Shares of our Information Arbitrage Pick Golden Enterprises (GLDC:NASDAQ) shot up 58.4 percent yesterday on news that its Board of Directors agreed to sell the company to snack food company Utz Quality Foods, Inc. Note that we sent this email to opt-ins less than a month ago, indicating our intuition that the stock could be a takeover candidate. We call this kind of research Information Arbitrage.

Shares of our Information Arbitrage Pick Golden Enterprises (GLDC:NASDAQ) shot up 58.4 percent yesterday on news that its Board of Directors agreed to sell the company to snack food company Utz Quality Foods, Inc. Note that we sent this email to opt-ins less than a month ago, indicating our intuition that the stock could be a takeover candidate. We call this kind of research Information Arbitrage.

GLDC is an example of how we deliver our successful CALLS TO ACTION to our members.

In this case, we found hidden information in SEC filings that indicated that the company would reverse a trend of declining sales and profitability and that it was a prime acquisition target.

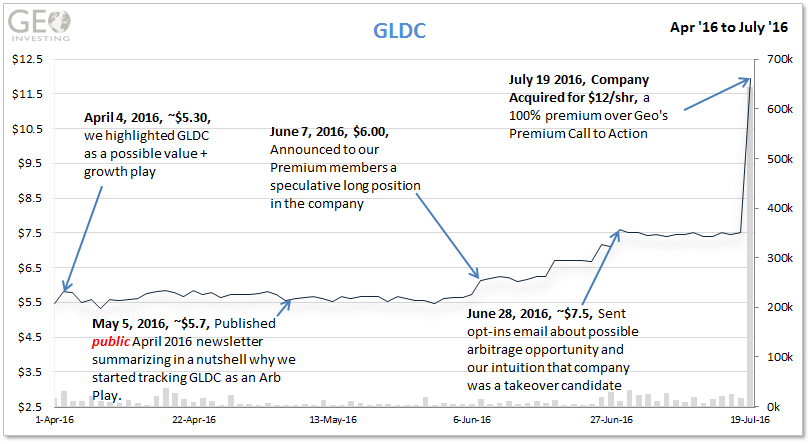

On July 19, 2016, the company’s Board of Directors agreed to sell the company to snack food company Utz Quality Foods, Inc. for $12/share in cash, a 100% premium over our Call to Action sent to Premium members on June 7, 2016.

Below is a reverse chronological timeline of research, literally from the inception of our coverage. This is the kind of grind that we undertake so you don’t have to.

Tuesday, July 19, 2016

GLDC Takeover for $12 per share in cash

GLDC and Utz Quality Foods, Inc. of Hanover, PA (“Utz”) announced that they entered into a definitive merger agreement on July 18, 2016, pursuant to which Utz will acquire the Company and Company stockholders will receive $12.00 per share in cash.

We announced a speculative long position in the company on June 7, 2016 to our members at around $6.00. This is now the newest addition to over 40 picks of ours that have been acquired at premiums.

On April 4, 2016 when the stock was trading at $5.30 we highlighted GLDC as a possible value + growth play, we offered our reasons for tracking which can be read here. On June 20, 2016 we highlighted the possible information arbitrage opportunity that we found in the Company’s filings, leading us to believe the Company may look to put itself up for sale once the common stock trust resolves. See more on this information arbitrage opportunity here.

For a quicker peak, our April 2016 Newsletter summarized why we started tracking the company, ultimately taking a position:

April 4, 2016 — Golden Enterprises Inc. (NASDAQ:GLDC) — An intriguing value plus growth play with activist investor involved. GLDC sells various salted snack and related products. Revenue growth has been steady but slow with EPS lumpy since 2005. We think that is about to change. A 13D filing in August 2015 by an activist investor fund revealed a 5% stake. The filing disclosed that once the fund acquired 8% of the GLDC’s capital stock it would have the right to nominate one person to the Board of Directors. On 10/30/15, the company disclosed the fund’s stake had increased to 8% and one board seat was added to accommodate the fund’s selection. Financial results for fiscal Q2 2016 were uninspiring with revenues down 0.6% compared to the same period in 2014. Management asserted, however, that they do not expect sales to continue to decline and noted improved margins and reduced SG&A as a % of sales. GLDC pays a 3% dividend and is well worth tracking.

We’re happy that GLDC was able to find a way to unlock shareholder value in a much quicker fashion than we thought they were going to be able to.

Friday, July 15, 2016

GLDC Research – Q4 2016 Financial Results

GLDC ($7.31) reported Q4 2016 results:

- Sales of $34.9 million vs $34.0 million in the prior year

- EPS of $0.08 vs $0.06

On April 4, 2016 when the stock was trading at $5.30 we highlighted GLDC as a possible value + growth play, we offered our reasons for tracking which can be read here. On June 20, 2016 we highlighted the possible information arbitrage opportunity that we found in the Company’s filings, leading us to believe the Company may look to put itself up for sale once the common stock trust resolves. See more on this information arbitrage opportunity here.

