On February 22, 2013 we published our first article on MKTG titled, “Responsys Inc. (MKTG): Filling the Valuation Gap” when the stock was trading at $7.76. Most recently, on May 6, we issued our follow up report “Responsys (MKTG) Last SaaS Standing” when the stock was trading at $10.80. Our bullish thesis was partly based on the valuation gap between MTKG multiples and other SaaS companies that were recently acquired. MKTG is now trading near $14.00. Comment streams related to our follow up article on Seeking Alpha brought Vocus Inc. (NASDAQ: VOCS) to our attention.

Vocus helps companies “enables businesses to attract, engage, and retain customers” through social media management, PR marketing (through the issuance of press releases), and email marketing (through the company’s iContact acquisition). The company offers its products on a stand-alone basis or as marketing suite (new product). We believe that the key to how enthusiastically investors embrace the VOCS story will be how well it develops its marketing suite since the growth of its legacy PR business may be played out and the margins of its marketing suite exceed the margins of its products that are sold on a stand-alone basis. While we are not overly excited over the acquisition of the lower margin iContact operation that occurred in February 2012, it gave VOCS the ability to quickly create a product offering unmatched by its competition. According to management:

“No other solution today brings together the essential components of digital marketing, including social search email and PR, together on an integrated platform that delivers rapid and measurable ROI across all of these channels.”

We couldn’t help but notice some of the similarities between MKTG and VOCS that may cause investors who follow the SaaS space to conclude that VOCS shares, at an Enterprise Value to Sales (EV/S) multiple of 1.4, are too cheap considering that they are selling at an appreciable discount to those of peer companies in an acquisition-hungry industry.

Cheap Based on Acquisition Activity

At its EV/S multiple, the company is priced well below the levels of companies that have recently been acquired:

| EV/Trailing Sales at Takeout Price | Date of Takeout | |

| Rightnow | 6.4 | Oct-11 |

| Successfactors | 9.9 | Dec-11 |

| Aprimo | 6.3 | Dec-10 |

| Unica | 4 | Aug-10 |

| Eloqua ELOQ1 | 8.2 | Dec-12 |

| Market Leader LEDR | 5.9 | May-13 |

| ExactTarget ET1 | 7.6 | Jun-13 |

| Mean | 6.8 | |

| Median | 6.4 | |

| Vocus VOCS(current) | 1.4 |

1Please note that ET and ELOQ (email and social media marketing) are the most akin to VOCS. But this list is only a fraction of the acquisition activity that has occurred in the SaaS universe.

- Oracle Corporation (NASDAQ:ORCL) – At least 18 SaaS acquisitions since 2010

- International Business Machines Corporation (NYSE:IBM)- 16 SaaS acquisitions since 2010

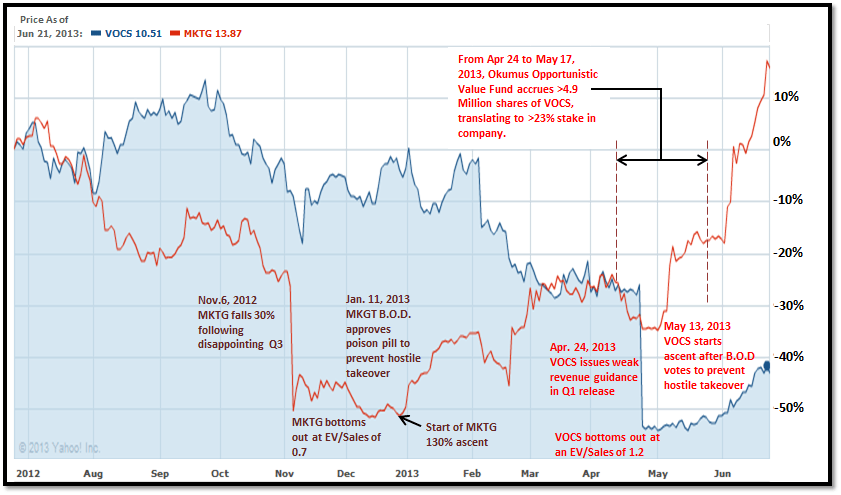

Additionally, the parallels that VOCS shares with MKTG (email and social media marketing, as well as being a similarly focused SaaS company) are eerily comparable. (See chart below)

- On November 6, 2012 MKTG shares fell 30% to $5.85 after it reported 2012 third quarter financial results where revenue growth was shy of analyst estimates.

