. The stock, which reached a high of nearly $9 per share at the height of the scheme, now trades at under a penny. SEC Charges Seven in Global Warming Pump-and-Dump Scheme Washington, D.C., Feb. 18, 2011 – The Securities and Exchange Commission today charged a group of seven individuals who perpetrated a fraudulent pump-and-dump scheme in the stock of a sham company that purported to provide products and services to fight global warming. (OTC:CTTD) SEC Charges Company CEOs and Penny Stock Promoters in Kickback Schemes Washington, D.C., June 30, 2011 – The Securities and Exchange Commission today filed securities fraud charges against several CEOs, their companies, and two penny stock promoters alleging they used kickbacks, a bribe and blast e-mails to manipulate trading in microcap stocks. |

Persons and Places involved in RAYS- No Strangers to Pump and Dump Stories

German Leg

The Raystream’s site is hosted in Germany, it was registered by Roman Rumpf, that provided the Texas office address as its Registrant Address. TheAdmin and Tech Addresses are the same: Ringstrasse 13, Berndorf, Hessen. This address doesn’t not jive with any address in SEC filings, but as we will learn later, it’s the private address of Roman Rumpf.

The address for the Raystream’s German Branch is Burg Lichtenfels, 35104 Lichtenfels. “Burg” is the German word for “Castle” and in fact the Caste ofLichtenfels is a real medieval castle.

Castle of Lichtenfels and Tan Siekmann

The Castle of Lichtenfels was built in 1189 and is located in the German State of Hesse, whose largest city is Frankfurt am Main (remember that Unlimited Trade has/had a Virtual Office in Frankfurt).

Since the late 1980s this Castle has belonged to the German entrepreneur Tan Siekmann and his parents.

Tan Siekmann is well-known in Germany because his company, Biodata AG,also based in the castle, was one the most famous bankrupt companieswhen Germany’s Dot-Com bubble exploded. After Biodata AG’s first insolvency in 2001(There is even a movie about it), the CEO and major holder Tan Siekmann founded “Biodata Systems GmbH“. Three years later (2004) “Biodata Systems GmbH” was also declared insolvent. Tan Siekmann, in this case, bought some of the insolvent assets and founded “Safe-Com GmbH & Co. KG“, and like the others was domiciled in the castle. Information on Safe-Com is scarce, but its website, Safe-Com.com, is no longer active, although some archived/crawled parts of the site are still available to view. It is also known that Roman Rumpf had a key technical role in Safe-Com.

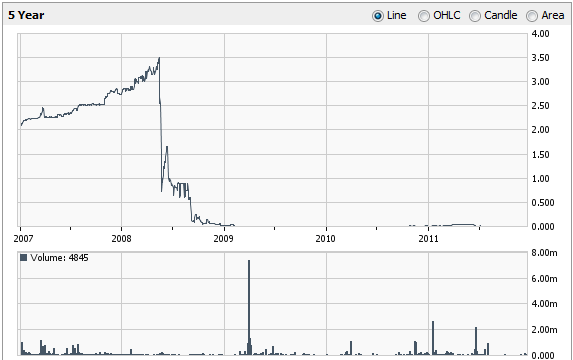

In another instance, as reported in a four year old article published by the German business magazine “brandeins“, the company Demuth & Dietl (a mobile telephony service provider) accused Tan Siekmann of being responsible for its own bankruptcy. Even more interesting, the same article states that in 2007 Safe-Com bought 65% of BodyTel Scientific Inc. (OTC:BDYT). BodyTel was a development stage company in a “sexy” sector (telemedical monitoring). After having touched $3 in 2008 it declined to 2 cents only a few months later!

BDYT 5 Year Chart

There is still more…

When Tan Siekmann was one the Major Holder at BodyTel, the company signed an investment agreement with Michael Kang and Francis Villena , who acted as agents for Bridge Capital LLC (June 11 , 2008)

In the Panama Companies Register there is a firm registered on June 6, 2008 called Bridge Capital Inc. (yes, we know the first was a LLC and this one is an INC.). Who were two of the three Bridge Capital Inc.’s managing directors? (Note that they all resigned):

- Maria Lucrecia Martinez (President)

- Marco Antonio Gomez (Treasurer)

These names are now quite familiar to us:

- Maria Lucrecia Martinez is President at Foresight Media Inc.

