I am going to discuss short pitches on two of four very different microcap stocks that are timely in the short-term, but also have long-term appeal; situations where insiders are “backing up the truck”. They also have an information arbitrage (“InfoArb”) theme to them. I have interviewed all four of these companies at some point. I will briefly discuss Eastern Company (NASDAQ:EML) and Mastech Digital Inc (AMEX:MHH). Elevator pitches of the other two names are available here and here. You can also view the full research for the latter two at their respective profiles here at the pro portal.

I know the following quote is probably overused, but it bears repeating. Peter Lynch said it best when he said:

“Insiders might sell their shares for any number of reasons, but they buy them for only one: they think the price will rise.”

A study is commonly referenced to support following the moves of insiders:

“The insider anomaly advantage has been estimated to be as much as 11 percentage points over the market return annually. The advantage tops out closer to seven percentage points, says Ian Dogan, founder of Insider Monkey, who wrote his doctoral dissertation on insider trading.”

Add a little fundamental analysis, and you should be able to improve on this stat by leaps and bounds.

Show me anything I can do to increase my odds of avoiding disaster and I will listen. When it comes to investing, a lot of us like to keep it simple; that’s why I like InfoArb so much. The free and readily available information that is ignored in the microcap space is a gift. You can use it to your advantage to trounce passive investment strategies. Many of you reading this probably agree that following the moves of managers/insiders you respect is another activity that increases the odds for success. Combine it with a little InfoArb, and your portfolio is in good company. It is a great strategy that even beginners can implement.

I thought about Lynch’s quote this morning when one of our GeoInvesting Premium members messaged me:

“Wow, that Guy (CEO & Founder) has been buying shares for as long as I can remember and he’s pissing it all away. Goes to show insider buys don’t always mean good things.”

No doubt, blindly buying shares in stocks where insiders are piling in will not guarantee success. But, when combined with a little research, it can be the best way to highjack cheap shares from impatient investors willing to part with their microcaps. If you don’t have time to interview management, following insider purchases of well-run companies and sprinkling a little InfoArb into the mix probably increases your chances for success to above 90%.

The Eastern Company (EML)

- Price: $27.55 (as of 3/9/2018)

- Annual Revenue Run-Rate: ~$215 million

- Annul EPS Run-Rate: $1.50 to $2.30

- Run-rate P/E: 18 to 12

Background

I wrote about EML in 2017, here and here. Much of the information I am presenting is still the same, except that the stock has become cheaper since my last update and has since reported 2017 yearend numbers. Even though shares have not done much since then, I think the stock has enormous potential. The company fits neatly into the “geek to chic” theme that I love. EML has been around for 160 years, has a stable revenue base, has been solidly profitable every year since data has been available, dating back to 1995, and has paid a dividend for 310 straight quarters. It’s also impressive that the company maintained its revenues and held profitability in 2008/2009. The company has three subsidiaries:

- The Industrial Hardware segment designs, manufactures and markets a diverse product line of industrial and vehicular hardware throughout North America, such as locks, latches, hinges, handles, lightweight composite structures.

- The Security Products segment is a leading manufacturer of security products. This segment manufactures electronic, smart card technology and mechanical locking devices, both keyed and keyless, for the computer, electronics, vending and gaming industries, luggage, furniture, laboratory equipment and commercial laundry industries.

- The Metal Products segment is the largest and most efficient producer of expansion shells for use in supporting the roofs of underground mines

These business lines are, not too exciting, and the lack of growth delivered by legacy management was equally unexciting. But in 2015, Barington Capital, an activist with a great track record, entered the picture, ousted old management in 2017 and inserted their “go to” guy, August Vlak, as CEO. And by the way, value investor Mario Gabelli is also a shareholder.

Geek to Chic

The new plan: Find new growth avenues for existing legacy product lines and bolt on some acquisitions. In April 2017, and subsequent to our published research, management announced it had acquired Velvac, an 80 year old premier designer and manufacturer of proprietary vision technology for commercial vehicles.

This move earned management an A in my book. Ever hear of the concept of “gaining more wallet share from existing customers”? In other words, management finds ways to capture more revenue from existing customers. When you dig into EML’s business, you will notice that their customers include trucking fleets, and Velvac offers fleet management solutions (among other vehicle components). The telematics industry is a hot topic now. Telematics solutions help improve safety and provide operators with useful data so that they can make better operating decisions. Regulation around the globe now dictates that fleets adopt telematics solutions. This, along with the desire for trucking operators to become more efficient, drives growth. Out of the gate, Velvac increased the size of EML by 40%.

