Mikros Systems Corporation (MKRS), is an advanced technology company specializing in the research and development of specialized test and maintenance equipment for the U.S. Navy. The company’s products…

- ADEPT (roughly $100K per unit)

- ADSSS (Price TBD)

… provide the Navy with remote monitoring capabilities of radar and weapons systems on ships.

Our research indicates investors do not fully recognize that military applications for MKRS products actually parallel “hot sectors” in the commercial market that address the increasing desire of companies to implement remote monitoring/data analytics capabilities. Aside from liking the stock on its merits, we think it could be only a matter of time before a large defense contractor acquires the company. This potential move would enable a suitor to capitalize on MKRS’s technology, installed base of products (“installed base”) and recurring revenue stream. In the meantime, the GeoTeam has been accumulating shares while the rest of the market is sleeping.

Shareholder Letter Says It All:

After a low point for the company in 2013 MKRS seems poised for a turnaround. Following are some excerpts from the company’s April 3, 2014 2013 fiscal year shareholder letter issued by Chairman, Tom Meaney:

“I am pleased to report some important developments that occurred over the past year which we expect to lead to increased revenue and profitability for Mikros in 2014 and 2015. We have expanded the capability and reach of our core ADEPT® product to other markets and ship classes, solidified our presence in Largo, Florida, a key defense industry hub, and aggressively explored commercialization of the core technology developed under our U.S. Navy R&D partnership.

We also accelerated our pursuit of potential non-defense markets. We believe that many of our core capabilities, including remote monitoring, rugged systems, predictive maintenance and communications expertise, could be applied to other industries which work with complex distributed systems. Targeted industries include utilities, communications and transportation systems. As an initial test case, we are currently exploring applications in the railroad industry, including discussions with industry leaders about potential joint ventures.

In closing, we believe that we have weathered the worst of the storm and positioned Mikros well to resume future growth.”

Patient Investors Should Be Handsomely Rewarded

The decline in MKRS’s share price from its all-time high in 2007 has likely been the result of the 2008 global recession and the related uncertainty over US government budgeting decisions that should have been routine contracting and funding decisions. MKRS, like virtually all government contractors, was greatly affected by the inability of congress to reach a budget agreement in 2013 and the resulting sequestration. We have interviewed and visited with management on several occasions and are convinced that if a few chips fall in the right places a sea change will soon be upon the company.

MKRS trades on the pink sheets but is fully reporting. The company has no debt, is sitting on $0.04 in cash per share and is armed with a management team with deep roots in the defense industry. Trading at around $0.10, MKRS is well off its all-time intra-day high of $1.05 reached in June 2007. It is interesting that during this time Mikros had grown its top line for five straight years and generated revenues of $3.1 million, basically what revenues were in 2013. Now, after six years of inconsistent growth, we think the company is in a position to embark on a multi-year period of growth and will be doing so from a higher base with a well- established product and far more certainty regarding its future prospects. Also helpful is that, at least for now, congress is behaving reasonably which has removed some ambiguity and should expedite the implementation of an ongoing Navy Modernization Program (“NMP”). Furthermore, China’s acceleration of its own NMP and recent aggressive activities in the South China Sea compels the U.S. to keep pace.

We see a rapidly growing value proposition for the company based on its proprietary technology that will ultimately be recognized by either the market and/or a large defense contractor acquiring the business. At $0.10 and assuming average performance by the business, we see very little downside risk. In our opinion, the greater risk is in missing the MKRS “ship” as it leaves the dock and sets sail to a bright future. We believe that this voyage will be relatively soon. One near-term catalyst would be the company’s progression into securing new contracts for the ship class that it has been serving for the past few years, AEGIS. In fact, it appears that the company is in the late stages of product testing with the U.S. which we believe will reignite interest in its stock.

“Mikros Systems Announces New Contract Awards in 2014: The initial production order for three (3) ADEPT systems will be the first production order with the newly developed chassis. It is anticipated that a much larger order will follow later this year to further outfit the Aegis combatants.”

A more powerful launching pad for the stock would be the company’s entry into ship classes other than AEGIS. Over the next several years, the total revenue potential for MKRS’s addressable market in just the Navy (detailed later in this report) for their lead product (“ADEPT”) is around $70 million. The mid/longer term opportunity is much greater, considering the prospects of its newest product (“ADSSS”), and of its remote monitoring products serving, commercial applications and military segments outside the Navy.. Once the company begins to realize an acceleration of contract wins, investors should find the currently depressed shares to be a potential multi-bagger opportunity.

