Keeping GeoInvesting Premium Members constantly informed on a stock or stocks we are tracking, buying and selling is a top priority that we don’t think enough investment research sites strive for. We do our best to bring you into our stock research pit, real-time. Here is an example of a stock, Orbotech (ORBK:NASDAQ), we have been covering since 2015 and how we delivered our thoughts AND successful CALLS TO ACTION to our members.

Tuesday, June 28, 2016

Further Due Diligence On ORBK; Initiated Long Position

ORBK ($25.50) As disclosed to you on March 14, 2016 we recently added ORBK to our big cap buy on pullback . Yesterday, via premium tweet we stated:

We were able to have a quick call with the Company’s IR. After our preliminary due diligence we decided to add the stock to the “mock buy on pullback portfolio 2.0” that we created on May 31, 2016. Here is a look at our ORBK pullback note:

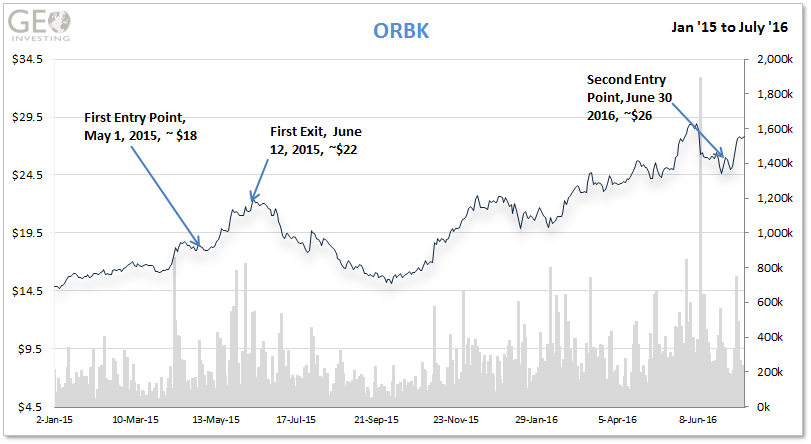

After a successful run with ORBK in May 2015, the stock crept its way back onto our radar. We bought ORBK in early May 2015 due to muted reaction to strong Q1 results. Shares quickly rose to $22 in mid June where we closed out our trade.

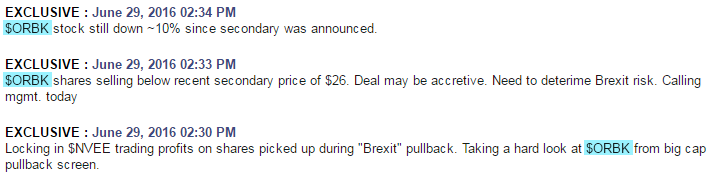

ORBK ended up seeing its 2015 EPS more than double to $2.09. Analysts expect EPS to grow $2.47 and $2.82 over the next two years. While not huge growth, shares are trading at a P/E of around 10 on 2016 EPS estimates (although ORBK’s industry does not generally carry a hi P/E (diversified electronics). However, shares recently plummeted 7 % on June 10th, 2016 on the heels of a secondary offering that de-risks the balance sheet and leads to EPS accretion. Trigger price $25.50.

“We are very pleased to have successfully executed this series of financing transactions which, we believe, will immediately increase shareholder value. The significant reduction in interest expense, net of the shares issued, is expected to be accretive to earnings per share on both pro forma and prospective bases,” stated Ran Bareket, the Company’s Chief Financial Officer. “The reduction in both interest expense and leverage on our balance sheet is considerable. In addition, the new debt agreement is secured only by the assets of the Company’s SPTS subsidiaries, whereas our previous Credit Agreement was secured by Company assets worldwide. As a result, we have substantially improved the strength of our balance sheet, seized upon current favorable conditions in the capital markets and enhanced operating flexibility for future growth opportunities.”

We believe that ORBK’s pullback from around $28 when it announced its secondary offering is unwarranted. While we calculate the transaction to issue shares and pay down debt to be only slightly accretive to EPS ($0.01 to $0.02 per share) on annual basis, we believe that after looking closely at the deal other bullish factors exist that could help lift shares back to their 52 week high of around $29.00 or a P/E 11.7 on analyst 2016 EPS estimates of $2.47.

These factors include:

- Significantly improves the risk profile of the Company which could eventually lead to expansion of its valuation multiples. Specifically, the new loans as part of the transaction are only secured by its U.K. subsidiary as opposed to the entire Company’s assets per the JP Morgan loan it paid off.

- We believe part of the reason management consummated these financial transactions is to put the Company in better position to use its balance sheet to explore new growth opportunities through potential acquisitions. One of the reasons we were a little hesitant about buying ORBK in the past was although growth had been respectable, we did not see much room for outsized growth from its current businesses.