- Marco Antonio Gomez is President at Unlimited Trade Inc. , and RAYS’ largest shareholder (the name there is longer: Marcos Antonio Gomez Sanchez)

To supplement the information we already have on Unlimited Trade Inc, Foresight Media Inc. (FM) enters the mix within the P&D campaign…

The Stock Market Autority (SMA) disclaimer for RAYS states:

[…]Raystream, (OTC:RAYS), the company featured in this issue, appears as paid advertising, paid by Unlimited Trade to provide public awareness for RAYS.[…]

[…]SMA and Foresight Media (FM) have used outside research and writers using public information to create the advertisement coming from SMA about RAYS.[…]

[…]FM has received and managed a total production budget of $3,250,000[…]

…confirming that Unlimited Trade paid itself in a certain manner to promote RAYS.

A medieval Castle, the same young entrepreneur, four collapsed businesses(one of which looks to be a U.S. pump and dump story), and conflicts of interest…an impressive record, making RAYS quite a good candidate for an SEC investigation.

Michael Kang and Francis Villena

Together, these individuals were behind BRIDGE CAPITAL.

But who is Francis Villena, aka Francisco Abellan Villena, aka Francisco Abellan, aka Frank Abel?

He lives in Barcellona, inherited an important printing company from his father, but above all it’s an “old friend of the SEC’s”, which on August 15, 2008 froze his assets, accusing him having earned over $13 million in a Trans-Atlantic “Pump and Dump” Scheme related to shares of GHL Technologies, Inc (Link 1 and Link 2)

Regarding Michael Kang, there was a Nevada corporation founded early this year called eLogic North America FX. On its contact-page, eLogic GmbH makes reference to “eLogic North America”, which suggests that they’re the same company. The Nevada Corporation’s president is Michael Kang, making him the fourth person in our crew of usual suspects to be tied to this company.

Roman Rumpf

Roman Rumpf was born on July 29, 1983 in Twistetal-Berndorf, a very small town in the German State of Hesse and he is currently domiciled in Ringstrasse 13, Berndorf, Hessen, one of the addresses registered for the raystream.com domain.

He is Co-founder and CTO of Raystream Inc and he also had a key technical role in Safe-Com as stated in his bio on Raystream’s site.

The June 24, 2011 8K states:

From June 2006 to February 2008 Mr. Rumpf was Project and Product Manager at Qnective Inc. a private Social Networking company.

There are some discrepancies between this statement and other information available on the Qnective web site and in the SEC filings.

As the company itself declares in its home page, Qnective was founded in 2007 (April 2, 2007 is the first date where the company name appears — its former name was Sotech Inc.). It is quite odd that it appears that Mr. Rumpf was Project and Product Manager at Qnective 10 months before the company was even founded.

The second and most important discrepancy is that this time (“From June 2006 to February 2008”), Qnective WASN’T private. Before going private in 2011, the company was listed on the OTC BB under the symbol QNTV. On May 5, 2011 the price of the stock was $1.00. The last price before going private on January 28, 2011 was $0.20. Tan Siekmann was a Beneficial Owner (10% or more) and the CTO of Qnective Inc.

Let’s take a closer look at Raystrem GmbH, the German firm created onMarch 21, 2011, its first CEO being Roman Rumpf (See Registrar for German Companies). Although the company was formed on that day, it was only communicated to the German Company Register on May 2, 2011. The sole owner of Raystream GmbH was the Panamanian Unlimited Trade Inc (Exhibit 5). Here is the timeline of events leading up to the acquisition of Raystream GmbH by Raystream Inc.

August 16, 2011

Roman Rumpf resigned as CEO and Thomas Friedli (Frankenberg, 1977-05-12) came on board to substitute him.

June 14, 2011

The same Roman Rumpf became the new CEO and only officer of Interdom Corp when Unlimited Trade Inc bought it.

June 16, 2011

Unlimited Trade Inc (Exhibit 6) sold its shares in Raystrem GmbH to the German holding “TOM Beteiligungsgesellschaft GmbH” (“TOM”). On June 24, 2011, Thomas Friedli took the place of Tan Siekmann as the CEO of this holding is (Lichtenfels, 1966-10-29).

Until June 7, 2001 Tan Siekmann was the only owner of TOM before selling a part of his shares to Thomas Friedli and Roman Rumpf (note that TOM had also a role in the Biodata saga).

July 12, 2011

Roman Rumpf resigned as CEO and become CTO. Brian Petersen was appointed as the new CEO.

August 22, 2011

Interdom changed its name to Raystream Inc and did a 37:1 forward-split.

September 19, 2011

Raystream Inc. acquired 100% of Raystream GmbH.

The Panamanian Unlimited Trade Inc purchased the German Raystrem GmbH through the American Raystream Inc. on September after having sold it in June of the same year. Unlimited Trade was presented in front of the German Notary by Tan Siekmann (Exhibit 7). Here you will find more than one clue of non-disclosed related party transactions.

