Summary

- A letter on October 5th from the California State Office of the Bureau of Land Management continues to paint a bleak picture for CDZI’s focus — its ongoing “water project”.

- This reconciles with, and further validates, past critical articles suggesting that the project is doomed for eventual failure and, as such, the company may be as well.

- On top of its main business operation looking like an impossibility, CDZI faces a major liquidity crisis and has enormous debt coming due.

- As it stands, CDZI’s balance sheet is insolvent and the company’s equity is worth $0 dollars on paper with seemingly no future road toward profitability or cash generation.

- Without steady profits, we value CDZI at what it’s worth on paper and believe it’s is on its way to $0, be it from bankruptcy, eventual dilution or other means.

The short case on Cadiz Inc. (NASDAQ:CDZI) is centered on two damning points: the company’s main business project (a water project focused on relocating water from an aquifer in the Mojave Desert) seems doomed for imminent failure and, in the meantime, CDZI has an insolvent balance sheet and has posted a loss the last 42 quarters straight.

The fact is that the company is essentially a one trick pony and has been working on the same “water project,” as they call it, for years, with very little tangible progress being made on the necessary regulatory front, while enriching insiders and burning through millions of dollars. The project’s recent resurgence, seemingly the only reason to potentially buy the stock, has been called, “the latest version of a proposal that’s been floating around for more than 15 years.”

Or, as the LA Times put it yesterday, “Cadiz was the brainchild of an investment promoter named Keith Brackpool, who came to the U.S. after pleading guilty to criminal charges relating to securities trading in Britain.”

This project was the one potential success story the company had and was dealt a massive blow just days ago that we think will be extremely detrimental to the company. Don’t take our word for it – the company has even stated themselves, in their 10-Q, that their ability repay their debt and remain liquid depends on the success of this project.

While this has been ongoing, CDZI has been looting its balance sheet andlosing money quarter after quarter, for years.

It has been argued exhaustively that CDZI’s water project has been, and will continue to be, a complete failure. For those unfamiliar with CDZI, this project represents just about all of the future prospects that investors are seemingly betting on when they are buying CDZI stock. This detailed and lengthy take down of the company’s water project, published in April 2015 by The Pump Stopper, is a must read as a pre-requisite for those reading this article and looking to familiarize themselves with the criticism surrounding CDZI.

Today, we take the next step in identifying what we believe to be an extremely promising short case against CDZI. Since the water project has been opined on at length, we’re only going to look at recent developments from the California State Bureau of Land Management and how they seem to validate past reports. Finally, we’re going to take a look at the company’s alarming liquidity crunch, insolvent balance sheet and perpetual cash burn.

Recent Regulatory Correspondence Confirms Short Thesis

The latest, and arguably the most threatening roadblock the company has faced is in a letter they received from the US Department of the Interior in early October. The letter notifies the company that it would not be allowed to use a loophole that the company was seeking to use in order to move its water pipeline project forward (“cannot be authorized”).

The letter cites not just one issue with the company’s plan, but rathernumerous issues that it takes exception with:

- the water conveyance pipeline

- the fire suppression system

- an access road

- power lines

- the excursion train

The letter makes it abundantly clear that CDZI is not furthering a railroad purpose, mentioning those words specifically numerous times.

The request was seeking to package CDZI’s water pipeline project in with late 1800’s railroad regulations that allowed usage of public land relatively freely for those looking to further a “railroad purpose”.

This KCET report states:

Cadiz had argued that its proposed 43-mile pipeline along the right-of-way of the Arizona California Railroad (AZCR) would have augmented the safety of railroad operations, by providing water for firefighting along the railroad’s right of way through one of the least-vegetated sections of the Mojave, as well as drinking and cooling water for possible passenger excursions. If that argument had flown, Cadiz could have taken advantage of a loophole of sorts that would have exempted the pipeline — and thus the whole project — from federal environmental review. Cadiz is asking that the determination by California BLM chief Jim Kenna be reviewed by Kenna’s boss, BLM Director Neil Kornze, but the chances that Kornze would countermand Kenna’s call are slender.

Veteran Southern California water wonks will be well acquainted with Cadiz: it’s the latest version of a proposal to mine the aquifer in the Cadiz and Fenner valleys south of the Mojave National Preserve that’s been floating around for more than 15 years. When first floated in the early months of the 21st Century, the Cadiz project would have provided 50,000 acre-feet a year to the Metropolitan Water District.

The company’s plan was to tuck its pipeline into this exception, as this would be a way around Federal Review of the company’s project, which we’re guessing the company does not want to happen, as it has been called a death sentence for the project by the Pump Stopper (http://pumpstopper.com) (“already effectively failed Federal Review”, “project failure and bankruptcy”) and here (“may kill the project”).

This is important because this exemption was seemingly the only back ended way that the company could conceive of getting approval for its project. It has widely been regarded that if the company needs to seek a federal review, the project might as well be considered dead.

