GeoInvesting Weekly Premium Email and Call To Action Updates (July 13 – July 17)

As an investor, you are probably on the lookout for companies that are aggressively targeting large markets. So, I wanted to take a second to talk about TAM or total addressable market:

“Total addressable market (TAM), is a term that is typically used to reference the revenue opportunity available for a product or service. TAM helps to prioritize business opportunities by serving as a quick metric of the underlying potential of a given opportunity.”

Obviously, there is nothing wrong with hunting for undervalued companies that operate in big markets. However, large markets, especially if they are growing fast, can pose challenges to sustaining profitable growth, unless there is a clear advantage or a unique focus. One of the things that stuck with me during my college days is that there is great value in exploring markets or pieces of a market that offer companies a chance to dominate them.

This memory recently resurfaced when I was going over some of my notes from Peter Thiel’s book, Zero to One. Peter Thiel is the co-founder of PayPal and Palantir (about to IPO). I highly recommend that you read his book. It’s an easy read that has some good lessons that highlight some moatish characteristics associated with successful companies and their management teams.

In his book, Thiel reminds us that the less competition, the better. He goes on to stress that many successful companies focus on dominating a small piece of a larger market before going after a larger piece of a target market:

“Every startup is small at the start. Every monopoly dominates a large share of its market. Therefore, every startup should start with a very small market. Always err on the side of starting too small. The reason is simple: it’s easier to dominate a small market than a large one. If you think your initial market might be too big, it almost certainly is. Small doesn’t mean nonexistent.”

In fact, sometimes it may make sense for a company to never expand into larger markets, but keep adding value to their existing target customers. That is why I have always been attracted to companies operating in niche or boring markets, as well as companies that are in a position to capture more wallet share.

While it’s great investing in companies that are capturing new customers at a fast pace, let’s not forget about those that are growing by selling more products & services to a loyal & under-penetrated legacy customer base. It’s where many multi-baggers are hiding. #WalletShare

— Maj Soueidan (@majgeoinvesting) May 28, 2020

I’d like to share three scenarios I prepared for this email to help us identify companies that have moatish characteristics in large and small TAMs:

Category One: A situation where a company has the opportunity to quickly gain market share in its target market that has a small TAM and expand the TAM. We tend to see these opportunities arise with medical device companies selling first class products.

Category Two: A large untapped TAM, where a company has a clear market leading position in a portion of the market that will be difficult for competitors to penetrate. Again, we tend to see these opportunities arise with medical device companies selling best in class products/solutions.

Category Three: A scenario where the TAM is not that big, but dominated by only a few players and where a company has been around for some time. In this case, the growth may not be exciting, but competition will likely not enter the market, and cash flow can be predictable. The cherry on top occurs when a company in this example finds new use cases for its products & services or if the TAM begins increasing a bit.

Great examples of the first two categories are medical device companies we’ve invested in, Cas Medical Systems, Inc. (NASDAQ:CASM) and Repro Med Systems, Inc. (NASDAQ:KRMD). Here is description of CASM’s medical device solution:

“With a simple non-invasive adhesive sensor applied to the skin, tissue oximeters alert clinicians to the oxygenation levels of a patient’s brain or other body tissue during medical procedures to avoid harm caused by insufficient oxygen (desaturation), otherwise known as hypoxia.”

CASM’s solution consists of a monitor that physicians use to read data during surgery and disposable sensors that deliver the data. The efficacy of CASM’s solution is miles better than the competition. In just a few years, CASM went from having a zero market share to a 20% market share by 2018, serving a very specific use case. The superiority of CASM’s solution also opened up the possibility to expand use cases that competing oximeters were being used for. CASM’s TAM was initially estimated to be $125 million, but the company’s product superiority has expanded the TAM to nearly $1 billion.

Furthermore, CASM created a “platform” solution that could actually be used in conjunction with competitor products. Basically, this allowed CASM’s sales force to be able to go into a hospital that was using a competitor’s product and say, “hey, don’t worry about buying our monitor. Just utilize our new OEM platform and better sensors with the monitor you already have, and get more accurate data, get meaningfully better patient outcomes and save money.” The second it became apparent that CASM was about to receive FDA approval for its OEM solution, it received and accepted a premium buyout offer in early 2019.

You can review our research coverage, including our report, on CASM here.