The list of the company owners for Raystream GmbH and TOM Beteiligungsgesellschaft mbH is presented in the Exhibit 5 and 6.

Thomas Friedli

Referenced above for having been part of certain share transaction, Thomas Friedli is known as the manager of the German branch of RAYS.

He is also Founding Partner and Chief Operations Officer of eLogic GmbH. The CEO of eLogic (also located in the Castle of Lichtenfels) is Tan Siekmann.

U.S.A. Leg

The American staff of RAYS is practically the same as those who work forPetersen-Hines LLC. When Brian Petersen was appointed as CEO at RAYS, the same SEC filing covering this appointment stated that he “has grown Petersen – Hines, LLC to a $35 million dollar company within six years”, even making it debt free. Is it feasible that they can devote enough time and resources to this development-stage RAYS venture? We are in the process of trying to determine if Petersen-Hines is aware of the past dealings of those associated with RAYS.

Nadia Christian, Vice President of Marketing at RAYS

Ms. Christian should be the busiest person in the staff. Not only is she presumably working simultaneously at Raystream Inc and Petersen-Hines LLC, but she runs also businesses of her own as a Cognitive Fitness Therapist. See also, this link.

Dane Butzer, Business Development Manager

We only had to view the html code of Raystream’s site to find a special surprise, another key staff member that was seemingly hidden from view:

Mr. Butzer has worked in intellectual property law with such renowned firms as Fitzpatrick, Cella, Harper & Scinto, and The Swernofsky Law Group. He also maintained a highly successful solo practice. Mr. Butzer has witnessed many start-up ventures and ongoing businesses both fail and succeed over the course of his career, resulting in a deep understanding of the fundamentals of applying technology and business processes in the real world.

In performing a web search on his name, he seems to be a reputable U.S. patent application attorney.

It’s our opinion that the heads of the RAYS operation are based in Germany, but they made sure to appoint a recognizable U.S. management team to possibly give a façade of legitimacy to the company.

Clues of an Off-Shore Scam (“Regulation S”)

On April 30, 2011Interdom had 4,175,000 outstanding shares:

- 3,500,000 owned by Igor Rumiantsev and purchased for $.0010/share on April 14, 2010.

- 675,000 issued at $.03/share

On June 14, 2011, Igor Rumiantsev privately sold all his 3,500,000 shares to Panamanian Unlimited Trade Inc for $200,000 ($.0571/share) making it the new major holder:

- 3,500,000 owned by Unlimited Trade and purchased for $.0571/share

On August 22, 2011 Interdom changed its name to Raystream and did a 37:1 forward split. After the split Raystream now had 154,475,000 outstanding shares:

- 129,500,000 owned by Unlimited Trade and purchased for $.0015/share

- 24,975,000 purchased by someone for $.0008/share

On September 19, 2011 three important events happened:

- Raystream Inc bought 100% of the German Firm Raystream GmbH for 20,000,000 shares

- Unlimited Trade converted its $2,000,000 financing into 5,000,000 common shares at $.40/share).

- Unlimited Trade cancelled 129,500,000 shares and now owns 5,000,000 shares

All the transactions occurred on September 19 pertain to off-shore entities (based in Germany and Panama) therefore these shares were exempt from registration (Regulation S). That led to the following situation:

- 20,000,000 owned by Raystream GmbH (paid price unknown).

- 5,000,000 owned by Unlimited Trade and paid $0.40/share

- 24,975,000 owned by others and having an initial price of $0.0008/share

- for a total of 49,975,000 outstanding shares.

Considered that to qualify for a Regulation S exemption, the shares may not be sold back into the United States for one year the effective count of shares available for free trading is currently only a little less than one half (of course they do not risk to loss the control of the company).

But… did Unlimited Trade really cancel those 129,500,000 shares? Nobody knows since they were not registered with the SEC.

Now the risk is that they will resell “Reg. S” or claimed-to-be-canceled stock to U.S. investors, diluting the float, pocketing high profits for themselves and causing the price to collapse.

Unlimited Trade already owned both Raystream Inc (NYSE:USA) and Raystream GmbH (Germany), but all of those transactions occurred between the same these related party entities. What exactly could be the rationalebehind these moves?