As the KCET report puts it succinctly, again,

In essence, the seemingly minor “administrative determination” means the company will likely have to put its project through a full federal environmental review if it’s going to proceed. And that meansfederal hydrologists will cast a critical eye on the company’s claims, and that may kill the project.

This is the stage the company is at now. We think this project, and CDZI, are as dead as a doornail.

The has a very slim “hail mary” chance of getting the BLM to overturn the appeal, as it says in the letter that it’s not technically final – but we believe the issues that would have to be addressed in order to make such an appeal worthwhile are far beyond the realm of what is possible at this point in CDZI’s lifecycle. In another “bullish scenario”, the company may have to tack many additional years onto its timeline while somehow dodging bankruptcy. At the worst, the end appears to be very near. We believe the Board of Directors needs to look very carefully at the best options for CDZI and its creditors at this point.

The company’s method of disclosing this recent letter is also interesting. The company’s disclosure methods surrounding this project had been in question for some time in prior critical articles. Adding to that contention, we would like to review the crux of the letter that the company saw and compare that with the headline that the company put out to investors.

Here is what the company saw in the letter:

And here is what they handed investors:

Guidance? Yes, they were “guided” that their project “could not be approved”.

And this isn’t the first time the company’s disclosures have been in question. Asecurities fraud suit claiming the company misrepresented its business practices surfaced in 2015.

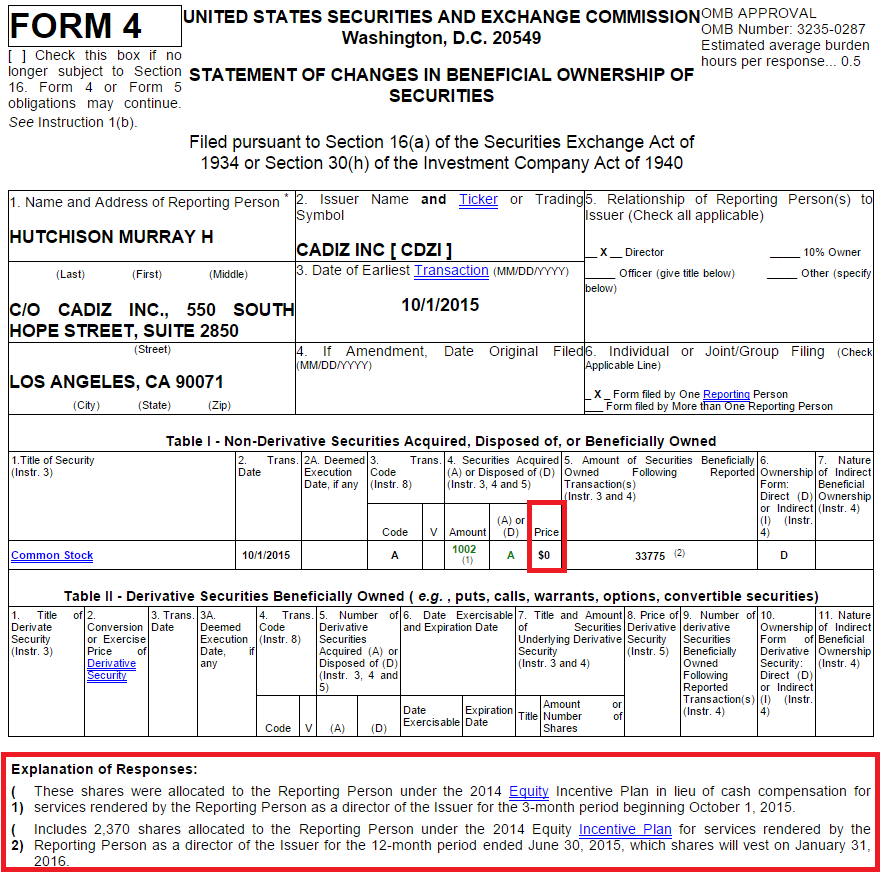

In addition to the interesting disclosure, the company filed two Form 4’s during the middle of the trading day and one at 4PM on that the day the letter was disclosed. These may or may not have helped steady the stock price. However, once investors dug into these Form 4’s, it was clear that only one – the one filed after 4PM EST – was an open market buy.

The other two Form 4’s looked like this one:

It also probably doesn’t help the cause that after the regulatory letter was issued, the CEO took to Twitter to call the regulators “dumb” and “stupid”.