- The stock bottomed out at an EV/Sales multiple of 0.7.

- In January 11, 2013 MKGT Board of Directors approved a poison pill to prevent a hostile takeover.

- Two reporting periods later (2012 fourth quarter and 2013 first quarter) MKTG is up nearly 150%, and reached a 52 week high of $14.42 on June, 26 2013.

It looks like analysts are finally willing to price MKTG at an EV/Sales multiple closer to the pre-acquisition EV/S multiples of its competitors, ET and ELOQ, which stood at around 5. On June 21, 2013 JMP Securities raised MKTG’s price target from $14.00 to $18.00 (via a Reuters headline) which equates to an EV/S multiple of 4.5. Recall, in our follow up MKTG article we assumed that the company should sell at an EV of around 5.

“It makes absolutely no sense that MKTG should sell at an EV/S multiple of 2. At the very least we believe it should trade at the average ELOQ and ET pre-acquisition EV/S multiple of around 5.”

We could not ignore the following similarities between MKTG and VOCS (See chart below):

- On April 24, 2013 VOCS shares plummeted 37% to $8.38 after it issued weaker than expected 2013 revenue guidance in its 2013 first quarter press release.

- The stock bottomed out at an EV/Sales multiple of 1.2.

- On May 13, 2103 VOCS Board of Directors approved a shareholder rights plan to prevent a hostile takeover.

“The rights plan is not intended to interfere with any proposals or offers that the Board of Directors determines to be in the best interests of all Vocus shareholders.”

Interestingly, the VOCS story contains an additional bullish catalyst to support an acquisition target thesis. A 13D filing on May 21, 2013 disclosed that an activist shareholder, Okumus Opportunistic Value Fund, Ltd.,(President, Ahmet H. Okumus) disclosed that it owns 4,926,304 shares of VOCS (a 23.35% stake). The related transactions regarding this ownership interest occurred from April 24, 2013 to May 17, 2013.

“The Reporting Persons (Okumus) believe that the Issuer’s financial performance can be improved to create greater value for the Issuer’s shareholders and accordingly, have had communication with the Issuer’s management with respect to the process of recommending two individuals to the Issuer’s board of directors. If the Reporting Persons ultimately decide to pursue such action, the Reporting Persons intend to work with the current board of directors to nominate two individuals as candidates for election to the Issuer’s board of directors. It is expected that the Reporting Persons will nominate one individual who is associated with the Reporting Persons, and one independent candidate. It is also anticipated that the Reporting Persons may, from time to time, have discussions with the board of directors and other shareholders of the Issuer with regard to the nomination process and subsequent election of directors.”

It remains to be seen if VOCS’ share price will see the similar substantial gains that MKTG experienced if and when investors realize that the market may have overreacted to noise that has little to do with the long term growth drivers of the company’s business. Applying a meager 3.5x EV/Sales suggests a value of nearly $30.00 a share, almost 200% above current levels. A multiple of 2.5-3.0 would lead to a price above $20.00.

Shares have already been quietly creeping back up from recent lows and now trade at around $10.25.

Let’s compare the charts of MKTG and VOCS:

In the end an acquisition suitor is not going to look at how is VOC S growing now, but instead it will assess how it will grow tomorrow.

Why VOCS Shares Sell at a Low EV/S Multiple

In April the stock dropped heavily (~40%) as a result of the company lowering its 2013 guidance from 20%+ bookings growth and 16% revenue growth to about 13% bookings growth and 10% revenue growth for the year. Above average rates of growth in the company’s traditional PR marketing business are decelerating in part due to the trend of companies to use other avenues of social/digital marketing. Furthermore, VOCS is focusing more of its resources to grow its new digital marketing suite; clearly the right move as evidenced by the many success stories of companies in this space (ET, ELOQ, MKTG to name a few). A minor negative short-term impact on revenue growth should be expected as the company grows its new marketing suite to a level where it can begin to have a bigger factor on overall company growth. But to punish VOCS as severely as the market has seems unwarranted for a company that has a solid history of growing its business. VOCS has grown revenues from in $20.4 in 2004 to $170 million in 2012.