We are awaiting the 10-Q filing to look over the Management Discussion & Analysis section where management gives more color on future outlook.

Monday, June 20, 2016

GLDC Research – Information Arbitrage Update

GLDC ($6.71) – We have talked about possible information arbitrage opportunities with GLDC in the past. The company has released information in its SEC filings that has not been in its press releases indicating that the declining/unexciting revenue performance that the Company experienced over the last several years may reverse. We noted the following passage:

For the thirteen weeks ended November 27, 2015, net sales decreased 0.1% from the thirteen weeks ended November 28, 2014. For the twenty-six weeks ended November 27, 2015, net sales decreased 0.6% from the comparable period in fiscal 2015. The decrease in the year to date sales is primarily due to the loss of a third party contract that expired at the end of the prior year first quarter. We do not expect to see a continuing trend of declining sales going forward. This year’s second quarter cost of sales was 49.7% of net sales compared to 51.4% for last year’s second quarter. This year’s cost of sales year to date was 49.4% of net sales compared to 50.6% for last year’s year to date. This year’s decrease in cost of sales was primarily due to a reduction in the price of commodities. This year’s second quarter, selling, general and administrative expenses were 47.0% of net sales compared to 48.1% for last year’s second quarter. This year’s selling, general and administrative expenses year to date were 46.7% of net sales compared to 47.5% for last year’s year to date. This year’s decrease in selling, general and administrative expenses was due to reduced fuel cost, reduction in cost associated with our fleet, and efficiencies from our ERP System. The efficiencies gained from the ERP system are expected to continue in the future.”

We also came across a second information arbitrage opportunity that was buried in the Company’s proxy statement:

“The Voting Committee will continue to vote the Company stock owned by SYB, Inc. (5,283,128 shares) and by the Martial Testamentary Trust (600,279 shares), respectively, until the SYB, Inc. Common Stock Trust and the Marital Testamentary Trust terminate. The Marital Testamentary Trust will terminate upon the death of Joann F. Bashinsky and the SYB, Inc. Common Stock Trust will terminate upon the earliest to occur of the following dates: (i) in the event the Company should be sold, five (5) years from the date of the sale of the Company, or (ii) December 31, 2020.”

We think there is a good chance that once the Trust noted in the above quote resolves, that the Company could put itself up for sale. However, this is a longer term catalyst. As we mentioned before, we have had a hard time securing an interview with management. Thus, constructing a valuation scenario on the shares is difficult since we do not know the magnitude by which sales and margins will accelerate (per 10-Q commentary) moving into the future. Per yahoo, based on a trailing P/E of 26, the stock does not look that cheap. The Company is also selling at an EV/EBITDA and EV/Sales of 9.2 and 0.60 respectively, multiples that could see an expansion.

Tuesday, June 7, 2016

GLDC Research – Stock Hitting News Highs

We noticed Golden Enterprises Inc. (NASDAQ:GLDC) hit a new 52-week high today. We previously published our reasons for tracking GLDC on April 4, 2016.

We believed we found an interesting information arbitrage opportunity in GLDC in which we touched upon a potential growth + value proposition. For example, the Company pays a dividend yielding about 2.4% and could be on the cusp of growing its sales and earnings after a long period of stagnant growth. The story also has an activist investor slant to it…White Winston holds a 5% stake in the stock, which we cover in a bit more detail below.

We are still intrigued about the information arbitrage angle of the GLDC story as the stock hits new highs going into its fourth quarter reporting period.

There was interesting material from the Q3 10-Q filing that was not in the related press release. Comments suggested that the Company is about to enter a period of revenue growth and margin expansion, something that we hope they will comment on and/or demonstrate when Q4 results are reported.

Unfortunately, our multiple attempts to contact management have still been unsuccessful, but we will keep trying. We are not big fans of buying stocks pre-earnings without speaking with management first. But due to the information arbitrage due diligence, we will take a very small speculative long position heading into the year-end earnings report yet to be reported (year ended May 29, 2016; Company has 90 days to file).

See our reasons for tracking here.

Tuesday, May 10, 2016

GLDC Research – Attempting to Contact Management

GLDC ($5.59) is a salty snack provider. On April 4, 2016 we highlighted GLDC as a possible value + growth play, we offered our reasons for tracking which can be read here. While the company did not include any revealing information in their earnings press releases, page 11 of the company’s Q2 2016 (end November) infers that better revenue growth may be in the cards going forward. We have reached out to management on several occasions and unfortunately we have not received any response. We will continue our attempts to contact management, but do not feel comfortable establishing a position without learning more about the activist involvement in the Company, a potential catalyst we discussed in our reasons for tracking note.