Dilution is a Certainty

Let’s assume for one moment RAYS has a piece of legitimacy. Since Raystream is a development stage company generating no revenues we need to assume that it will have to raise substantial capital to implement its goals.RAYS agrees (from various filings):

- “The Company has incurred losses since inception resulting in an accumulated deficit of $189,286 as of July 31, 2011 and further losses are anticipated in the development of its business raising substantial doubt about the Company’s ability to continue as a going concern. Although the Company obtained debt financing in July (See Note 4), the ability to continue as a going concern is dependent upon the Company generating profitable operations in the future and/or to obtain the necessary additional financing to meet its obligations and repay its liabilities arising from normal business operations when they come due.”

- “We expect we will require additional capital to meet our long term operating requirements. We expect to raise additional capital through, among other things, the sale of equity or debt securities.”

- “We expect that working capital requirements will continue to be funded through a combination of our existing funds and further issuances of securities.”

- “Existing working capital, further advances and debt instruments, and anticipated cash flow are expected to be adequate to fund our operations over the next six months. We have no lines of credit or other bank financing arrangements. Generally, we have financed operations to date through the proceeds of the private placement of equity and debt instruments. In connection with our business plan, management anticipates additional increases in operating expenses and capital expenditures relating to: (i) acquisition of inventory; (ii) developmental expenses associated with a start-up business; and (iii) marketing expenses. We intend to finance these expenses with further issuances of securities, and debt issuances. Thereafter, we expect we will need to raise additional capital and generate revenues to meet long-term operating requirements.”

- “We will have to raise additional funds in the next twelve months in order to sustain and expand our operations. We currently do not have a specific plan of how we will obtain such funding; however, we anticipate that additional funding will be in the form of equity financing from the sale of our common stock.”

What does all this mean? These comments imply that RAYS only has enough cash to sustain it operations for the next 3 to 12 months, depending on which SEC filings are referenced, just to sustain operations.

TICK TOCK

Well, this deadline is approaching fast and has likely accelerated now that it has a revolutionary, unpatented product to market. This means that substantial dilution, an investor’s worst enemy, is around corner and should continue well into the future. Investors who purchase RAYS shares now could be blindsided with equity offerings and a sharp hit to the share price. Worst yet, if the company is unable to raise capital the story could end badly in 3 months.

Valuation & Conclusion

Until RAYS clearly demonstrates that it can secure industry giants as customers or book meaningful revenues we believe that RAYS is worth no more than what it would claim as a shell company or at most about $0.004 to $0.01. ($200k to $500k divided by 50M outstanding shares). Even when applying RAYS claimed shareholder equity (which virtually consists solely of goodwill) as shown its October 2011 10Q, a price target of just $0.19 can be derived.

Furthermore, even if RAYS has a semblance of legitimacy, dilution is a major risk further limiting EPS performance. To put this into perspective, Divx raised a total of $146 million (pre IPO and IPO) to develop their business. If RAYS needs to raise a similar amount of capital, shareholders will be slammed with massive dilution. For a company with limited revenues, equity offerings will likely have to be accomplished at a major discount to its current market price.Even in the unlikely case that RAYS had a product that people could sink their teeth into (in other words an honest company with a promising product), you would still only end up with a company with a horrible equity market presence, not only due to the manner in which it went public, but also by having gone public prematurely.

Although the company talks a big talk, Raystream cannot boast solid customers to initiate to a meaningful revenue stream. In fact, we were unable to get much out a former customer of Raystream, who consequently terminated its need for whatever technology the company offered, effectively reducing the number of paying customers RAYS has to just one, to the best of our knowledge and until proven otherwise. The mention of large industry players such as YouTube and Google is a tactic promoters are using to draw investors into a web of deception. Would respected companies like these seriously want to deal with executives whose pasts are as shady as Raystream’s story?

Raystream is hardly letting the product speak for itself. The company instead chooses to promote the stock through hype and related party funds and what amounts to a weak attempt to demonstrate how much more superior their so called “proprietary” product is when compared to others. If Raystream was a respectable company, it wouldn’t use pump outfits and stock promoters to throw industry buzz words around and spread innuendo of an eventual acquisition by an industry giant. The company would instead go much further into actually proving the product.

One of the most compelling facets of the RAYS story that has convinced us that there is no way to trust anything that comes out of the company’s camp is the cast of characters involved, a crew that can be referred to as the Usual Suspects due to their involvement with other failed ventures/promotions. If your head was not spinning by the time you finished reading about the business relationships of RAYS personnel, then you need to read it again. Let it sink in, and then decide if this is a genuinely honest business venture hell bent on over-achieving in a market that already appears saturated with the same technology RAYS claims to have developed.

Exhibit 1

Exhibit 2

Exhibit 3

Exhibit 4

Exhibit 5

Exhibit 6

Exhibit 7

Exhibit 8