The Growth Picture Could Improve

The company expects its new marketing suite product to grow 200-300% year-over-year (“YoY”) from $12 million in 2012 to the mid $30 million range this year. Company-wide growth could easily re-accelerate as the marketing suite becomes a larger part of VOCS’ overall business (which is expected to be around $35 million or about 20% of sales by year end and growing 200% YoY) and the macroeconomic environment in North America continues to improve.

Longer term, the company is looking to continue a shift from its legacy PR offering toward its marketing suite offering, which it believes is more lucrative. At the present time, marketing-related services account for less than half of sales, but grew at a 37% clip from the first half of 2012 to the second.

Ultimately, we believe that the ability of VOCS’s to grow its business at a rapid pace will depend on the market acceptance of its marketing suite by existing and new customers.

The following quote from the 2013 first quarter conference call illustrates that, so far, VOCS’s optimism for the outlook for the future of its marketing suite is not misplaced:

“At the beginning of the year, we were expecting to double bookings for the Marketing Suite in 2013.Looking forward, based on Q1 performance, strong macro demand for digital marketing and our expanded direct sales capacity, we now see our goal to double Marketing Suite subscriptions as too conservative. With this in mind, we’re expanding our marketing efforts behind the success of our Marketing Suite and now expect to triple the business in 2013, with bookings in the mid-$30 million range.”

Look Beyond the Obvious

SaaS company valuations are very dependent upon revenue growth performance. The sales growth of top-tier SaaS companies generally run in excess of 20%. The company has proven that it can grow sales in excess of 20% on a consistent basis.

| 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | |

| Rev | $20.4 | $28.1 | $40.3 | $58.1 | $77.5 | $84.6 | $96.8 | $114.9 | $170.8 |

| YoY Growth Rate | 37.7% | 43.4% | 44.2% | 33.4% | 9.2% | 14.4% | 18.7% | 48.7% |

Thus, investors who focus on VOCS’s current 2013 guidance which is hindered by the moderation of growth rates of its legacy business will not view the company as a tier one candidate. Those that look at VOCS’ entire business plan, with an assumption that management will execute its new digital marketing strategy and that sales growth will eventually accelerate will view VOCS as a bargain at current prices and a potential acquisition candidate. This could be why Ahmet H. Okumus acquired 4,926,304 shares of VOCS (23.35% stake).

Also consider that tier one SaaS plays often carry gross margins (GM) of at least 70% and experience high renewal rates. Vocus is a SaaS business with 84% GM’s and 80-85% renewal rates for its products.

Essentially, based on the current revenue outlook VOCS looks like a tier two company on the surface, but in actuality it is a tier one once the layers of its growth drivers are analyzed.

Valuation

Worst case scenario

Investors who hold a pessimistic view towards VOCS’s product offering other than its marketing suite can find solace in knowing that upside to VOCS’ current share price still exist in such a scenario.

VOCS’ digital marketing revenues are growing at torrid pace and should be valued at a minimum EV/S multiple of 5.

Overly conservative investors can place an EV/S multiple of 1 on VOCS standalone legacy businesses. Based on 2013 revenue guidance this analysis would value the entire business at around $12.01.

But this scenario is misplaced. It fails to take into account that

- the legacy businesses has customer retention rates of around 80%

- legacy businesses generate cash to help VOCS develop its marketing suite

- VOCS is replacing legacy revenue with higher margin revenue.

Keep in mind that the marketing suite revenues would probably be valued at around an EV/S of 8 if the company was acquired. In this case, VOCS’s entire operation would be worth $17.00 (only assuming an EV/S of 1 on the legacy businesses and its email marketing product).

Significant Upside Exists

The long term model is for 25-30% operating margins and 20% free cash flow (“FCF”) margins, which seem reasonable given that VOCS is an 84% GM business and expect GM’s to rise slightly over time (targeting 90%). This is in line with other high margin SaaS companies. It also boasted 25% FCF margins in 2008 while still meaningfully growing its top line. Prior FCF margin guidance was 25-30%, but this number has been lowered to 20% after the iContact acquisition.

