I hope you had a great start to your new year. In 2020, we are resolving to aggressively hunt, actively track and potentially buy superior medical device/testing companies with clear economic moats. Warren Buffett introduced the concept of “economic moats. An economic moat, per Investopedia, is defined as:

“…a company’s competitive advantage derived as a result of various business tactics that allow it to earn above-average profits for a sustainable period of time.”

So, why is that we feel compelled to go in this direction? Or just go to the end of this article to see what new medical device company we are so excited about.

Why We Like Medical Device Companies

Although the healthcare stock market universe is a field of dreams, where so many companies fail to grow revenue or turn a profit, there are plenty that are able to create sustainable moats by creating sticky customer and partner relationships.

Additionally, accessories that are used with medical devices or in conjunction with tests are often discarded after each use, also known as a Razor/Razorblade model. This creates predictable recurring revenue streams, which investors love. Once a level of revenue is reached, profitability can be established, leading to profits growing at a much faster rate than sales. These companies can also become ideal takeover candidates. We have identified several parameters to help us find medical device stocks that we think can multiply many times over. Some of the most important parameters, which many of the above examples demonstrate, include:

- First class management team with a history of operating medical device/test companies in the past.

- First class product that has little or no competition, where the effectiveness over the competition is clearly evident. (Moat)

- At an inflection point where revenues start to accelerate and where profitability has occurred or is close to occurring. Otherwise, there will be a high risk that the company will have to aggressively raise money by issuing stock. WE DESPISE DILUTION!

- Strong partnerships with pharmaceutical companies that may want to use the device/test during clinical trials. This could increase the chances that the partners will use the solution during commercialization of their drugs/therapies if they are approved by regulatory bodies like the FDA.

- Plenty of market share to capture.

- The solution actually expands the target market potential by opening up medical indications that the device/test can be used for.

- Saves the healthcare system money.

Now let’s take a look at our track record.

Comprehensive GeoInvesting Medical Device/Test Track Record

Since we launched GeoInvesting in 2007, our coverage on the medical device/test space has been encouraging.

The Bullish Side of Our Medical Device Company Coverage – Eight out of Nine excel; Five Multi-baggers

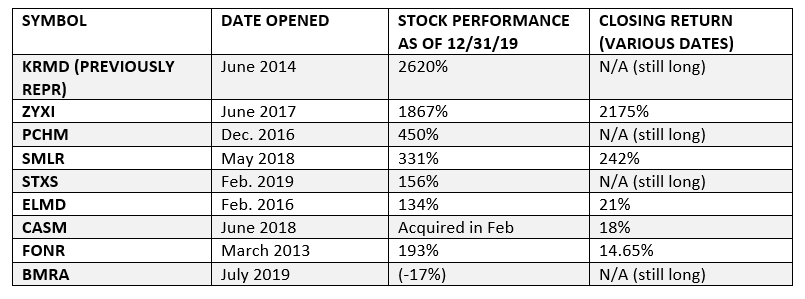

On the bullish research side, GEO has disclosed long positions on nine medical device/test stocks. I want to stress that we did not selectively choose to disclose just the stocks that went on to perform well – these stocks do, in fact, encompass our complete coverage of medical device stocks. In this article, I include a list of these companies, each accompanied by a few key bullet points that helped us develop our positive opinions. This is a routine we often follow as it helps us document our initial thoughts as a reference to see what we did right and where we may have gone wrong after our investments have played out. Hopefully, sharing these cliff notes with you can help you with your future research process.

Repro Med Systems, Inc. (NASDAQ:KRMD)

KRMD is up 2350% since our initiation of coverage in June of 2014 (old symbol was REPR). We later added KRMD to GeoInvesting’s Run to One Model Portfolio. The R21 portfolio aims to find higher quality penny stocks trading well under $1.00 that we believe have a chance of rising above $1.00 over time. These companies typically have clean capital structures. The company makes and sells a home infusion drug delivery system that does not require electric power to operate. The system uses subcutaneous needles to penetrate the skin, as opposed to typical systems that require power to deliver medication through intravenous needles by penetrating a vein.

- We believed that KRMD’s device was a perfect play on the growing trend to move patient care away from hospitals to the home or specialized clinics. The ease of use of the device allows patients to use it without the need of nursing care.

- Updates in Medicare reimbursement codes opened up the door for KRMD’s solution to gain traction.

- An amazing track record of growing revenue quarter over of quarter and year over year.

- Year over year growth in 34 of 39 quarters since the beginning of 2010.

- 24 out of 38 sequential improvements over same period.

- Huge and consistent stock purchases by an activist persisted, even as the stock moved higher. This investor later became a board member of the company.

- New experienced management team and Board of Directors accelerated growth with new business development initiatives. New board also removed some legacy management that had been wasting company funds on personal “toys,” like leasing a private jet from the CEO!

- Has mostly self-funded its growth.

- Successfully navigated issues outlined in an FDA warning letter

- We believe that KRMD will eventually be acquired by a pharma company or by a medical products distribution company.

Here’s our original KRMD article.