MKRS products and business drivers

The foundation of MKRS’s business lies in the company’s proprietary ADEPT technology. The company’s products are:

- Adaptive Diagnostic Electronic Portable Testset (“ADEPT”). Currently the majority of product sales, ADEPT is deployed in large quantities on some of the Navy’s AEGIS cruisers. Two to Three ADEPT units are required per AEGIS. ADEPT is portable.

- ADEPT Distance Support Sense Suite system (“ADSSS”). This can be viewed as the “sexy future” where the company takes remote monitoring to a new level. Multiple ADSSS’s are permanently installed on ships, and are currently being considered for use on the LSC ships, potentially opening up a new revenue stream.

Revenue Cycle:

- Engineering Sales – Customers pay MKRS to develop, manufacture and install a limited amount of product. This phase of the product cycle in a government project is often referred to as low rate initial production (“LRIP”).

- Product Sales- Installation of ADEPT and ADSSS on large scale.

- Recurring Maintenance and Support- Routine maintenance on installed product (every two years on AEGIS)

Reasons for Optimism:

1. 2013 Was A Difficult Year, But More Importantly, Possibly A Transformative Year

Mikros’ business depends on the timely and ongoing receipt of task orders and funding from the U.S. Navy to maintain consistent business flow and operations. 2013 proved to be a very difficult year. Political wrangling in congress froze the normal contracting and funding processes for the US Government directly disrupting MKRS’s business. Under the circumstances, management could have laid off engineering staff to cut costs and maintain profitability. Instead, the decision was made to invest in the business by maintaining staff levels and other operations. In addition, management invested in a redesigned chassis (less cost, easier to manufacture and more efficient) for the next generation of the company’s flagship ADEPT product and an upgraded production facility that expanded capacity needed to keep pace with anticipated demand in 2014 and beyond. That decision has paid off as the company was adequately staffed and prepared to aggressively execute on business opportunities now that government contracting and funding is back on track. The benefits of making sound and prudent decisions by continuing to invest in the business during hard times should carry forward throughout 2014 and into the future. That is one of the key factors that drew our attention to MKRS.

2. The Company’s products are essential to monitoring and maintaining weapons and radar systems as well as helping the Navy reduce maintenance costs.

Key benefits of the MKRS product offerings include:

- Distance support capability enabling “expert” remote (shore-based) system support and fleet-wide system analysis;

- Reduction in the amount of electronic test equipment required for organizational level support; and

- Modularity and programmability which aims to overcome obsolescence with ongoing programming updates, cycled maintenance and product enhancements that allow the product to hold its “real estate” on the ship once on board. This makes the products ever-evolving as lessons learned from issues encountered with current test equipment and support capability are reflected in future systems.

There should be no doubt that MKRS is selling a product that the military actually needs and uses. MKRS’s products ensure that weapons and radar systems on naval ships are functioning properly. Its lead product, ADEPT, is in its second generation and weighs 22.5 lbs. In laymen terms, sailors carry ADEPT to different parts of a ship to connect it to highly sophisticated radar systems to make sure they are functioning properly and to determine if maintenance is required. Data is stored in the memory cards of ADEPT so that it can be viewed on deck or sent to headquarters on shore.

“ADEPT represents a new approach to Navy shipboard maintenance, integrating modular instrumentation cards in a rugged enclosure with an onboard computer, input and output devices, networking hardware, removable hard drives, and a touch screen display. A custom software application provides the user interface and integrates the hardware with a database that stores user information, instrument readings, maintenance requirements, and training aids. ADEPT is designed to be adapted to other complex shipboard systems, and to provide integrated distance support capabilities for remote diagnostics and troubleshooting by shore-based Navy experts.”

Aside from the national security advantages ADEPT offers, radar and weapon systems cost billions of dollars, so it’s essential to catch problems early.

We are especially excited about ADSSS, a new ADEPT product that is permanently installed into various systems on naval ships so that naval officers on and off shore can share real time performance and maintenance information. This product helps address problems earlier, offers more efficient logistical solutions and reduces inventory costs. Equally important, it also reduces headcount and personnel costs on the ships. Through our research, we learned that naval officer and other personnel costs are the greatest long-term expense for the Navy. The incremental revenue that MKRS can generate from ADSSS is significant since it will likely require more installations per ship. An attractive aspect about ADSSS is that it complements and works in conjunction with ADEPT’s increasing overall efficiency. The advantage of ADSSS is that it collects real time data on an ongoing basis which helps sailors better pinpoint where problems exist, quicker, taking the guesswork out of where to take ADEPT when required. Since the ADSSS can’t be installed everywhere on a ship, there is still the need for the ADEPT “portable” solution. If the ship is using one of the products, it also needs the other.