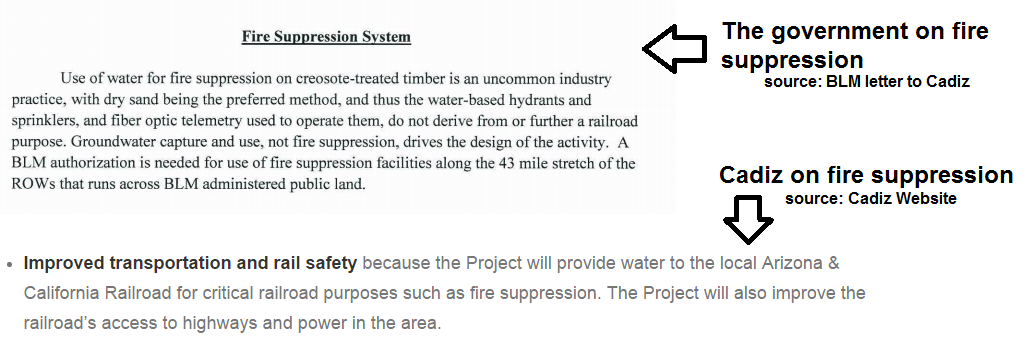

Among other reasons (the big one being that CDZI’s project doesn’t further a “railroad purpose” – kind of obvious), the government and the company seem to have big trouble seeing eye to eye when it comes to the science behind this project. CDZI’s science, not surprisingly, falls in their favor. For instance, look at the difference in opinion when it comes to the projects touted “fire suppression” benefits.

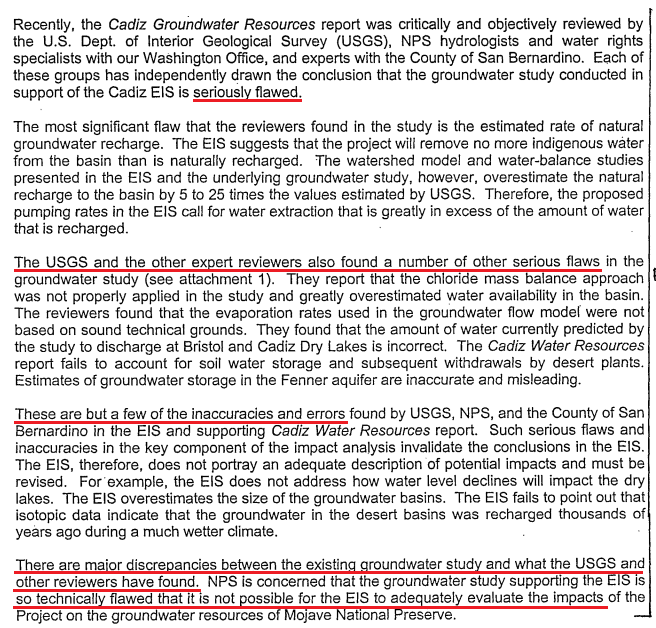

Lest we also not forget back in 2000, when geologists took a look at the data the company was using to try and further its project, a scathing report was issued to the company noting numerous flaws. We believe there is an extremely low chance that the company receives approval through a federal approval process. Government geologists don’t seem to be on the side of the company, and have repeatedly assessed that the company’s plan to use a desert aquifer as “seriously flawed”.

Here’s an excerpt from the brutal assessment that was issued to the company back in 2000.

You can find a link to the National Parks Service geological assessment here.

The project is seemingly so unviable, it’s bringing politicians together from across the aisle. This is from a 2013 LA Times article:

A Republican congressman who represents the northern Mojave Desert has asked the federal government to launch a full-fledged environmental review of Cadiz Inc.’s proposed groundwater pumping project.

The request by U.S. Rep. Paul Cook (R-Yucca Valley) joins a similar one made last year by Sen. Dianne Feinstein (D-Calif.), making a rare show of bipartisan unity on a publics lands issue.

The same Senator, Dianne Feinstein violently opposed the project in 2014 where she, “inserted a rider into a budget bill that bars the Department of the Interior from spending any money this fiscal year on reviewing the project for permits. ‘Severely drawing down the aquifer could damage that region of the Mojave Desert beyond repair,’ she wrote in an e-mail. ‘The bottom line is that right now we need more responsibility in how we use our water, not less,'” she said, according to a 2014 Bloomberg article.

A Massive Liquidity Concern, Major Risk for Shareholders

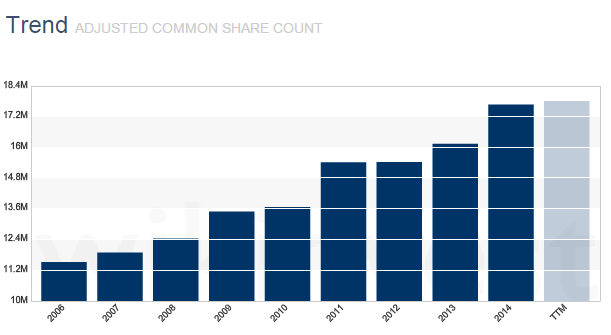

CDZI has, on the other hand, done some things well over the last few years: issuing shares, for instance. Here’s the company’s ballooning share count, up more than 50% since 2006. We expect this trend to continue further as the debt laden company has narrowing choices aside from issuing equity if they want to keep “operations” going.

The company’s cash flow tells the story of the coming dire need for cash. In the last 6 months, the company has burned $5.3 million in cash (silver lining: down from $6.5 million the year prior!). At this rate, the company is going to face some cash problems within a quarter or two and we expect further financing, should the Board allow this company to continue as is.

