We recently wrote an in depth research piece on Rand Worldwide Inc (OOTC:RWWI) supporting our long disclosure in the stock. It was one of our more near-term picks that we published to our pro portal to help our members learn more about the reasons why we like RWWI. If you’re already a member and need a refresher, sign in and go here to see where RWWI was when we wrote our RFT (Reasons For Tracking) on the company.

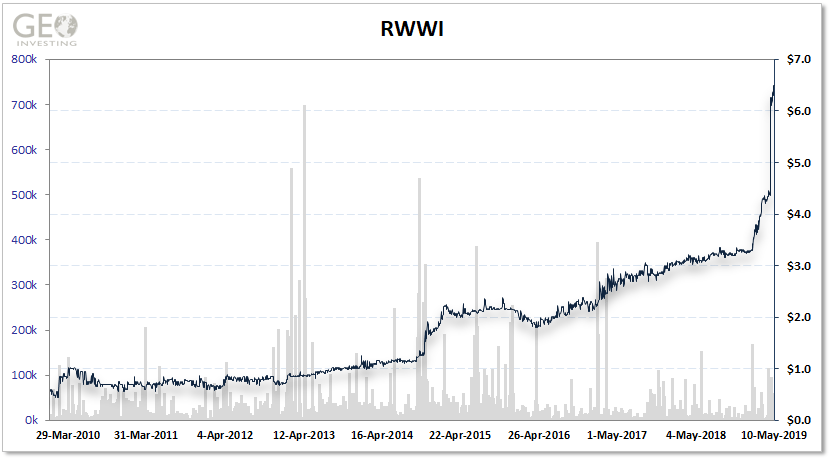

RWWI’s chart is one you probably wouldn’t mind seeing for every stock in your portfolio.

$5,000 invested in the stock in December 2010 at $0.53 (the average of the high and low for the month) would now be worth $61,320, which equates to a compounded annual return of around 36.8%. And we think this performance will continue.

Our bullish thesis is based on 5 factors

- RWWI easily debunks negative microcap stereotypes

- Recurring revenue aspect to RWWI’s business model

- Strong relationship with Autodesk

- RWWI could be an ideal acquisition candidate

- Operating leverage

We took an in-depth look at each one of these factors for our premium members.

Here is a passage from the article that we love because it debunks negative stereotypes labeled by the financial media that all microcaps are microCraps.

1. RWWI is a Beautiful Example of Debunking OTC Microcap Stereotypes

You are probably aware of many of the negative stereotypes surrounding microcaps, including the assumption that they are all pump and dumps or development stage companies with barely any revenue. RWWI proves those stereotypes wrong:

- It has been around for over 20 years

- It is one of the largest resellers of Autodesk products

- It employs over 400 people in almost 50 locations across North America

- It has served over 25,000 customers

- It has an extensive sales database that contains several hundred thousand point-of-contact names collected over its history

RWWI’s going public history began in October 1996 when, with about $9.5 million in revenue, Spatial Technology completed its initial public on the American Stock Exchange under the symbol SIY (prospectus not available online). SIY was a:

“…leading developer of three dimensional proprietary modeling software. The Company licenses its 3D modeling software to software developers, enabling them to incorporate advanced 3D modeling functionality into their applications. The Company’s 3D modeling software is designed as an open, component-based software technology that is compatible with a variety of platforms. The Company’s ACIS 3D modeling software products provide core 3D modeling capability for numerous commercial CAD software applications. In addition, the Company’s 3D modeling software is licensed by leading universities and research institutions.”In November 2000, SIY sold its proprietary modeling software business for $25 million to Dassault Systems in order to focus on its new PlanetCAD software reseller online platform that allowed manufacturing and design engineers to access and apply third party software to their needs. The stock symbol was changed to PCD. Then, in 2002, PCD completed a merger with software company Avatech to strengthen its Autodesk relationship and product offering breadth.

“This merger will allow us to continue our solid commitment to Autodesk, Inc. (NASDAQ:ADSK) by strengthening the R & D efforts including an Autodesk platform-based product.”