We also explored the Company’s “exposure risk” to Brexit because it has a subsidiary in the U.K. and close to 14% of overall sales originate in Europe. Actually, it appears that expenses from its U.K. operations are recorded in British Pounds, while its revenues are in U.S. dollars. This means that a weakening of the U.K. currency could actually benefit ORBK’s bottom line or at least offset some of the negative currency impacts from potentially lower demand for its products from the U.K market.

Caveat:

- Investors need to keep in mind, even though we believe “Brexit” is a non-factor in the near term for ORBK; the fact that the Company does have exposure to Europe and the U.K. in general could make shares volatile due to headline risk.

Tuesday, June 28, 2016

ORBK Call to Action

ORBK ($23.99) — After a successful run with ORBK in May 2015, the stock crept its way back onto our radar. We bought ORBK in early May 2015 due to muted reaction to strong Q1 results. Shares quickly rose to $22 in mid June where we closed out our trade. ORBK ended up seeing its 2015 EPS more than double to $2.09. Analysts expect EPS to grow $2.47 and $2.82 over the next two years. While not huge growth, shares are trading at a P/E of around 10 on 2016 EPS estimates (although ORBK’s industry does not generally carry a hi P/E (diversified electronics). However, shares recently plummeted 7 % on June 10th, 2016 on the heels of a secondary offering that de-risks the balance sheet and leads to EPS accretion. Trigger price $25.50.

“We are very pleased to have successfully executed this series of financing transactions which, we believe, will immediately increase shareholder value. The significant reduction in interest expense, net of the shares issued, is expected to be accretive to earnings per share on both pro forma and prospective bases,” stated Ran Bareket, the Company’s Chief Financial Officer. “The reduction in both interest expense and leverage on our balance sheet is considerable. In addition, the new debt agreement is secured only by the assets of the Company’s SPTS subsidiaries, whereas our previous Credit Agreement was secured by Company assets worldwide. As a result, we have substantially improved the strength of our balance sheet, seized upon current favorable conditions in the capital markets and enhanced operating flexibility for future growth opportunities.”

Tuesday, May 19, 2015

Looking to sell 10% of our ORBK long position

On May 1, 2015 we listed our reasons for tracking ORBK and initiated a long position at ~$18. On May 5th 2015, we stated:

“after further due diligence, we have learned that there is an additional caveat to the story in that the company has limited visibility beyond one quarter out. We are still long this name, but we are keeping a cautious eye on the company.”

Shares are up over 9% since our May 1 call to action. We will look to sell roughly 10% of our long position.

Friday, May 1, 2015

Initiated Position in ORBK

Yesterday via premium tweet we stated:

“We see muted reaction to strong Q1 2015 earnings for ORBK as buying opportunity. Starting to build long position. #GeoCallToAction”

We have initiated a small position . We plan to interview managment next week and listen to the Q1 2015 conference call to determine if we will need to make any changes to our bullish assumptions. Here are our reasons for tracking:

ORBK ($17.79) – provides yield-enhancing and production solutions for printed circuit boards (PCBs), liquid crystal displays (LCDs), and semiconductor devices. Our reasons for tracking are:

- Just reported strong Q1 2015 results

- Q1 2015 revenues of $185 million vs $105 million in the prior year and ahead of analyst estimates of $181.2

- Q1 2015 non-GAAP EPS of $0.48 vs $0.19 in the prior year and ahead of analyst estimates of $0.43

- The company provided Q2 2015 revenue guidance of $185 to $193 million, ahead of analyst Q2 2015 revenue estimates of $184.8 million.

- We like companies that provide products/services to help their customers run a more efficient ship, especially in competitive environments. This often can lead itself to a highly recurring revenue business model.

Q1 press release quote:

“Our flat panel display business and semiconductor device division continued to perform strongly, reflecting healthy demand trends across product lines and customer segments. Consumer electronics is becoming an increasingly indispensable part of modern life, requiring ever smaller, thinner, faster, more flexible and even wearable devices. This inevitably gives rise to escalating manufacturing challenges, which Orbotech’s solutions are designed to solve, supporting both our customers and leading consumer electronics designers. The breadth and depth of our product offering, especially after the SPTS acquisition, enables us to benefit from the continually evolving and complex world of electronics.”

- The company has logged in 3 quarters of strong sales and non-GAAP EPS growth.

- Sales and EPS are expected to grow 26% and 131% respectably in 2015.

- Analyst just increased price target to $24.

Caveat

While strong top and bottom line growth are expected to continue for Q2 2105, growth is expected to slow in the second half of the year. Furthermore, growth is expected to moderate in 2016. However, the company’s recent performance of exceeding analyst estimates and its acquisition strategy may be enough to provide shares with support.