The company generates minimal revenue, and has survived over the last 10 to 15 years by taking on lower and lower quality debt while plundering the balance sheet, resulting in negative equity for shareholders. All the while, insiders have been paid handsomely and the company continues to bet its future on a project that does not seem viable.

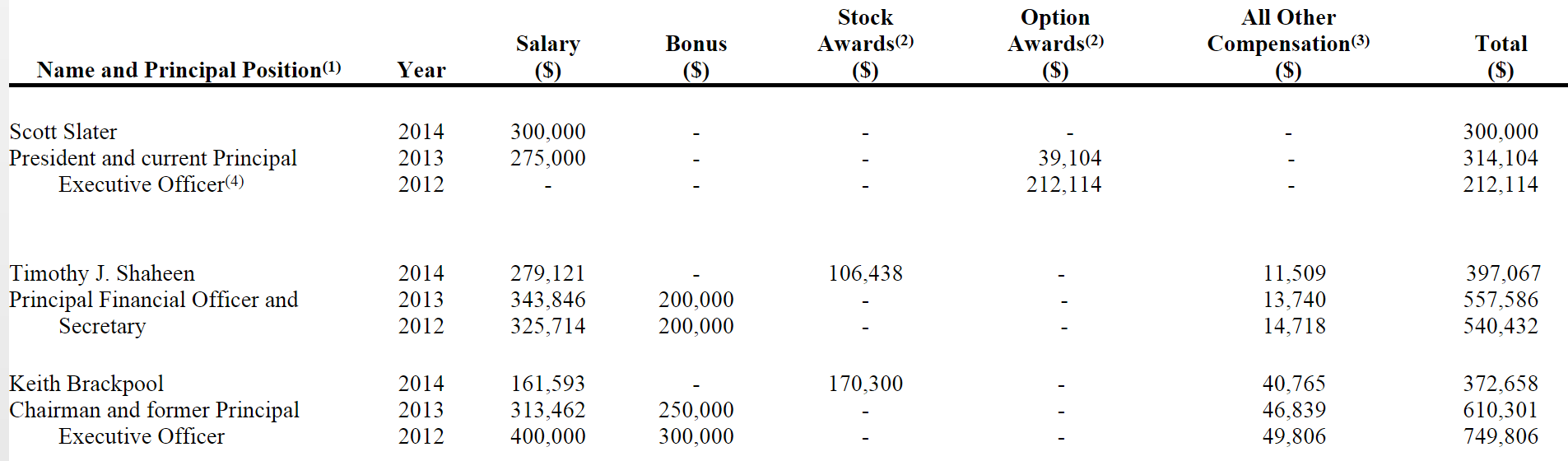

Here is what the Board is allowing company executives to take home in the last three years, from the most recent proxy. The CEO has netted more than $800K in three years, the CFO has netted well over $1 million, and the Chairman has taken home over $1.5 million:

After 42 straight quarters of not posting a profit.

In addition to this, when not flying on a private jet…

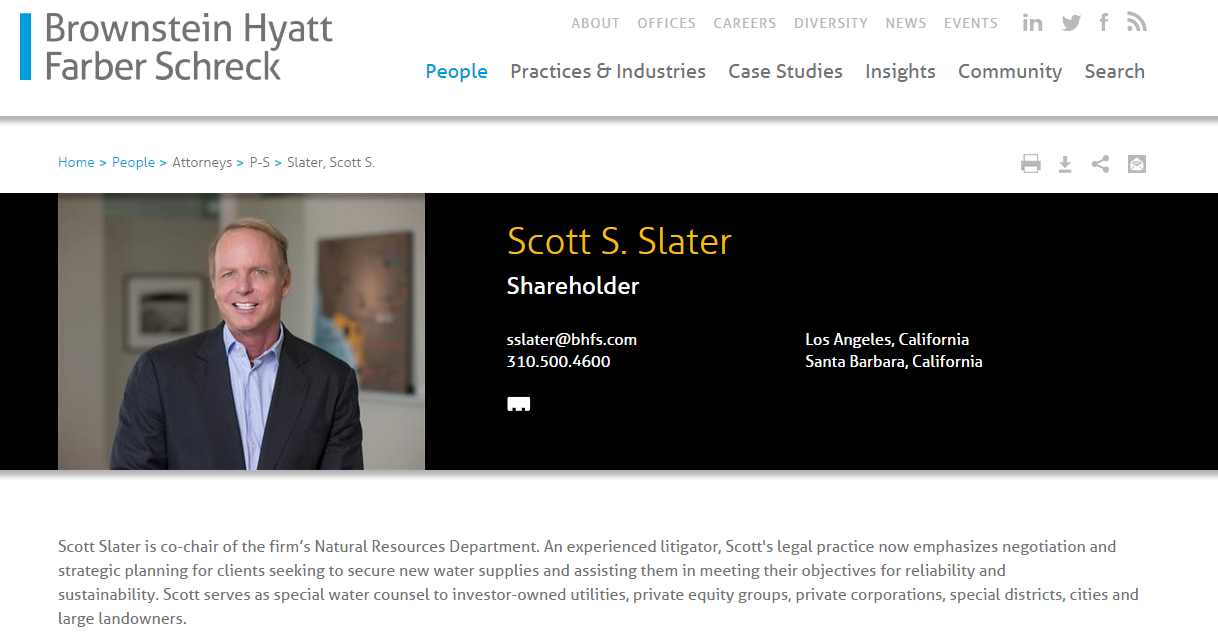

…the CEO also appears to be working as part of law firm Brownstein Hyatt Farber Schreck, where he is listed under “people” with the title “Shareholder” and listed alternately as “co-chair of the firm’s Natural Resources Department” and “special water counsel”.

