Since we launched GeoInvesting in 2008, over 20 GeoBargains and/or stock picks that we have presented to our premium members via our email alerts have been acquired. Some of these scenarios were based on good luck. In other instances we were able to predict takeover scenarios based on obvious clues unearthed through our due diligence process; FFEX was one of these instances. Frozen Food Express (old symbol FFEX) was the largest full-service, publicly owned, temperature-controlled trucking company in North America.

After an unsuccessful run as a GeoBargain, on June 4, 2013 we revisited FFEX after stumbling upon a series of 13D filings. The filings contained what we believed to be “no brainer” clues that eventually led to FFEX being acquired for a minimum price of $2.10, or a 40% premium above the price at which its shares were trading at that time. Forty-one days later FFEX announced that the company:

“…entered into a definitive agreement pursuant to which Duff Brothers Capital Corporation will offer to acquire all of the outstanding shares of common stock of FFE (except shares owned by its affiliates) for $2.10 in cash per share of common stock.”

The deal closed on August 19, 2013 and was valued at about 1.5x FFEX’s book value (“BV”)/Share. Interestingly, another trucking company, privately owned Gordon Trucking, was acquired by HTLD for $300 million at 1.5x “revenue equipment and other fixed assets” disclosed in a November 11, 2013 press release.

Well, coincidentally we believe another trucking company, USA Truck (USAK), is a prime candidate for an eventual acquisition. Valuing USAK at 1.5x BV/Share would value the stock at around $15.00. However, as we will later explain, we believe meaningful upside exists to this price target. The market seems to already be casting its vote in agreement since the stock is already trading above $15.00.

We coded USAK as a GeoBargain on November 14, 2013 at $13.35. We stated:

“We established a long position and coded Usa Truck as a GeoBargain special situation play at $13.55.”

Seeking Alpha author MTF Investing did a great job of explaining the “takeout” scenario that is propelling USAK shares:

- On October 27, 2013 – USA Trucks Goes On The Offense With Knight Transportation

- On November 8, 2013 – USA Trucks Vs. Knight Transportation: The Hostile Takeover Continues

We will present our take on the USAK story and why we believe an additional catalyst not mentioned in these two articles should continue to push USAK shares higher.

Like FFEX, 13D filing analysis has been the basis for part of our thesis. Unlike FFEX, we believe that a USAK acquisition scenario has an additional twist to it.

A competitor, Knight Transportation, recently approached USAK to acquire the company at a price of $9.00/share. In a September 26, 2013 13D filing, Knight disclosed an 829,946 share position, or 7.9%, in USAK. Throughout three additional 13D/A filings Knight disclosed that it increased its stake to 1,305,517 shares or a 12.4% ownership interest. USAK rejected the offer. We are aware that Knight made its decision to acquire a stake in USAK after it had received material non-public information from the company. USAK subsequently filed a claim against Knight, citing a breach in confidentiality with respect to the potential acquisition. The nature of the action asserts that:

“USA Truck’s Board of Directors is very disappointed that Knight is doing exactly what it promised not to do: use confidential information that it was provided in the context of friendly and private discussions regarding a negotiated transaction between the companies to initiate a creeping hostile takeover of USA Truck at a price that does not reflect the full intrinsic value of USA Truck. As stated in the Company’s release dated September 26, the Company has previously offered to meet with Knight and remains open to all strategic options that reflect the full intrinsic value of USA Truck, including further discussions with Knight.”

Management went on to state:

“To ensure that USA Truck’s Board of Directors can consider a proposed transaction in light of the recent initiatives undertaken by the Company’s new management team and earnings growth prospects without the threat of continued share acquisitions by Knight Transportation, the lawsuit seeks to require Knight Transportation to restore a level playing field by divesting the shares it acquired in violation of the Confidentiality Agreement.”

These statements clearly show that USAK could be interested in selling the company for the right price. And Knights action not to sell its USAK shares thus far indicates that it has not bailed on wanting to acquire USAK

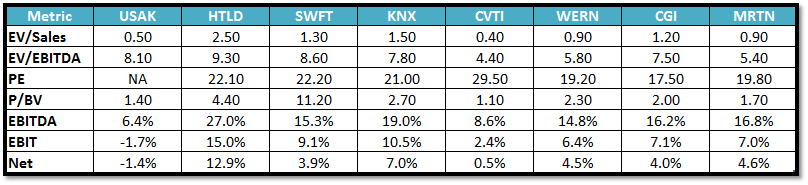

The average Price/Book Value (P/BV) of the trucking competitor set that Knight used in their presentation discussing USAK proposal was 3.43x, or 2.17x, excluding Swift Transportation (NYSE:SWFT) who has an abnormally high P/BV. Assuming 2.17x USAK’s BV of $10.23/share, we get to a price target of $22.20.

Furthermore, a takeover scenario, or one where Knight does not steal USAK from current shareholders, is strengthened by knowledge of the recent purchase of 13.3% of USAK shares by a very successful activist investor (Baker Street Capital) disclosed in a form 13D on November 7, 2013. At the time, the stock was around $13.00. This investor’s involvement also bodes well for an investment in USAK from a purely fundamental point of view in the event that a takeover event does not occur.