3. Increasing Backlog Potential And The Quicker Release Of Task Orders

The Navy modernization program is intended to ensure that the ships can be operated optimally and cost-effectively throughout their entire 35- or 40-year intended service lives.

“The Navy has begun a program to modernize its 22 in-service Aegis cruisers and the 62 Aegis destroyers procured in FY2005 and prior years. Under Navy plans, the modernization of these 84 ships would occur over a period of more than 20 years. The program’s estimated total cost is about $16.6 billion in constant FY2010 dollars.” March 31, 2010 article

MKRS’s backlog consists of contracted engineering services and product sales. Backlog is realized as task orders are released by the Navy. The military tends to release task orders in small batches over time. Being at the mercy of government bureaucracies is an issue for MKRS and other defense contractors who have experienced delays in the issuance of task orders, particularly during periods of domestic political turmoil.

The question now is will the U.S. Navy ramp up its modernization program? We think the answer is yes. The resolution of the 2013 U.S. budget fiasco which provided more visibility into the amount of money that will be spent on defense initiatives should result in an increased willingness of the Navy to award contracts and accelerate the release of task orders. More importantly, the Navy is feeling pressure from China. China’s military modernization efforts, including those targeting its naval fleet, have ramped up in recent years. China has doubled its defense budget over the last six years which has put its navy on pace to become second only to the U.S. in military shipbuilding technical capabilities and possibly meet or exceed the U.S by 2030. It is likely that the U.S. will increase its efforts to maintain its edge over the Chinese naval fleet and retain its status as the world’s military superpower.

As a part of the U.S. strategic rebalancing toward the Asia-Pacific region announced in January 2012, Department of Defense (DOD) planning is placing an increased emphasis on the Asia- Pacific region. This should result in more emphasis by DOD planners on U.S. naval and air force initiatives. Administration officials have stated that notwithstanding constraints on U.S. defense spending, the U.S. military presence in the Asia-Pacific region will be maintained and strengthened. February 28, 2014 article.

In MKRS’s 10K 2013 , the company states:

“We intend to capitalize on the Navy modernization program, which could result in two or three ADEPT units being placed on each destroyer and cruiser in the U.S. Navy, with the potential to install multiple units on additional U.S. Navy ships and submarines.”

This is a key step for the MKRS growth story to reach a whole new level. The acceptance of ADEPT products on ships other than AEGIS in the Navy fleet would be a transformative event for MKRS.

We also think that the ADSSS, as a high tech option, will gain significant contract momentum within the Navy.

Finally, MKRS management has recently invested in engineering resources that could facilitate participation in subcontracting opportunities with large defense contractors, something the company was not been equipped to pursue in its past. The ability to serve as a subcontractor with much larger players should open new revenue streams for the company and more consistent order flow.

4. Market opportunity

There are ample opportunities to greatly increase the deployment of ADEPT in the U.S. Navy fleet beyond the existing AEGIS class cruisers and destroyers. MKRS has installed over 50 ADEPT systems on 50 AEGIS ships since it received its first contract on October 12, 2009. In order for this story to resonate with investors, they need to be convinced that ADEPT has broader applications in the U.S. Navy than just the AEGIS fleet. Management understands this…

“Mikros is also proposing to apply ADEPT to conditioned-based maintenance applications on other naval platforms, such as amphibious ships, carriers and submarines. Combined, these platforms have the potential to generate wide placement of ADEPT Units and multiple additional orders throughout the Navy.”

Investors are largely unaware of the opportunities available to MKRS and its ADEPT and ADSSS products. That’s because MKRS’s management team is focused on building the business, not promoting the company and its stock. Management is, however, mindful of its investors and we think they are committed to ramping up future communications, as appropriate, to keep them informed of opportunities that are on the horizon and within reach. For example, the company has not aggressively promoted the progress of its ADSSS initiative and its market potential. The GeoTeam had representatives at the Surface Navy 26th National Symposium conference held in Washington D.C on January 14-16th and we learned that the Navy personnel involved with the Littoral Combat Ships (“LCS”) are excited about ADSSS and the product is in the final stages of testing with positive results. The U.S. Naval Fleet is expected to add 32 to 55 LCS’s over the next 5 to 8 years.