It also appears that the law firm that Slater works at could be “feasting at the trough,” according to this article:

The owners of the land above this underground water supply, Cadiz Inc., have long hoped to drill large wells into the aquifer, suck out some of the water and pipe it to Southern California, where it could be steamed into a latte in a Malibu café or blasted through a car wash in downtown San Diego.

The project has the potential to make the company and its shareholders serious money, if they can make it happen.

Two hundred miles from Cadiz, in the San Diego suburb of Kearny Mesa, sits one public agency that has the power to bring this desert water west. The San Diego County Water Authority is charged with securing freshwater supplies for San Diego in the coming decades. It sets policy, makes deals and can generally tighten or loosen the spigot on the county’s water supply.

One of the Water Authority’s advisers is attorney Christine Frahm. A former chair of the authority’s board, Frahm has been heavily involved in local water policy for years, and currently works for the agency as an attorney and consultant.

While she’s been advising the Water Authority, and at least one other local public agency, Frahm’s firm has built a significant financial relationship with Cadiz Inc. Another shareholder at the firm where she works, Brownstein Hyatt Farber Schreck, Scott S. Slater, was named Cadiz’s CEO in February, and the firm recently signed a contract thatpromises it hundreds of thousands of shares in Cadiz as its project gets closer to completion.

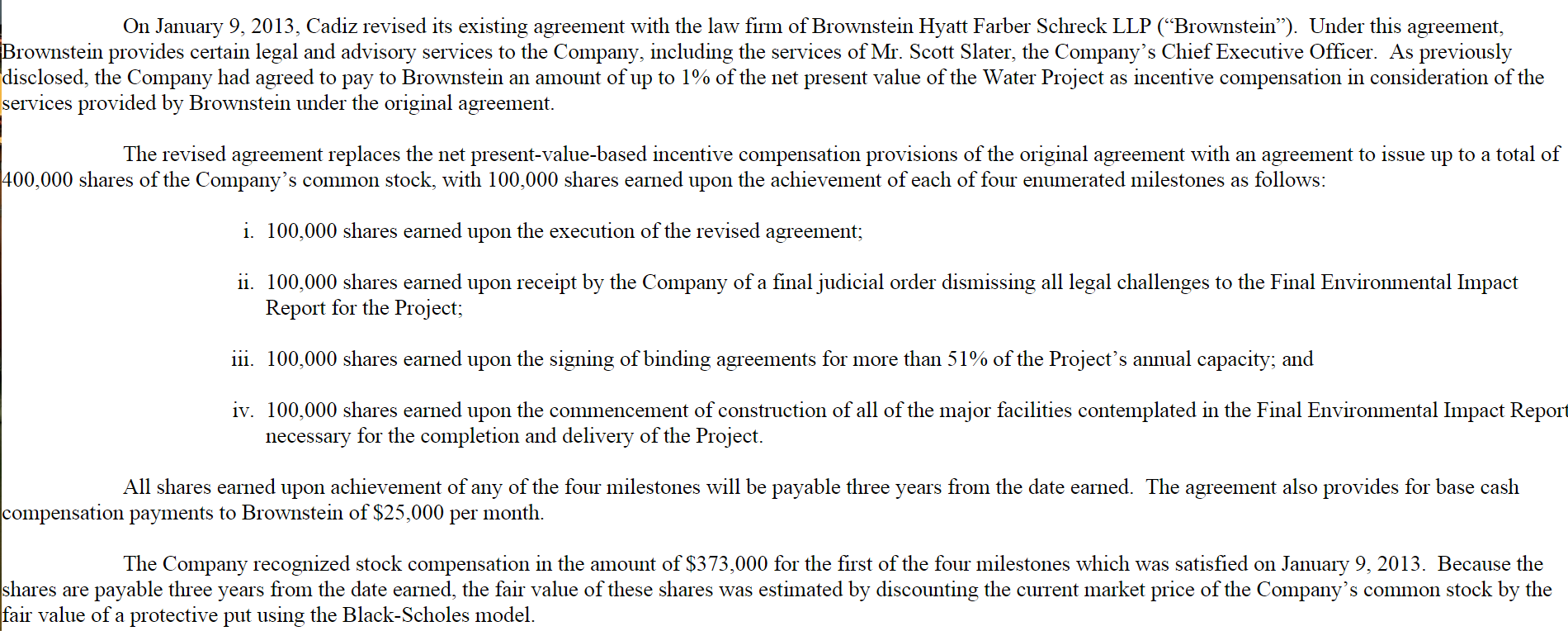

Take a look at an agreement from 2013 between CDZI and the firm Slater is “shareholder” of (link to full agreement here).