The good news is that Knight also said publicly that it would consider raising its bid if USAK’s results improve, a situation that should soon start to bear fruit as restructuring moves recently implemented by USAK management to improve company operations gain speed.

The Obvious Clues Why Knight Will Not Steal USAK

Clue One: Offer Already Rejected

Knight (KNX) recently published a presentation that we interpret as a trashing of USAK. We view this as a classic ploy to keep the stock down so that Knight can try to acquire the company at a lower price. We believe Knight will have to raise its offer significantly to have a chance of acquiring USAK. In fact, we view Knight’s presentation, which attempted to show that USAK was overvalued at today’s levels, is actually an indication of the opposite. Knight seems is so interested in acquiring USAK that it may be trying to artificially depress the stock price in order to acquire the company. If Knight did not care so much about acquiring USAK it could have just given up, since the stock price is far above the original $9.00 offer.

USAK has publicly stated that Knight is not fairly valuing its assets, and that it believes a higher price is warranted. We agree and will discuss later why we think USAK is worth anywhere from $17.00-$40.00.

Clue Two: 13D/G Filing Analysis – Activist Investor Gets Involved

One September 13G filing and two November Form 4 filings show that Stone House Capital Management acquired 1,343,830 shares of USAK, representing a 13.0% ownership interest. Interestingly, Stone House’s most recent Form 4 shows that it purchased shares on November 14, 2013 at a price of $13.56.

On November 7, 2013, Baker Street Capital also filed a 13D where it disclosed that it owned 1,400,000 shares, or 13.3%. Specifically, Baker purchased its shares in two blocks:

- 751,277 at $13.00 on October 8, 2013.

- 648,723 at $12.85 on November 6, 2013.

Combined, Baker Street and Stone House now own 2,705,000 shares, or around 26% of USAK. Essentially, Knight would need their blessing to acquire USAK.

The fact that Baker and Stone House have purchased shares near USAK’s 52-week high, and at much higher prices than Knight’s bid, leads us to believe they also feel that Knight’s bid is too low.

As we will demonstrate, there is a very wide differential between the current market price and where USAK peers are trading. We think a strategic acquirer would recognize this differential and pay substantially more than current prices for USAK. Baker and Stone House likely realize that USAK restructuring initiatives are taking hold and may want to wait for operational improvements over the next 12-24 months, hoping for a sale of the business at a much higher price than current prices. If a sale process is run (which we view as likely given the Baker Street and Stone House interest), we think this value will be realized in the near-term.

Clue Three: Understanding the 13D vs. 13G

Baker Street made sure to file a 13D, as opposed to a 13G, regarding its ownership stake in USAK. Thus, we think Baker Street will lead the charge to maximize value for USAK shareholders. A 13G is filed when an investor intends to be a passive owner in a company. However, a 13D is filed when an investor wants to leave the door open for taking an active role in defining the direction of the company, including the possibility of exerting control.

Clue Four: Who is Baker Street?

“…a value-focused investment firm founded in 2009 by Vadim Perelman and based in Los Angeles.”

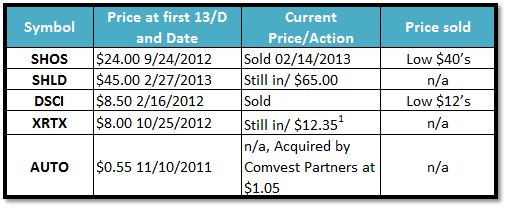

Baker has a knack for making large bets in special situation plays, and winning big. In fact, one of its recent investments was in AutoInfo (old symbol AUTO), a company similar to USAK that also participates in the trucking industry. In November 2011, Baker disclosed that it bought a 9.1% position in AUTO at a price of $0.55. On March 1, 2013 the company was acquired by Comvest Partners for a $1.05, or 90% premium over cost. And Baker is not afraid to pound the table in order to justify its investment positions.

On September 9, 2013 Baker published a 139-page report as to why it thought Sears Holdings (NASDAQ:SHLD), a stock that had been in free fall mode and trading at its 52-week lows, was severely undervalued. The stock shot up 17% on the day of the report and eventually reached $66.00. We would not be surprised if Baker eventually published a similar type of report on USAK. An article published on Seeking Alpha on September 19, 2013 highlights another winning trade by Baker on Xyratex Ltd. (XRTX).

Other Investments by Baker Street:

1Price adjusted for $2.00 special dividend on December 17, 2012.

Clue Five: USAK Turn Around in Full Throttle

Recall a statement we made earlier in this article:

“The good news is that Knight also said publicly that they would consider raising its bid if USAK’s results improve.”