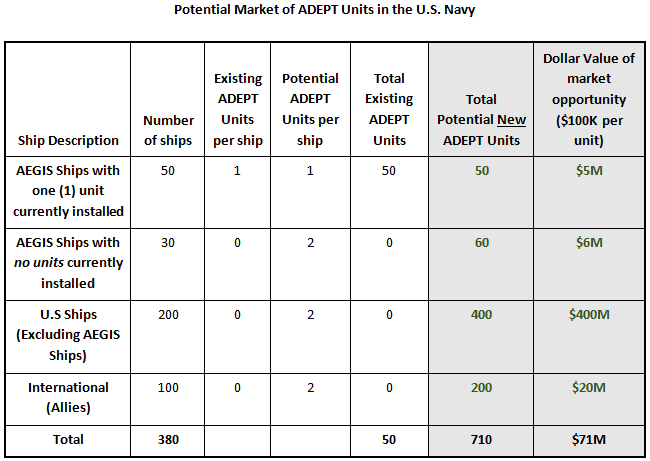

The following chart reflects the potential addressable market for ADEPT in the U.S. Navy and our allies, and does not even include potential revenue from ADSSS which we think could be much larger.

In addition, there are 25 to 30 on-shore stations that will need ADEPT-related equipment. As China grows its Navy and as North Korea becomes more of a “pest” we think our allies represent a meaningful international market for MKRS to address.

In total, we calculate that the product revenue potential just from ADEPT is roughly $70 million. In addition, each unit deployed will generate future revenue for calibration, routine upgrades and maintenance on an ongoing basis. This adds an annuity element to MKRS’s revenue stream.

The company is also pursuing opportunities to expand the reach of ADEPT. Management believes the technology has broad appeal in both the military (Marines, Army, Air Force all have radar and weapons systems) and commercial marketplaces. The state-of-the-art remote test capabilities can be used by many commercial and government customers such as the FAA, radio and television stations, cellular service providers, trains and airlines. In fact, we understand the company is currently in discussions with a railroad company, and addressed this development in the CEO’s 2013 shareholder letter. Because this letter was not widely published, we don’t think most investors are aware of this development. If the ADEPT technology gains traction with commercial customers it could be a game changer for MKRS.

MKRS Revenue Streams And Business Drivers

The ADEPT systems generate revenues through the sale of equipment (two per ship averaging around $100,000 each), engineering services related to the technology (cost plus fixed fee basis) and periodic calibration and scheduled maintenance of the equipment. The most profitable source of revenues and key driver for the business is ADEPT manufacturing and unit sales. Each new system deployed increases MRKR’s installed base on board the Navy AEGIS fleet creating new opportunities for the business.

Engineering contract services are another source of revenue that are critical to MKRS’s long term success. Engineering services benefit the company by enabling the billing rates for engineers to cover direct payroll and overhead costs and can generate a modest profit for the business. Essentially, the client is funding development efforts to enhance existing products and develop new technologies that become Intellectual Property owned by MKRS and available for other applications and uses.

Other benefits arise from the recurring and nonrecurring revenues generated by the installed base. An example of non-recurring revenues is an ongoing project to convert the operating system software from Windows XP to Windows 7. Alternatively, recurring revenues are generated by scheduled calibration, upgrades and maintenance of the equipment every two years. Furthermore, ongoing maintenance of the ADEPT units creates an ever evolving, long-lived asset that, once deployed, stay on board for as long as the ship is in service.

ADEPT systems essentially own real estate on long-lived Navy ships

Based on our research, we think the value of the ever-growing installed base of ADEPT products is underappreciated and, therefore, undervalued by the market. The ADEPT systems essentially own real estate on the ships serviced. AEGIS cruisers and battle ships remain in service for 30 to 35 years and carriers, for 50 years. Once installed the ADEPT systems are likely to stay on board for the duration. That is made possible by ongoing product enhancements and cycled recalibration and maintenance of the systems. As the successes of the installed base become known, so too do MKRS’s and ADEPT’s brands. This is a classic example of success ultimately leading to more success.

A recent example of how the success of the ADEPT technology and growth of the installed base has benefited MKRS is illustrated by an important new development contract that was awarded to MKRS in February 2014. The contract extends the ADEPT system to a second Navy radar system, the SPS-49. The AN/SPS-49 is a U.S. Navy two-dimensional, long range air search radar built by Raytheon that can provide contact bearing and range. The SPS-49 is a primary air-search radar for numerous ships in the U.S. fleet.

