By Maj Soueidan, Co-founder, GeoInvesting

Investor appetite for big cap stocks over microcaps has never been greater than I can recall since I began investing over two decades ago. But, I find that some investors too often make the mistake of associating the market cap of a company with the size of its revenue. This stereotype along with others, such as believing that all microcaps are microCraps, will cause you to miss wonderful stock picking chances.

One of my favorite types of stocks to buy are microcaps that are generating big cap revenue. I call these Big Cap Micros (BCM).

Just take a look at Systemax Inc. (NYSE:SYX), a re-seller of maintenance, repair and operational (MRO) products. Our research team came across the stock in March 2017 after noticing that restructuring initiatives were beginning to stick. With a billion dollars in revenue, and a market cap of $360 million, SYX was a classic BCM. The good news: the stock has exploded since March, rising 38% last week, alone. The bad news: I was not along for most of the ride that has shares now trading at a market cap just shy of $1 billion, or a 170% move in about 5 months.

BCM Defined

Any nanocap, microcap or smallcap investor knows that stocks can go into overdrive when they attract interest from institutions

In a time where lack of liquidity in microcaps has been outside the norm, I find that BCM can entice capital from a wider pool of investors when inflection points are nearing.

In the broadest sense, a BigCapMicro is a microcap stock with meaningful revenue of at least $50 to $150 million. I used to have this criteria set at $500 million to $1 billion, but lowered the threshold to expand my hunting ground and find bullish setups earlier.

You might be surprised to know that many of these companies generate north of $1.0 billion in revenue. These are real companies that debunk negative stereotypes labeling all microcaps as low quality, low revenue-generating companies.

Many times, BCMs already have institutional backing. I generally consider the following as my sweet spot when searching for BCM:

- Currently in a revenue zone between $500 million and $1 billion

- Less than 15 million shares outstanding (the smaller the better)

- Under $20.00 share price

The inflection points that often come with BCM are:

- Top line growth driven by acquisitions

- An increase in organic growth prospects through selling off underperforming assets

- Selling assets to pay down debt and increase margins

- Finding new growth markets from established product lines or retooling them

- Chapter 11 exits

Looking for established companies with revenue between $200 million to $300 million that are embarking on an aggressive acquisition strategy is a great way to find Pre-BCM chances.

Plenty of Opportunities

Most U.S. BCM live on the NASDAQ, NYSE and AMEX, but some special situations also exist on the OTC, especially companies exiting bankruptcies. In total, and after excluding funds, warrants, preferred stock or other non-traditional securities as well as REIT and SPACs, I estimate* that there are over 1500 microcaps and nanocaps trading on the NASADAQ, NYSE and NYSE MKT (AMEX).

| Venue | Total Microcaps | Total Nanocaps | Micros, ex non-traditional | Nanos, ex funds non-traditional |

| NASDAQ | 880 | 883 | 759 | 425 |

| NYSE | 380 | 195 | 143 | 27 |

| AMEX (NYSE MKT) | 131 | 128 | 89 | 100 |

*Data is about two months old.

There is a nice pool to choose from. The trick is to find which ones will find ways to maximize shareholder value vs. which ones will stay the same or become “stale.”