You can view a slide presentation (via my speaking engagement at the 2019 Planet Microcap Showcase conference in Vegas) we put together that highlights our coverage on KRMD (REPR) here.

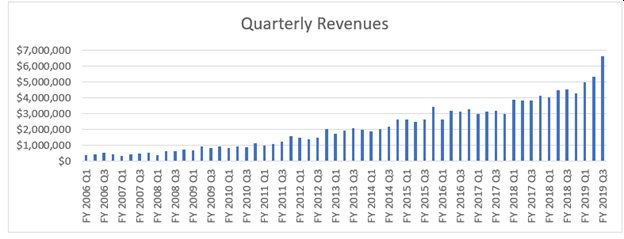

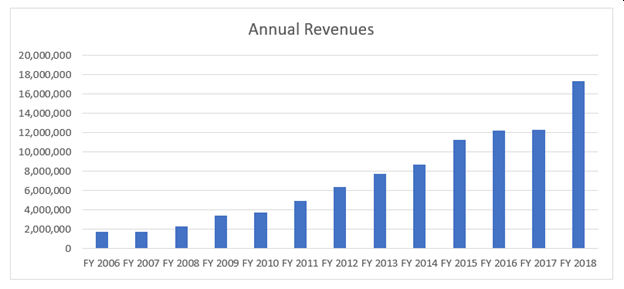

As an aside, we updated one of the KRMD/REPR revenue charts for this article since we feel it conveys a powerful message on the importance of consistent revenue growth.

Since 2006, of the 59 quarters leading up to and including the third quarter of 2019, there have been 50 quarters where the company had positive year-over year revenue growth and 39 quarters where the company had positive sequential revenue growth.

Since 2006, 12 out of 13 years until 2018, the company had posted positive year-over-year revenue growth.

Zynex, Inc. (OOTC:ZYXI)

ZYXI Rose 2175% at the time we closed our long position at $9.25 in June 2019. We disclosed a long position on the stock on June 6, 2017 at $0.40 and simultaneously added the stock to GeoInvesting’s Run to One model portfolio (R21). ZYXI markets pain management medical devices. We also added ZYXI to our Buy on Pull Back Model Portfolio, also successfully trading it around our core position after shares experienced an aggressive pullback during its run over $1.00. Our Buy on Pull Back Model Portfolios contain stocks that react negatively or have muted reactions to good news, or fall for no reason at all. We currently do not have any active Pullback portfolios, but you can see some of our prior ones here.

- Many R21 candidates we identify have multi-bagger potential due the existence of a possible de-risking catalyst event that the market has not found. These types of information arbitrage scenarios are common in the microcap space. With ZYXI, we stumbled upon a trifecta of positive catalysts. The company:

- Turned EPS positive

- Issued some really positive guidance in a conference call related to a quarterly report press release dated June 2 2017. This guidance was not mentioned in the press release, creating a classic InfoArb event.

- Began deleveraging its troubled balance sheet that had caused the company to enter into a forbearance agreement for two years. The company eventually paid off all its debt and improved its cash collections.

If there is one thing to learn from ZYXI, it’s that identifying companies with the potential for de-risking catalysts offers some of the best chances to experience quick multi-bagger moves, as the market re-prices shares for the lower risk. However, if sales and earnings are not really growing, the price surge can be temporary. The fact that ZYXI had also entered a growth inflection point helped it maintain its price gains. However, we need to point out that a Seeking Alpha author recently published a bearish report on the company.

Pharmchem Laboratories Inc (OOTC:PCHM)

PCHM Is up 463% since we disclosed our long position and bullish research in December 2016. The company makes a drug testing “sweat patch” used by the court system to monitor the level of certain narcotics while offenders are on parole or in rehab centers.

- The stock was left for dead, trading for pennies. At one time, it had been a leader in the urine testing market but eventually fell on hard times when it lost a major contract. The company sold off most its assets, but retained its sweat patch product. Our research indicated that the much smaller sweat patch technology was beginning to gain traction.

- The company was growing revenue and highly profitable, trading at around $0.07 and selling at a P/E of 3.5!

- PCHM declared a 5-cent dividend when the stock was trading at $0.40 and has now paid 4 dividends, totaling $0.28.

- PCHM is currently looking at ways to expand its product portfolio and presence outside the court system.

See the original PCHM article here.

Semler Scientific Inc (OOTC:SMLR)

SMLR was up 358% when we sold the stock in January 2019, 6 months after we disclosed that we were long. It eventually increased by 2300% since a GeoInvesting premium member, Jakewell Parker, published his bullish research, exclusively on GeoInvesting on November 30, 2015. SMLR’s main product is QuantaFlo, a blood flow measurement device used to examine vascular conditions. Our original cliff notes included:

- A strong quarterly earnings report results was the initial catalyst

- An investor in our network who was very familiar with SMLR urged us to take a hard look at the company

- Incredibly strong gross and operating margins allowed the company to reach profitability, which we believed would accelerate rapidly

- Large addressable market

- Product seemed to be superior to the competition it faced

- Cross-selling opportunities with insurance companies due to revenue opportunities their model created for insurance companies.