If we take the long-term FCF guidance on the current sales numbers, VOCS would be trading at 5.3x normalized FCF (20% FCF margins). Checking against a wide variety of comps (ADBE, ET, ELOQ, CRM, N, ORCL, IBM) and comparing FCF multiples, VOCS has the lowest. Only Oracle and IBM come close (around 9-10x), but those companies already have $100B+ market caps and much lower growth prospects.

Historical stock price trends show that, from a multiples and comps perspective, there is huge upside to the company’s shares. It is easy for SaaS companies to trade at 3-5x sales; in fact VOCS was there as recently as last September. However, it is rare to see a SaaS business trading for as low a multiple as VOCS (less than 2x sales) when it still has reasonable growth prospects. Considering the imminent growth of VOCS’ marketing suite and the favorable tailwinds surrounding its business, 3-4x sales seems fair for this business — this implies a huge upside. Taking the midpoint at 3.5x, this would suggest a value of nearly $30.00 a share, almost 200% above current levels. Even under a more conservative set of assumptions there appears to be a large margin of safety at the current quote of $10.22. At 2.5-3x sales, or 12x normalized FCF (both of which are well within VOCS’ historical ranges), this translates to a price above $20.00.

There is a good chance that if the company put itself up for sale it could garner a high price. This scenario may end up playing out as Okumus has a history of taking large stakes in out of favor companies and demanding change.

3.1x sales would imply almost a triple from today’s prices for the entire Vocus business. The firm’s relatively small market cap ($215 million) and well developed and integrated product offerings mean that it could be a compelling acquisition target for a larger firm looking to gain a foothold in the less-than-1000 employee market. There has been recent M&A activity in the space as well; Salesforce.com, one of the largest players, recently bought ExactTarget for about $2.5 billion in cash, translating to a multiple of 7.6x ExactTarget’s sales! If Vocus were to be purchased anywhere near that number, it would be an instant multi-bagger.

This situation provides an investor with a degree of security on the purchase. If the company got taken out it would likely be at a much higher price, but even if it didn’t the investor would be left with a high quality business with strong growth prospects trading at a significant discount to historical levels; hardly a bad situation.

Strong Industry Tailwinds

Strong growth should be spurred by favorable industry tailwinds, which have made digital marketing one of the most attractive opportunities in software today. Today, 88% of consumers use the internet to research products. Of all the search results they pull up, 70% of the links are organic, underscoring the critical importance of SEO. In contrast to traditional forms of advertising, like Yellow Pages and newspapers that have experienced declines of around 50% in the past 6-7 years, digital marketing is expected to grow at an annual rate of 17% until 2016, which represents a doubling from levels seen as recently as early 2012.

Within this industry, VOCS focuses its sales efforts on small and mid-size businesses that have between 2-999 employees. This is a lucrative opportunity and still relatively underserved; running the math on it, with $1 million mid-size firms at an average selling price (ASP) of $7,000 and 5 million small firms that have an ASP of about $3,000, the total addressable market for Vocus could be as large as around $22 billion. Furthermore, the company’s focus on these smaller companies prevents it from having to compete with larger, better-capitalized firms like CRM and IBM and enhances its competitive positioning. At the moment, VOCS derives about 60% of its sales from mid-size businesses, but management believes it will be able to expand its share among the smaller businesses (2-9 employees) in a cost-effective manner.

Other Factors to Consider

VOCS sells a sticky product. The business itself is very attractive: asset light, subscription based, with a limited need for capex. The company is able to recoup its investment on a customer within 7-8 months, with lifetime profitability approaching 70% (calculated as lifetime contribution / lifetime sales). The firm’s sales model is attractive as well, with representative additions being accretive to cash flow within a year (more detail provided later).

The company has a balanced mix of subscription types, with choices including annual, monthly, and transactional (all are prepaid). Several customers have claimed at various investor conferences that the ROI’s that they have seen are in the range of several hundred percent. Based on renewal rates, customers seem very dedicated and happy with products, as VOCS’ integrated offering provides efficient management of the wide variety of online marketing strategies that are available in today’s environment. This satisfaction has created consistent sales growth, with top line growth in each of the last thirteen years.