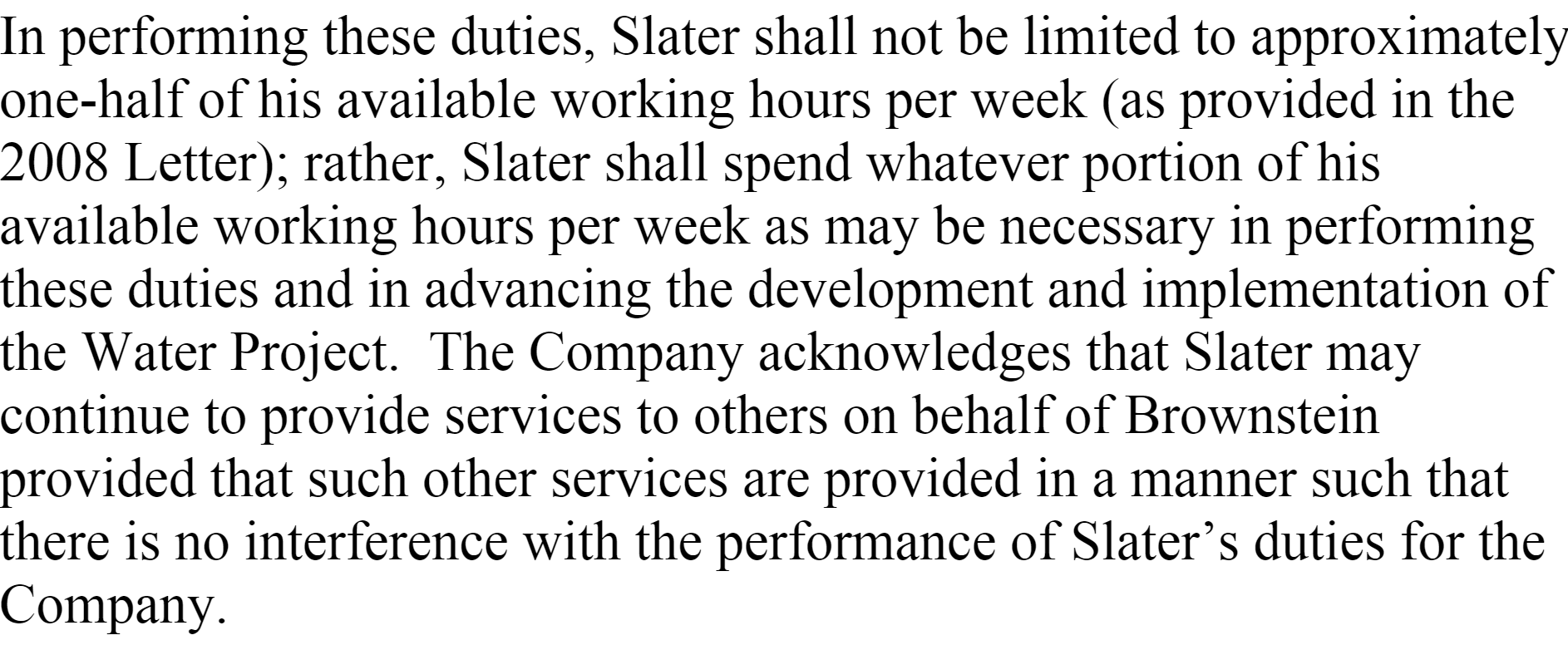

Here’s a line from the full agreement that states CDZI’s CEO can work for Brownstein in other matters:

In addition, according to this May 2015 S-3, it appears these “terms of engagement” still stand.