Monday, April 4, 2016

Now Tracking GLDC

GLDC ($5.30) offers salted snack items, such as potato chips, tortilla chips, corn chips, fried pork skins, baked and fried cheese curls, onion rings, and puff corn. It also sells canned dips, pretzels, peanut butter crackers, cheese crackers, dried meat products, and nuts packaged by other manufacturers using the Golden Flake label

The Company has grown revenues at a steady but slow clip since 2005 but has reported lumpy EPS over the same period.

| 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2005 | |

| REV | $131.7 | $135.9 | $137.3 | $136.2 | $131.0 | $128.4 | $122.2 | $113.4 | $110.8 | $106.5 | $103.1 |

| EPS | $0.15 | $0.08 | $0.10 | $0.19 | $0.26 | $0.36 | $0.17 | $0.10 | $0.10 | $0.02 | $0.00 |

However, we believe the stock is worth tracking due to a 13D filing from August 2015 from White Winston Select Asset Funds, LLC, an activist investor fund.

- At the time of the filing the White Winston held a 5% stake in the stock.

Quote from 13D:

“The Fund acquired a position in the Shares in the belief that they were undervalued. The Reporting Persons have been in discussions with members of the Issuer’s management and Board of Directors since September 2014 regarding ways to enhance shareholder value, and the possibility of representation for the Fund on the Issuer’s Board of Directors.

Since January of 2015, the Reporting Persons have been in discussions with Issuer’s management concerning entering into an agreement with Issuer pursuant to which the Fund would receive the right to nominate one person to the Issuer’s Board of Directors once the Fund owns eight percent (8%) of the Issuer’s outstanding capital stock. The Issuer’s management would recommend the election of such nominee to the Issuer’s Board of Directors and, if approved by the Board of Directors, such nominee would then be recommended to the Issuer’s Stockholders/Voting Committee for election to the Issuer’s Board. The Voting Committee has the right to vote a majority of the Issuer’s common stock and therefore exercises voting control over the Issuer. The Issuer’s management would continue to nominate eleven (11) members of the Issuer’s Board of Directors. The Manager is now in the process of negotiating with management of Issuer an agreement between the Fund and the Issuer providing for the Fund’s right to representation on the Issuer’s Board of Directors, which agreement is subject to approval of the Issuer’s Board of Directors.”

- On October 30th 2015 the company disclosed that Winston ownership stake was at 8%.

“White Winston beneficially owns more than 5% of the common stock of the Company. Pursuant to the Agreement, upon White Winston’s acquiring 8% of the common stock of the Company, the Board of Directors of the Company (“Board”) will be increased by one director and White Winston will have the right to nominate a person to serve as this additional director. The White Winston nominee is subject to the approval of the Board. The Company believes White Winston, as a substantial stockholder, can supply the Company with valuable financial insight and assistance in the Company’s continued efforts to enhance shareholder value. The Company believes that an additional Director nominated by White Winston will be in the best interest of the Company.

- We plan to contact management about this development and get a better understanding of Winston’s plan, whether it is to grow or sell the company.

- While the company does not include any revealing information in their earnings press releases, page 11 of the company’s Q2 2016 (end November) infers that better revenue growth may be in the cards going forward.

“For the thirteen weeks ended November 27, 2015, net sales decreased 0.1% from the thirteen weeks ended November 28, 2014. For the twenty-six weeks ended November 27, 2015, net sales decreased 0.6% from the comparable period in fiscal 2015. The decrease in the year to date sales is primarily due to the loss of a third party contract that expired at the end of the prior year first quarter. We do not expect to see a continuing trend of declining sales going forward. This year’s second quarter cost of sales was 49.7% of net sales compared to 51.4% for last year’s second quarter. This year’s cost of sales year to date was 49.4% of net sales compared to 50.6% for last year’s year to date. This year’s decrease in cost of sales was primarily due to a reduction in the price of commodities. This year’s second quarter, selling, general and administrative expenses were 47.0% of net sales compared to 48.1% for last year’s second quarter. This year’s selling, general and administrative expenses year to date were 46.7% of net sales compared to 47.5% for last year’s year to date. This year’s decrease in selling, general and administrative expenses was due to reduced fuel cost, reduction in cost associated with our fleet, and efficiencies from our ERP System. The efficiencies gained from the ERP system are expected to continue in the future.”

- It appears the company’s margins are benefiting from commodity and oil prices.

- The company pays a dividend, currently yielding around 3%

- GLDC could be the typical value plus growth scenario we search for. Specifically we love boring stocks that have not experienced any recent growth in sales and earnings that will receive a catalyst to enter into a growth cycle, leading to an expansion of valuation multiples.

Caveats:

- Shares are trading at a trailing P/E of 24 which is pretty rich unless we determine growth will substantially accelerate going forward.

- We need to verify non-GAAP EPS figures

Again, we plan to interview company ASAP.