Per the 2013 first quarter conference call, here is an example of the success a global clothing retail brand has experienced after using VOCS marketing suite.

“The results speak for themselves. And — since implementing Vocus, their online retail sales have increased by 300%. They are now found on the first page of Google search and they’re able to implement big company digital marketing with a marketing staff of only 5 people.”

VOCS sells its products through a commission model, meaning its wage expenses will only increase if sales increase as well. In 2012, it nearly doubled its sales force of 270 to 500. VOCS generates very predictable returns on its sales team members, with cash flow being breakeven after 7 months and GAAP being breakeven over 18 months. This is likely a large reason why the company has been consistent in hitting its guidance; the company made sales and cash flow guidance in 2007-2011, except for a revenue miss in 2009. Management frequently mentions the importance of a large sales force to the company’s success, believing that broad distribution is the best way to reach the total addressable market (“TAM”).

One of the biggest keys to Vocus’s future growth will be its success in shifting customers from monthly and transaction-based subscriptions to annual ones. At the present time, nearly 90% of the company’s customers utilize these monthly or transactional models, meaning only a small sliver have annual subscriptions. However, that small group accounts for nearly 66% of revenue! This implies that even a small shift in the customer-mix toward the annual package could provide huge sales upsides. It would be interesting to hear management’s plan to stimulate this; at the moment, it appears that the company is hoping its customers will naturally choose the longer subscription once they realize how useful and cost effective the product is for them when compared to other services offering the same end results.

In a similar manner to its subscription mix goals, VOCS is looking to get customers to shift from stand-alone products to product suites, which are higher margin and better revenue generators. At the moment, about 40% of sales still come from these stand-alone offerings, so there remains a substantial opportunity to sway customers toward the suites and further boost GM’s and sales.

Conclusion

It remains to be seen if Vocus will turn its ship around and, at the same time, successfully integrate the iContact acquisition into its business model. There is also some risk that its legacy businesses deteriorates faster than expected. However, it is tough to ignore the favorable industry trend and business metrics that increase the company’s chance for mid to long-term success. The risk/reward ratio profile of investing in VOCS is very compelling. If the company succeeds in all aspects of its business plan, shares could triple. Even if the new marketing suite is the only aspect of the company that investors choose to assign a premium value on, a worst case scenario, they still make money with their investments. Furthermore, the low hanging fruit provided by acquisition trends makes VOCS a healthy speculative addition to your portfolio.

Disclosure: Long VOCS, MKTG

Disclaimer:

You agree that you shall not republish or redistribute in any medium any information on the GeoInvesting website without our express written authorization. You acknowledge that GeoInvesting is not registered as an exchange, broker-dealer or investment advisor under any federal or state securities laws, and that GeoInvesting has not provided you with any individualized investment advice or information. Nothing in the website should be construed to be an offer or sale of any security. You should consult your financial advisor before making any investment decision or engaging in any securities transaction as investing in any securities mentioned in the website may or may not be suitable to you or for your particular circumstances. GeoInvesting, its affiliates, and the third party information providers providing content to the website may hold short positions, long positions or options in securities mentioned in the website and related documents and otherwise may effect purchase or sale transactions in such securities.

GeoInvesting, its affiliates, and the information providers make no warranties, express or implied, as to the accuracy, adequacy or completeness of any of the information contained in the website. All such materials are provided to you on an ‘as is’ basis, without any warranties as to merchantability or fitness neither for a particular purpose or use nor with respect to the results which may be obtained from the use of such materials. GeoInvesting, its affiliates, and the information providers shall have no responsibility or liability for any errors or omissions nor shall they be liable for any damages, whether direct or indirect, special or consequential even if they have been advised of the possibility of such damages. In no event shall the liability of GeoInvesting, any of its affiliates, or the information providers pursuant to any cause of action, whether in contract, tort, or otherwise exceed the fee paid by you for access to such materials in the month in which such cause of action is alleged to have arisen. Furthermore, GeoInvesting shall have no responsibility or liability for delays or failures due to circumstances beyond its control