A Few Illustrations – Microcap That “Grew” Up

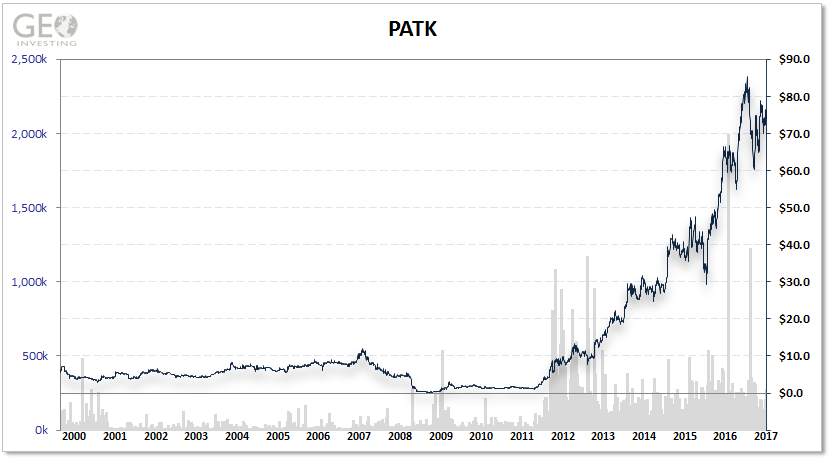

Patrick Industries Inc. (NMS:PATK): Grow through acquisitions

- Industry: Recreational Vehicle Products

- Shares Out: 16.7 million

- Inflection point year: 2010

- Market Cap at beginning of run: ~13 million

- Current market cap: $1.24 billion

- Sales at beginning of run: $278 million

- Sales now: $1.29 billion

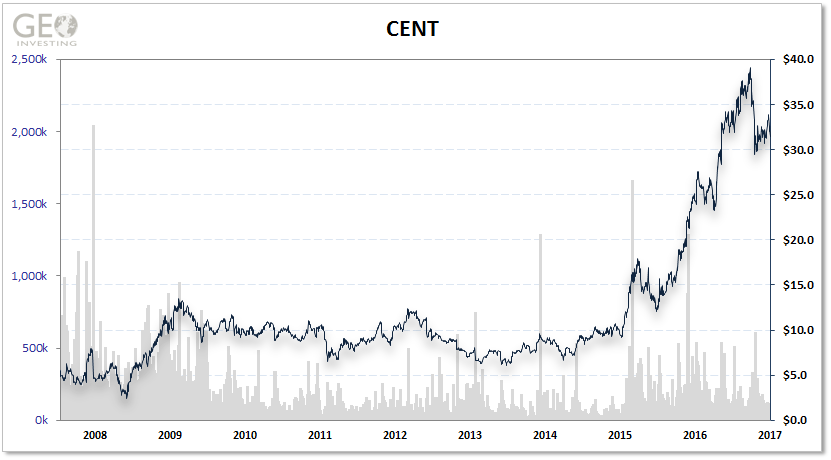

Central Garden & Pet Company (NMS:CENT): Grow through acquisitions and re-tooling of its business segments

- Industry: Pet, Lawn & Garden

- Shares Out: 12.1 million

- Inflection point year: 2014

- Market Cap at beginning of run: ~113 million

- Current market cap: $1.56 billion

- Sales at beginning of run: $1.6 billion

- Sales now: $1.9 billion

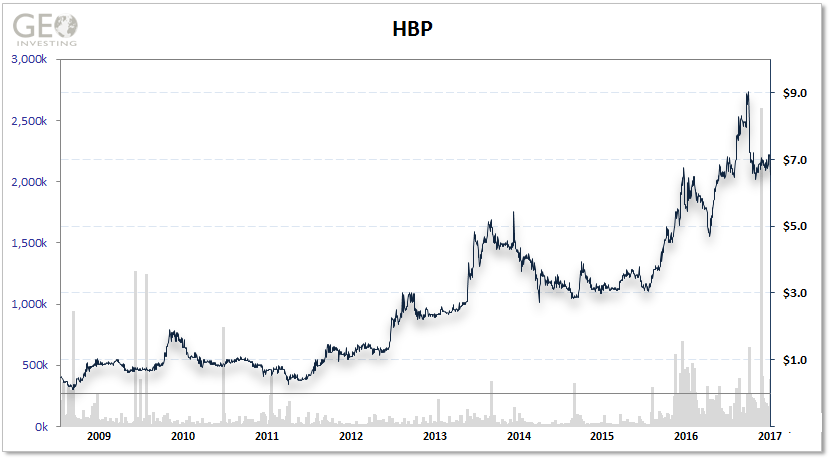

Huttig Building Products Inc. (NASDAQ:HBP): Restructuring and acquisition strategy after the 2008 financial crisis

- Industry: Building Products

- Shares Out: 25.8 million

- Inflection point year: 2013

- Market Cap at beginning of run: ~26 million

- Current market cap: $176 million

- Sales at beginning of run: $561 million

- Sales now: $730 million

—

Maj Soueidan

Great question William.

Well, the biggest key for me, as you might suspect, is management. If I am impressed with management, that goes a long way. And that assessment usually comes through interviews. I remember when I first interviewed $NVEE. I was very excited to learn about management’s past successful history that included a strong acquisition strategy. As you can see, the stock has taken off. $GTT $CENT $PATK are other stocks that have done well growing their companies through acquisitions.

Many investors will just write off companies that make acquisitions. But doing it responsibly is a great way to gain market share, good customers and cross-selling opportunities. You know, that’s what gives us an advantage, when we look at stocks/situations that other investors automatically ignore.

But you are right to be skeptical. When a company makes an accretive acquisition it can often be a great lift to growth for year one. A key test to a good acquisition is if it will continue to contribute to growth past year one. Otherwise, the company will have to continue to make Acquisitions to grow. And then become a serial acquisition maker.

Let me think about your question a little more and see if I can come up with a check list. Thank you

Will

Hey Maj. I also love reading your articles!

Just a quick question. How do you judge whether acquisitions are value enhancing or value destroying because I tend to shy away from serial acquirers, but some of them are obviously doing a good job with this strategy.