Well, it’s worth noting that in the most recently reported quarter, USAK reported 8.5% EBITDA margins, a dramatic improvement year-over-year from 2.2% EBITDA margins one year ago. Things are improving very rapidly, and USAK actually outperformed its peer group in revenue growth. We think the new management team is highly competent and is improving this business in a rapid and dramatic way. Also, the management team is not necessarily tasked with having to reinvent the wheel. Trucking is a fairly consistent business where solid operators should be able to generate fairly consistent results over time.

USAK hired its new CEO John Simone on February 18, 2013. He has 30 years of operational and management experience in the transportation industry and has worked for companies such as UPS, Ryder, and Greatwide Logistics.

While Knight stated that it would be willing to increase its bid if USAK can show operating improvements, given Knight’s own ability to operate we are confident that if it acquired USAK it could increase the operations substantially. And Knight knows this.

Clue Six: Knight Needs USAK

A USAK investor presentation (Slide 20) filed in October 2013 highlighted Knight might want to acquire USA Truck:

- Knight’s growth has stagnated.

- Reinvigorate Knight’s stock price during slow-growth period.

- Acquire USAK drivers to solve the driver shortage problem.

- Buy USAK market and route strengths east of Great Plains.

- Knight recognizes USAK’s progress before the market fully reflects our value.

Clue Seven: Now That Activist Investors Are Involved, There Is Little Chance That Knight Will Get the Votes To Steal USAK At $9.00

In the words of USAK management from the October 2013 Investor Presentation:

- Knight opportunistically timed its proposal to capture significant shareholder value creation that rightly belongs to USA Truck’s stockholders.

- Offer fails to reflect rapid progress being made under new and expanded management team.

- Offer does not reflect strong prospects for earnings growth.

- USA Truck’s board remains open to all strategic options that reflect the full intrinsic value of the company, including further discussions with Knight.

In the end, USAK is clearly worth more in a turnaround situation than Knight is giving it credit for. We believe a potential suitor could pay much more than where USAK is currently trading and still have it be monetarily accretive.

Valuation: Gaping Hole between Knight’s Bid and What USAK Is Worth

We think it is very unlikely that USAK will get bought out at $9.00 or even at its current price. Below, we show various margins of USAK’s competitors that give reason as to why the company is an attractive investment:

If USAK can get closer to a normalized margin in the industry and trade at similar multiples, the upside from current prices is $30-$40/share.

In a recent presentation, USAK pointed out that if they improve their operating ratio in 2014, they would generate $1.60/share in EPS in 2014. The average P/E multiple in the industry is 18, which implies a $28.80 stock on $1.60/share in EPS. Furthermore, it is clear that others in the industry have generated high single-digit operating margins, in which case USAK could generate even more EPS.

We can understand why Knight is so interested. Again, the average P/BV of the trucking competitor set that Knight used in its presentation was 3.43, or 2.17 excluding SWFT who has an abnormally high P/BV. Assuming 2.17x Knight’s Book Value of $10.23/share, we get to a price target of $22.20. We realize that Knight will not want to pay the average book value of the industry. Even if we assume Knight pays a significant discount to the peer multiples, we still think this transaction could happen in the near-term at a level between $17-$22/share.

Valuation Based on Price/Book Value

We think that looking at this on a P/BV makes sense because we believe that Knight should be able to raise USAK’s margins to a level more similar to that of the peer group. Knight itself trades at 2.6x book value and generates 19% EBITDA margins, one of the highest of the peer group, indicating that they are likely one of the best operators in the group.

Valuation Based on Earnings Power

Looking at this from an Earnings Power perspective, if USAK can get their operating margins to a more normalized level (which they have done in the past without issue), the company could earn $1.60/share in 2014. On a long-term basis, if USAK was able to raise its net income margins to the same level as Knight’s, it would generate $3.22/share on 2014 revenue estimates of $602 million. With comparable P/E ratios in the industry ranging from 17x to 21x, we believe a valuation of $25-$40/share is not unrealistic once the true earnings power of the business is demonstrated. This is why we believe management has stated that USAK is “dramatically undervalued” at the price Knight wishes to take the company private.

Valuation Based on Enterprise Value/Sales

One other valuation method we consider is EV/Sales. The average EV/Sales of the competitors in Knight’s presentation, excluding USAK, is 1.13x. At 2014 estimates (per presentation) of $475 million in sales, that is $537 million EV and a $38.35/share market price. (Please note that analyst 2014 revenue estimates per Reuters are $602 million, which implies upside to this scenario).

So, three different valuation metrics for USAK as well as peer comparisons substantiate dramatically higher prices than today’s prices. Now, given that USAK is currently underperforming its competitors on an operating basis with lower margins, we believe some discount is warranted. However, we think the discount does not accurately represent the difference between USAK’s current price and the various valuations we have presented. We believe a strategic acquirer would recognize this difference, and in this case that acquirer is Knight.

Conclusion:

We think it is only a matter of time before more investors recognize the hidden clues buried in SEC document; clues that have been pushing USAK shares higher. The fact a highly successful firm like Baker Street Capital is investing a good deal of money in USAK shares gives us confidence that even if Knight does not acquire USAK there is value well beyond Knight.

Disclosure: Long USAK