5. ADEPT’s Position with the U.S. Navy Is Secure

MKRS has a long-standing and solid relationship with the Navy based on its proven track record of developing innovative technology. In the 1980’s MKRS developed a state-of-the-art military radio frequency and underwater data communications that is still being used by the Navy. In the mid 1990’s MKRS developed an advanced Digital Signal Processing (DSP) technology which was used for high-speed data broadcasting techniques utilizing the commercial AM and FM radio spectrum.

MKRS’s successful initiative in the 1980’s and 1990’s served as preludes to the development of the ADEPT technology, which was originally designated as the Multiple Function Distributed Test and Analysis Tool and began as a Small Business Innovation Research (“SBIR”) investigation in 2002. Since then over 50 systems have been successfully deployed and new opportunities both with the AEGIS class cruisers and destroyers, as well as for other classes of Navy ships, are opening up. The ever growing installed base of ADEPT systems is the springboard for future growth.

MKRS’s longstanding relationship with the U.S. Navy and experience with government contracting puts the company in a solid position. That’s because the complex government contracting process creates barriers to entry once a contractor has its equipment and technology deployed. The ADEPT systems deployed to date have all been under the SBIR program. It requires an exacting process and specific knowledge of and compliance with government contracting procedures. Winning acceptance in the SBIR program is a very competitive process. The SBIR program is defined as follows:

“The Small Business Innovation Research (SBIR) program is a highly competitive program that encourages domestic small businesses to engage in Federal Research/Research and Development (R/R&D) that has the potential for commercialization. Through a competitive awards-based program, SBIR enables small businesses to explore their technological potential and provides the incentive to profit from its commercialization.”

MKRS utilizes indefinite delivery, indefinite quantity (“IDIQ”) contracts to perform government work:

Indefinite delivery, indefinite quantity contracts provide for an indefinite quantity of services for a fixed time. They are used when GSA can’t determine, above a specified minimum, the precise quantities of supplies or services that the government will require during the contract period. IDIQs help streamline the contract process and speed service delivery.

Under the terms of the current contract to deploy ADEPT on the AEGIS fleet, the Navy can’t award other companies a similar contract covering the same product for five years after the last contracted ADPET is placed on a ship. So unless better technology comes along, MKRS will be ingrained in the Navy.

The fact that AEGIS appears to be close to awarding MKRS another long-term contract should solidify its standing with the Navy.

MKRS Staff Have Technical Expertise Navy Personnel Do Not Possess

There were times in the past when the Navy attempted to reduce spending on the ADEPT program by utilizing its own personnel to perform certain functions on its own, thereby avoiding the requisitioning MKRS’s services. In a sense, the Navy became MKRS’s greatest competitor for certain functions. That tact, however, did not work out. That’s because sailors are already taxed with keeping the radar systems running properly and they simply don’t have the time or expertise to do the work of MKRS’s engineers on the ADEPT systems. These circumstances only served to bring the need for MKRS engineers into focus and cement the company’s relationship with key Navy personnel.

Valuation scenarios

We think the company is in position to generate $5 to $6 million in revenue and $0.02 EPS in 2014, provided it receives a follow-on contract from AEGIS relatively soon. If the company is able to monetize its current discussions with the rail company our estimates would prove to be conservative. (This is more of a post-2014 development) Furthermore, we have not baked in any revenues from its ADSSS product.

In the near-term we think investors will be willing to push shares much higher if the company is able to secure an IDIQ contract with AEGIS, as it has inferred to be in the works in a recent press release.

- Worst case short-term scenario: P/E 15 * $0.02 EPS estimate = $0.30 per share

- Mid-case short-term scenario: P/E 25 * $0.02 EPS estimate = $0.50 per share

- Best case short-term scenario: Flirts with the all-time highs of around $1.00 per share attained in 2007 when revenue was around $3 million.

Past 2014, management has to prove it can execute its strategy for diversified growth and give more color on the prospects for each component of revenue.

Caveats

- It is not a guarantee that MKRS will receive follow-on order for AEGIS.

- Expansion past the Navy could be challenging.

- Adequate capital to fund expansion may be required.

- Uncertain impact of dysfunctional government. The government sequestration issue could resurface in 2016.

- Meaningful reduction in number of expected ships would translate into reduced product deployment.

Disclosure: Long MKRS