The name of the company was changed to Avatech Solutions, and it was listed under the symbol AVSO. Finally, in 2010, Rand Worldwide completed a reverse merger with AVSO:

“With little geographic overlap between the businesses today, the combination of Rand Worldwide and Avatech allows us to leverage the full range of selling and technical resources of each of the companies to enhance the service delivered to our clients,” commented Dulude. “We believe that clients in all of the geographies we serve will reap the benefits of the very deep bench of technical service capabilities that will result from combining the two companies. Also, the ability to deliver the additional products and solutions that each company has to its respective customer bases represents an attractive cross selling opportunity.”

Steve Blum, Autodesk’s senior vice president of Americas Sales said, “Autodesk has been very pleased with the performance of these two significant channel partners and we look forward to the increased capabilities available with this combination.” All Autodesk related services and sales activities for the two companies will be combined under the IMAGINiT Technologies brand worldwide (IMAGINiT, purchased by Rand in 2000, is the largest North American value-added reseller of pre-packaged software product offerings developed by Autodesk).

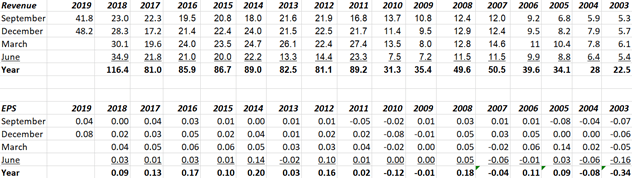

The new company is named Rand Worldwide, trading under the symbol RWWI. Throughout its history, the company has grown considerably, generating substantial revenue, while generally maintaining profitability:

Its revenue growth performance has certainly been lumpy and has hit periods of little, or no, growth. This has also been the case for the company’s EPS performance. With software companies, however, I am more interested in revenue growth and the level of recurring revenue.

The jump in 2011 revenue was due to an acquisition (merger), but it then flattened out until 2018 and 2019, due to four acquisitions made dating back to 2016. Without the luxury of SEC filings since 2015, it is going to be hard to determine what type of organic growth the company has been experiencing. However, we believe that recurring revenue, recent industry trends and an increased pursuit of M&A could be setting up RWWI for new elevated base-level EPS, and possibly a period of accelerated growth.

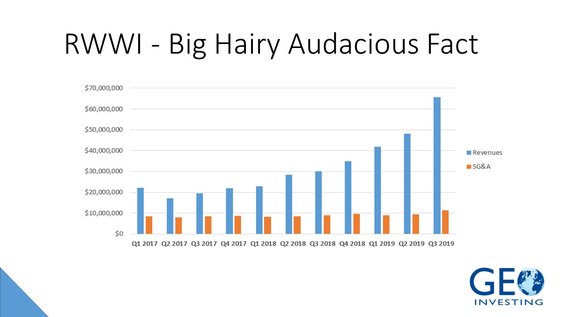

On Inflection Points

Operating leverage in a business occurs when Sales, General & Administrative (SG&A) and marketing expenses grow at a slower rate than revenue. This allows earnings to accelerate at a much faster Pace than Revenue.

There is one slide in the above-referenced article that really captures the essence of this, which is why we think RWWI has reached a transformative inflection point.

What is a Big Hairy Audacious Fact?

…well, a take on Jim Collins’ Big Hairy Audacious Goal…

So remember, the size of the market cap does not determine the size of the revenue. It is possible to find many companies with substantial revenue that sell at a marketcaps of less than $300 million, the definition of a microcap. For example a building supplier, Bluelinx Holdings Inc. (NYSE:BXC), has a marketcap of $230 million, but has revenue of over $1 billion. In fact, there are companies with less than $50 million market caps, known as nanocaps, with large revenue and earnings.

If you’d like to learn more about all the reasons that we like RWWI and why we still think it has significant potential, please consider joining our platform, which we think you will agree is different than any other microcap platform out there providing organic research. We have a proficient team of experts and a history of uncovering fraud and deception, which is why our members have grown to respect our long research. Where there’s caveats, we find them. Where there’s opportunity, we pounce.