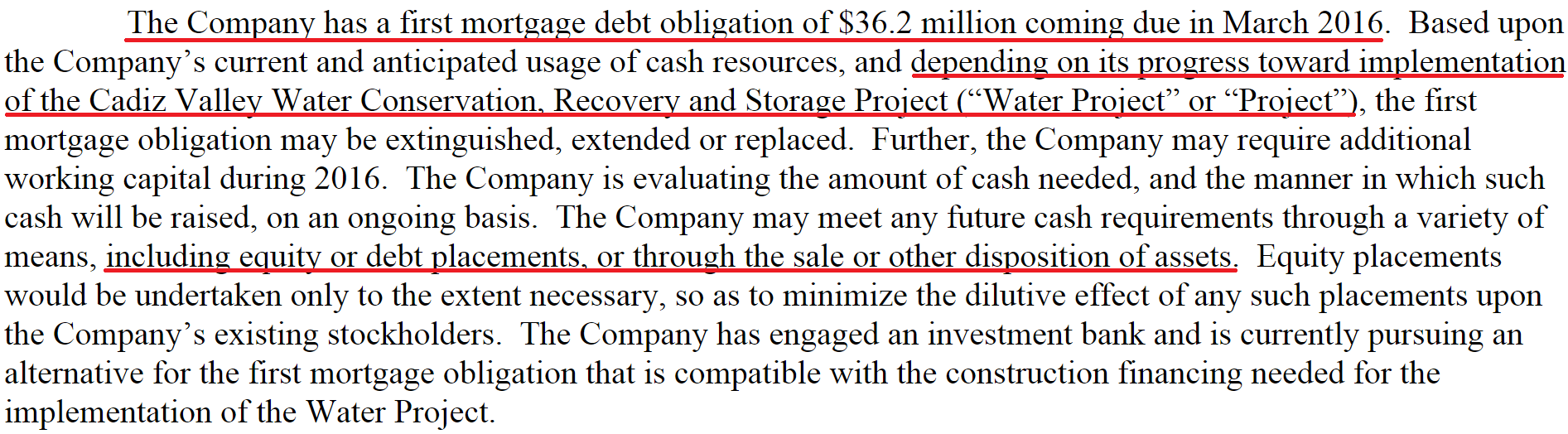

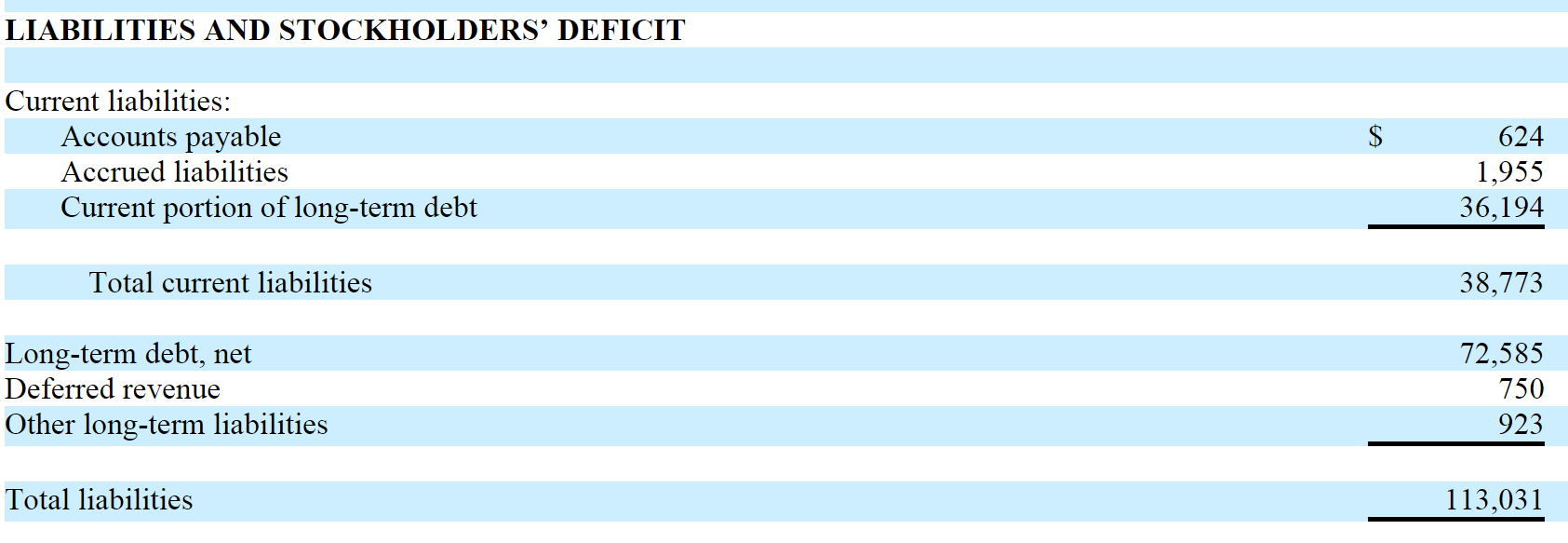

But it’s the liquidation section of Cadiz’s company’s filings that really tell the tale of just how distressed that company is. This section clearly states the company’s capital needs are only good until February of 2016, and that the company has $36.2 million in debt coming due in March of 2016. It also says its liquidity “depends on its progress toward implementation of [the water project].” This is the same project that appears to be in jeopardy of imminent failure.

The company continues by stating that it could default in March of 2016 due to this debt. (click to enlarge)

Here is a look at the company’s debt that’s current, and coming due – adding up, with other liabilities, to total liabilities of $113.03 million.