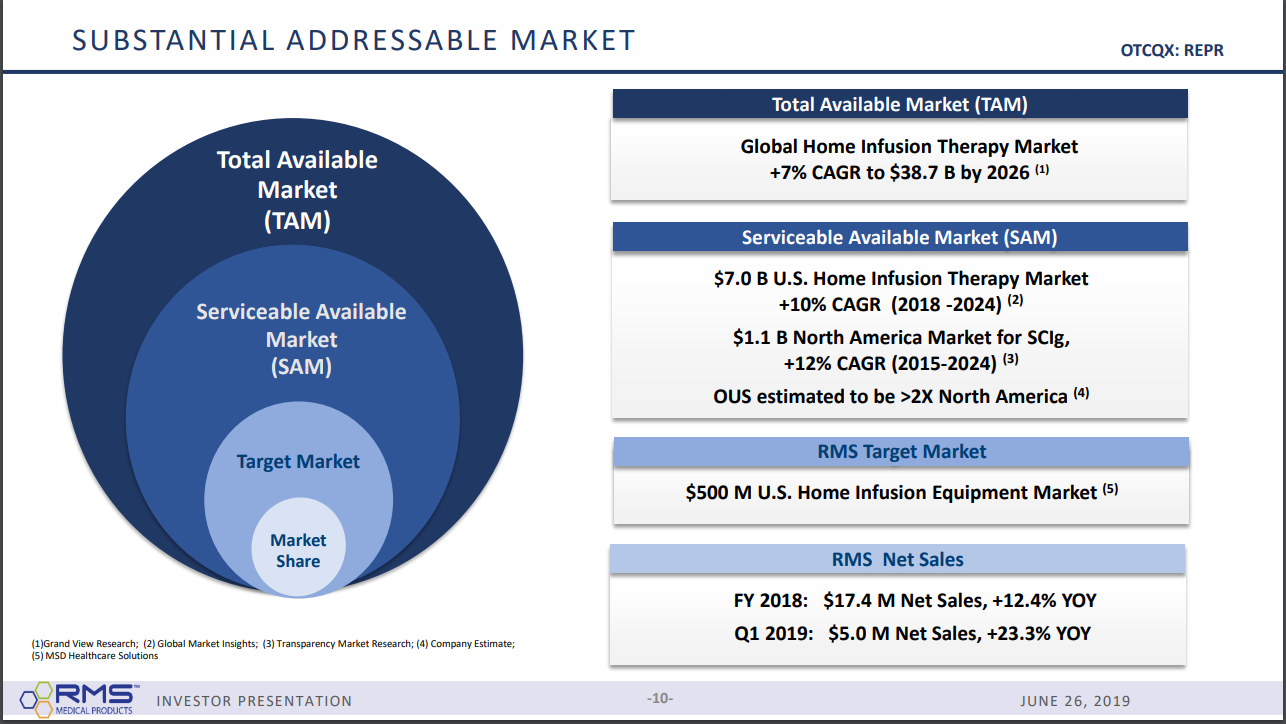

KRMD is a little different in that the company has had a leading market position in its niche home infusion target market (Subcutaneous Immune Globulin (SCIG)) for several years. It is similar in that it has a best in class solution that delivers medication subcutaneously (under the skin), as opposed to intravenously (in the vein) and without the need for electric power. This is a perfect solution to meet the burgeoning growth in demand for home healthcare. KRMD’s competitive position began to get a boost in 2007, when it received a favorable FDA decision regarding medicare reimbursement:

“The Freedom60 Syringe Infusion Pump is the only allowable pump to be billed with the Subcutaneous Immune Globulin (SCIG). All other pumps or modifiers will result in a denial.”

This allowed legacy management to perform a decent job increasing the usage of the company’s solution for limited medical conditions it was already serving. However, a new management team and board that began entering the picture in 2018 accelerated the adoption into current target markets and have been gaining FDA approval to expand the usage of KRMD’s solution to infuse more drugs. These actions have put KRMD in a position to possibly eventually expand outside its $500 million target market to one that is worth several billions of dollars.

You can see our complete coverage on KRMD that began in 2014 at $0.24 here.

You can see more about why we like medical device companies here. By the way, Clearpoint Neuro Inc. (NASDAQ:CLPT) is a medical device company that we believe has some of the same characteristics of CASM and KRMD.

An example of category three is Evans & Sutherland Computer Cor (OOTC:ESCC), a turnaround we first bought at $0.14 in 2014. ESCC Has been providing equipment and entertainment video content to planetariums for over 70 years. The value of Evans & Sutherland Computer Cor (OOTC:ESCC)’s TAM when we first bought the stock was about $65 million per year and had increased to a range of $65 million to $100 million by 2019. Management has also been exploring how it could address other markets to increase its TAM. Well, in March 2020, ESCC agreed to be acquired by a private equity firm at a share price of $1.19. We suspect that things were going on that were increasing TAM and that plans are in the works to enter new markets.

That brings us to a company we referenced in the ‘What to Expect Next’ section of last week’s wrap up that fits firmly into category three. Unfortunately, we can’t publish the report yet since we found some new information on the company’s website that could impact our conviction and valuation assumptions. I will be reaching out to management this week. Please be aware that the stock is extremely illiquid.

Have a great week

Maj Soueidan, Co-founder GeoInvesting

Weekly Wrap Up Summary…

Log in below with your Premium Account to continue reading or join GeoInvesting and please become an Premium Member today.