Growth Kicking In

All segments are growing organically, which is something you want to see, even when acquisitions are part of a growth story. Q4 2017 results business segment highlights included:

- Industrial Hardware segment grew by 89% and 107%, and excluding Velvac, grew by 11% and 6%, in fiscal year 2017 and the fourth quarter of 2017, respectively, compared to the same periods in 2016, as a result of strong sales growth to heavy duty truck and service bodies customers.

- Security Product Segment sales grew by 7% and 9% in fiscal year 2017 and the fourth quarter of 2017, respectively, over the same periods in 2016, as a result of our investments in growth at Illinois Lock and Argo Transdata.

- Metal Products segment, full year 2017 and fourth quarter 2017 sales were up 45% respectively, over the same periods in 2016. This segment continues to benefit from a resurgence in sales to mining customers and diversification to other industrial markets.

InfoArb

In a nutshell, here are what I purport to be the gaps in investors’ knowledge:

- I don’t think investors have pieced together the telematics angle

- Investors are probably not looking past GAAP EPS numbers that mask the true earnings power of the enterprise. When you get under the hood and strip out acquisition integration costs, you will notice that the company’s annual EPS run-rate is tracking between $1.50 to $2.30 (depending on the persistence of costs to fine tune a new product launch from Velvac.) That means shares are selling at a forward P/E of 12 to 18, but I think shares will carry valuation multiples meaningfully higher from where they are now as management continues to build the company well beyond this current run-rate over time, by penetrating high growth markets and making more acquisitions.

Insiders and Activist Step Up the Plate

Even though management only owns 6% of the stock, some of it was bought at prices as high as $25.75. But, Barington Capital should be considered an insider. Barington Capital owns 9.19% and its General Partner, James Mitarotonda, is also the Chairman of the Board of EML. In May 2017, Mitarotonda scooped up 52,598 shares at $25.90 in a private transaction with another shareholder in May 2017. And don’t forget, Barington inserted Vlak as CEO.

Mario Gabelli owns a 7.8% stake. Gabelli is mostly knows as value investor and, at times, does take a passive activist role in his quest to create value. I would consider Gabelli to be a “quasi” insider.

EML Caveats

- There are certainly risks to the story. There is no guarantee that the company will be able to find the right acquisitions or develop new products that will be adopted by its existing and/or new customers.

- We’re still waiting for the costs associated with the Velvac acquisition to abate.

- Increased leverage to consummate the Velvac business.

- There is difficulty in managing three divisions with a different market emphasis.

Mastech Digital (MHH)

- Price: $12.19 (as of 3/9/2018)

- Annual Revenue Run-Rate: ~$200 million

- Annul EPS Run-Rate: ~$1.25

- Run-rate P/E: 10

Background

The company has two main operating segments: (Source 10-Q)

- IT staffing (legacy): We work with businesses and institutions with significant IT spending and recurring staffing service needs. We also support smaller organizations with their “project focused” temporary IT staffing requirements.

- Digital Transformation IT Services: Following our recent acquisition of the services division of Canada-based InfoTrelllis, Inc., we have added specialized capabilities in delivering data management and analytics services to our customers globally. This business offers project-based consulting services in the areas of Master Data Management, Data Integration, and Big Data, with such services delivered using on-site and offshore resources.

GeoInvesting coded MHH as a GeoBargain on 12/19/2012, $4.40 (adjusted for stock splits) and man, did we get spoiled. The company paid two special dividends in a span of 11 months and reported great numbers. Shares skyrocketed to $19 in 12 months and quickly underwent a 3 for 2 stock split. If that was chapter one in our MHH story, I couldn’t wait for the rest of the book.

As we explained to our premium members, the company was easily exceeding its stated goal of growing 1.5x the IT staffing industry, which was growing at a healthy 6% annual clip with some really nice tailwinds. Its valuation compared to comps like Igate Corporation (acquired in 2015) was significantly depressed. MHH’s growth plan was being led by a new CEO, Kevin Horner, who arrived in 2011. Horner’s initiatives increased the quality of MHH’s product offering which resulted in happier customers and an increase in the wallet share per customer. He also “got more with less” by scaling back staff and creating employee incentive programs. So, what happened?