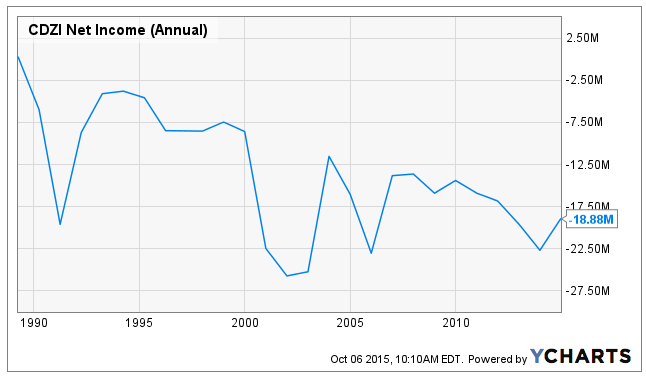

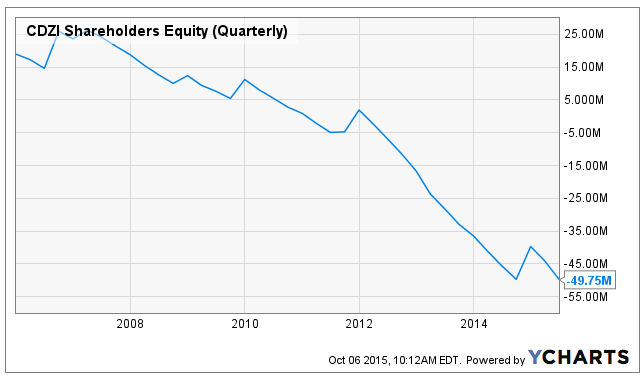

And here is a chart showing exactly how the company has plundered and incapacitated its balance sheet over the last 9 years.

We Value the Company at $0

It is not in GeoInvesting’s nature to be sensational. We don’t call companies frauds when they make “material misstatements” and we only assign price targets that we think are fair and worked out through real world valuation scenarios. It is rare that we assign $0 price targets to companies that are not simply outright frauds. CDZI is an exception to this rule.

Put simply, with an $80 million dollar market cap, we think the company is about $80 million overpriced.

We believe that shares are on their way to zero and the only question is when this will happen, and by what means. We can safely and fairly conclude that this company will eventually asymptote toward zero, whether it’s from toxic debt or plain old bankruptcy. While we cannot predict how long the company can issue shares and move forward to prolong their existence, what we can predict is that it is likely going to be detrimental to shareholders. As such, we are short CDZI.

Investors in this company need to consider several things. The first is that they need to consider that the company has an enormous amount of debt coming due in the beginning of 2016 that they cannot pay as they currently stand. Second, they need to consider that the company is burning about $10 million in cash per year which, without considering their debt, gives them roughly another 2 to 3 quarters to operate. Lastly, investors need to realize that there is no more room for give on the company’s balance sheet and that any financing moving forward is likely to be extremely toxic, resulting in the issuance of even more shares potentially coupled with warrants and other instruments that could further dilute the company.

We have already seen some of this take effect, as we have seen the company increase its share account significantly over the last 10 years.

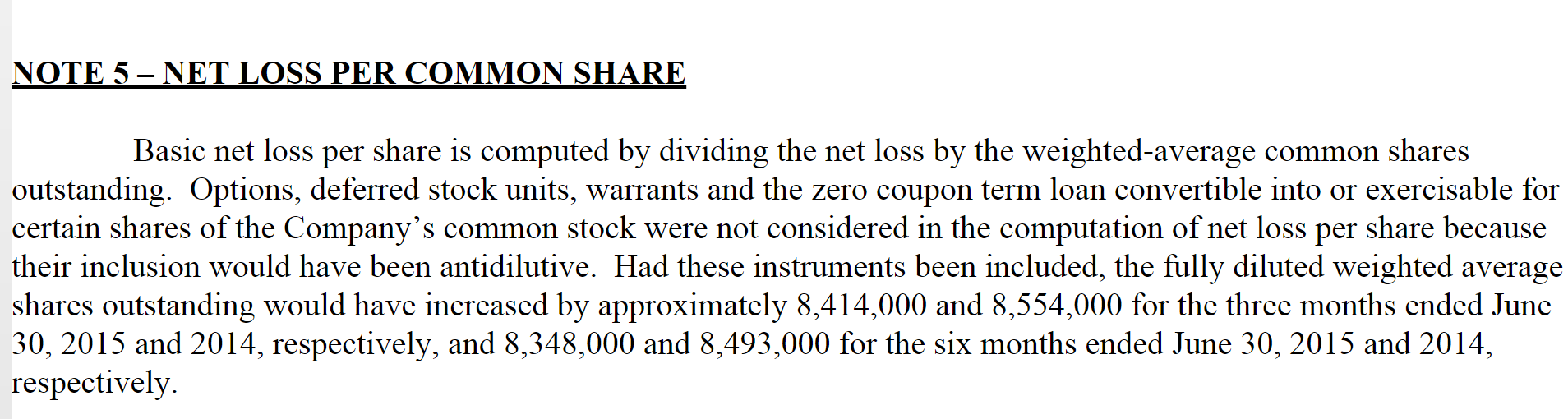

This note from the 10-Q gives us insight into the fully diluted share count, which is actually more than 26 million shares.

Taking into account the company’s fully diluted share account of about 26 million, an investor would note that the companies actually been assigned a market cap of almost $100 million, and that, again is $100 million too much.

With what we believe to be no viable projects in the pipeline, we think Cadiz’s equity is worthless.