See the original SMLR article

Stereotaxis, Inc. (OOTC:STXS)

STXS Is up 150% since we initiated coverage in February of 2019. STXS sells a robotic solution for doctors to treat arrhythmias and perform endovascular procedures. The company sells its product suite to hospitals.

- A new CEO and CFO joined the company to fix some of the mistakes that prior management made, such as selling a poor product and incurring too much debt.

- We saw tremendous growth, since only 1% of the target market has adopted robotic solutions.

- Introduced a best-in-class upgrade to its product suite.

- We believe the company is about to reach profitability, alleviating the need to raise substantial amounts of capital to grow.

- Based on acquisition activity in the space, we believe the company is an ideal takeover target. Some investors speculate that STXS could be worth over $10 in an acquisition deal.

- We are not big fans of the capital structure due to preferred stock that was issued when the new CEO arrived to pay down some debt. The convertible preferred stock could result in the company having over 100 million shares outstanding. We generally do not like to buy microcap stocks with over 50 million outstanding shares; as a matter of fact, most of the companies we buy have share counts well under 25 million. However, we made an exception that has paid off, so far.

See our STXS reasons for tracking article.

Electromed, Inc. (NYSE:ELMD)

ELMD Rose 21% during 2016 when we were long the stock and is up 40% since we revisited the story, adding it to our Model Takeover Portfolio in August 2017. However, we currently don’t own the stock and sold shares too soon. ELMD provides airway clearance solutions (SmartVest) to patients with compromised pulmonary functions.

- The company began to make money on nice revenue growth, as the benefits from realigning its sales force started to pay off.

- Activist investor, Red Oak Partners, was aggressively buying shares.

- Management comments suggested that the company was/is well positioned for double digit revenue and earnings growth over the next few years.

- Strong balance sheet.

- Low price/sales multiple for a medical device company.

- Tremendous market potential outside its current core markets.

- We exited the stock too early since revenue and EPS growth became inconsistent. We are very curious to see if the company can maintain a healthy level of growth.

- The company recently reported another strong quarter, but we are still unsure if EPS growth can be maintained, due to comments that marketing expenses will increase moving forward.

Original ELMD article.

Cas Medical Systems, Inc. (NASDAQ:CASM)

CASM was acquired at a modest premium of ~20% in March 2019, about 9 months after we disclosed we were long the stock in June 2018. CASM’s product measures the oxygenation for cerebral tissue during surgery or critical care situations to prevent serious poor patient care outcomes, including death from a condition called hypoxia.

- First class CEO who had an impeccable track record of running three prior medical device companies and selling them to larger companies at attractive premiums.

- Best-in-class product: Independent studies clearly showed that its product was easily better than the comps

- Fixed the balance sheet, creating a pathway to imminent profitability.

- Was expanding the target market.

- Replaced entire salesforce.

- Was about to introduce a product feature that would allow competitor solutions to “bolt” on CASM technology and get the benefits of its improved performance.

- We thought the company would be acquired.

See our original CASM article.

Fonar Corporation (NASDAQ:FONR)

We bought stock in FONR, engages in the research, development, production, and marketing of magnetic resonance imaging (MRI) medical scanning equipment, based on some acquisition activity the company was pursuing that led to the company managing MRI facilities. This move resulted in the company achieving high growth rates for a short period of time. However, we never took a deep dive into the company as we just didn’t see a pathway for the company to achieving high long-term growth at the time. However, the company is producing a consistent level of revenue and profitably. So, we might revisit the story to see if the company is still pursuing an acquisition strategy.

Please see our 2013 note that had us contemplating on performing further due diligence.

Biomerica, Inc. (NASDAQ:BMRA)

BMRA’s performance has not yet reaped any rewards so far, as the market waits for clinical results data and FDA approval on some of its products. Our coverage on the stock began in May 2017. BMRA sells various over the counter medical diagnostic tests.

- Previous CEO who successfully ran the company in the past came back to help the company regain the growth that it had lost.

- Even though the company was not growing and was losing money, it has a proven presence in the market.

- BMRA’s current product portfolio lineup could provide outsized upside potential if the company is successful in gaining FDA approval. If FDA approval does occur, we believe the company could be acquired at a substantial premium over current prices.

- Insiders are funding the company

See our reasons for tracking note.

The Bearish Side of Our Medical Device Company Coverage

On the bearish research side, $GBSNQ, a rapid diagnostic medical test (Nucleic Acid Assay Testing) firm, is trading at $0.02, and for all intents and purposes down ~100% from its reverse split adjusted price of ~$6000.00 when we first shorted the stock and published our negative findings on the company in April of 2015. With the Q designation since March 2018, it appears that the company’s eventually bankruptcy is a fitting end to a saga rife with failures.

- We believed that the company was overhyping its ability to monetize its product portfolio.

- The company had raised money through what we believe to be institutions that had a propensity for funding bad businesses.

- The company was continually raising money through toxic financings.

- A close inspection of the financing documents helped us form an opinion that investors did not have confidence in the business plan.

- We believed that, given the competitive environment, the company would not be able to successfully compete and commercialize to scale.

See our original GBSN report here.