The reality is that a good deal of potential multi-bagger companies face roadblocks that need to be conquered. In fact, my first question during every management interview is:

“Can you please take me through your history and how you met challenges you encountered?”

As my tennis coach likes to say in his Serbian accent: “I view trouble as challenges.”

Some minor trouble arrived for MHH: over the next 3 years shares slowly grinded lower, eventually touching $5.81 in February 2017.

Even though the IT staffing industry was growing, the rate of growth was slowing, and company margins were getting a little pinched as a result of having to compete for increasing demand for quality IT talent. Furthermore, the company underestimated costs related to a large project and unfortunately, the higher growth areas of MHH business were not large enough to offset what was going on in their “bread and butter” IT staffing business.

In a candid follow up interview I had with management, I got the sense that they clearly understood where they went wrong by not taking a more of a hands-on approach in contract negotiations.

Moving Forward

Management is very aware that it needs to invest in growth as the IT staffing industry growth rate cools (natural evolution as the unemployment rate normalizes). When I first interviewed management in 2012, the IT staffing industry was growing around 6% compared to about 3% today. While the June 2015 acquisition of Hudson expanded the size of its lT legacy business (adding revenue of about $20 million), the 2017 purchase of InfoTrellis (data analytics; big data) is very exciting.

Although InfoTrellis only gives MHH an initial 11% ($22 million) bump to legacy revenue, this move will allow MHH to cross sell data analytics services to its legacy customers and give them a more complete product offering. Its margin profile is also much better than the IT staffing revenue, with operating margins of 26% vs 4%. The addition of InfoTrellis could also lead to higher valuation multiples due to the much higher industry growth rates of the analytics business vs. IT staffing; a CAGR of 12% over the few years.

It should be noted that Kevin Horner left the company in early 2016. Although the board was pleased with the progress MHH made under Horner’s lead, the new President and CEO, Vivak Gupta, appears to have some very deep roots in the IT industry. The company could lean on these roots to reach its next level of growth.

InfoArb

Like EML, the InfoArb for MHH initially stemmed from investors’ failure to look past weak headline numbers when the company reported flat YoY Q3 2017 comps on higher revenue. The legacy business was met with temporary set-backs as expressed by the CEO in the Q3 CC:

“An educated guess would say that probably the hurricane was 50% of the problem and the higher vacations were 50% of the problem.”

Some participants on the Q3 conference call expressed concern over weak organic topline growth at InfoTrellis (which did partially contribute to the quarter). Management responded that, at times, this revenue can be a little lumpy. Regardless, I believe that InfoTrellis will have plenty of room to grow through synergies with MHH’s legacy business. The stock fell from $12.75 to $9.60 during the week following the earnings report. The company has since reported Q4 2017 results, where sales grew 25% to $40.5 million and adjusted EPS rose 68% to $0.32, or a $1.28 annual run rate. Shares are back on track, but still severely undervalued and, I believe, are ready to capture investor interest in the short-term.

Management Loads Up the Truck

Here is the kicker: management (Mastech’s founders and majority shareholders, Ashok Trivedi and Sunil Wadhwani) went all-in on the InfoTrellis acquisition, participating in the $6 million equity portion of the deal, purchasing shares at $7.00, which was higher than market prices at that time. I’ll follow that bet.

Insiders now own about ~75 the recent financing.

Valuation

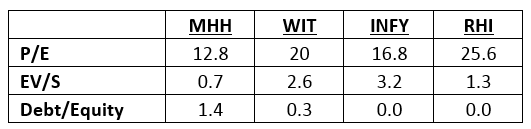

I think MHH is severely undervalued. The management team has done a great job navigating through challenges and is investing in growth to complement its “bread and butter” legacy business. This should lead to an expansion of valuation multiples. Here is a look at how MHH stacks up against comps Wipro Limited (NYSE:WIT), Infosys (NYSE:INFY), and Robert Half International (NYSE:RHI) .

It’s also worth noting that competitor Igate (old symbol IGTE) was acquired in 2015 at the following multiples:

- P/E: 25

- EV/S: 3.0

MHH Caveats

- Legacy business could underperform

- Legacy margins could worsen

- $38 million of debt vs $2.5m cash and cash equivalents

- Higher leverage than comps could restrict expansion in valuation multiples

- Need a deep dive interview with the new CEO