We have a saying around the Geoinvesting office when we lose money on an investment as the result of missing an important piece of due diligence.

“You just got YUII’ied!”

You will understand what I mean if you keep reading, including the video that says it all at the end of the article.

Easy Like Sunday Morning

Maybe you can relate to this Sunday morning spring scenario.

You wake up to a beautiful spring sunny landscape, hearing birds chirping and smelling flowers blooming, thankful this is not just a dream. Soon, you get after whatever it is you do in the morning, maybe a cup of coffee, maybe some weightlifting, or maybe a jog. Heck, maybe you just go back to bed for a while! But one thing’s for sure, you’re looking forward to spending this Sunday relaxing, getting ready for the week’s grind.

You’re also looking forward to assembling that stand-up desk that arrived during the week. It looks simple enough to assemble, and you are like “screw it”, I don’t need any “dayam instructions”, so you put them aside.

I think you know where I’m going with this. More often than not, unless we have MacGyver skills…

…many of us are probably going to screw it up. You might end up dissembling the desk back to the point where you made a mistake and start reassembling it, this time using the instructions. Now you’ve essentially doubled the time it took to put it together.

Or maybe you’re just lazy and conclude that your patchwork functions just fine, and you even smugly think it’s close enough to perfect. Then, one day you’re standing up at your wonderful desk when it falls apart. A large wooden slab slides down to the floor, injuring your toe, and your pride. You begrudgingly realize you can’t return the desk because you broke it, and finally admit that you should have read the directions from the get go, instead of wasting money, time and saving that trip to the ER!

I don’t think this is what Lionel Richie envisioned when he was writing “Easy Like Sunday Morning” in 1977 while he was part of the Commodores.

Read The “Dayam” Risk Factors!

The investment process is already hard and much like putting that desk together. If you don’t do it right, your process just falls apart and fails to yield the knowledge needed to keep that slab in place. You need to navigate through thousands of stocks and mountains of press releases to decipher which management teams are straight shooters who hold things together and which ones are just straight up bullshitters that destroy the foundations and integrity of a company. If you’re not reading risk factors in 10K SEC filings of stocks on your watchlists, you’re making the investment process a whole lot harder and opening yourself up to a slew of completely avoidable mistakes.

Risk factors are the fine print in your investment instruction manual that too many investors ignore.

The fact that SEC filings present themselves as piles of boring pages of boiler plate language is no reason to ignore them. Once you figure how to read SEC filings and where to look for information, the process is quite easy and actually fun, much like that disciplined routine you exercised of doing math problems – you know, that one that yielded those coveted A’s in calculus. There is so much good information you can use in SEC filings to help you manage the risk of your portfolio by selling or avoiding certain stocks, and maybe even profiting by shorting them. Strive for those A’s.

When you don’t read risk factors, you only have yourself to blame when a seemingly boilerplate risk factor comes true or better yet, when a stone-cold unusual non-boilerplate risk was staring you right in the face.

Nothing drives this point home better than the case study of Yuhe Int`l Inc (GREY:YUII), a stock we were both long and short during different stretches of time at GeoInvesting.

Chicken Farms

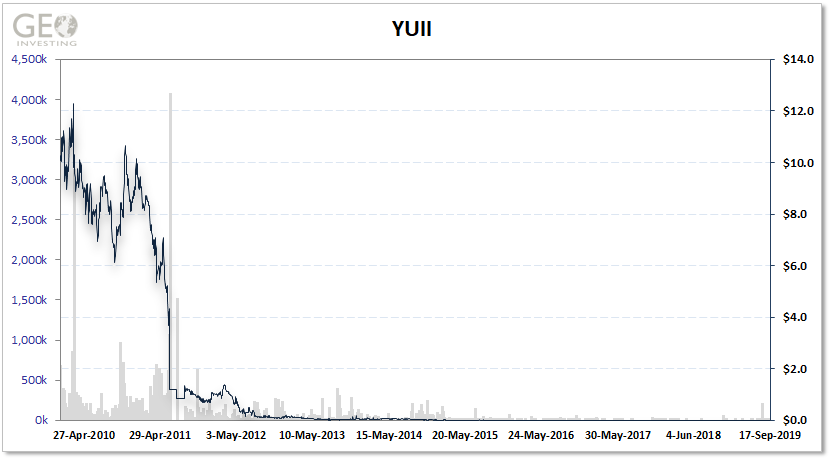

Yuhe International was a China based company that went public in the U.S. through a reverse merger in March 2008. YUII had claimed to be the largest supplier of day-old chickens in China. The company eventually graduated from the OTC to the NASDAQ in April 2008. This is probably all you have to know to understand how badly this story is going to end.

Ok, I’ll alleviate the suspense. On June 17, 2011, YUII’s stock was halted and eventually got delisted from the NASDAQ on July 12, 2011 as a direct result of research we published on June 13, 2011 that was based on our on-the-ground due diligence we had performed in China.

In its case against YUII, the SEC summarized the fraud:

“This case concerns false public statements made by Yuhe, a China-based company under Gao’s direction and control whose stock, during the relevant time, traded in the United States on the NASDAQ. Between approximately December 2009 and June 2011, Yuhe misled its public investors by disseminating a series of materially false statements concerning a purported acquisition for more than $15 million.

In truth, the acquisition never occurred, and Gao used his power as CEO to divert more than $12 million that purportedly was used for the acquisition to a private account he controlled.”

Between 2009 and 2014, GeoInvesting uncovered and reported on 12 fraudulent US based China companies trading in U.S. (which were eventually delisted), as well as 22 U.S. domiciled pump and dumps. You can learn more about how we stumbled upon the pattern fraud that that was exported to US exchanges through U.S. Listed China-based companies.

At one time, we had high hopes for YUII. Specifically, financial information in SAIC filings looked encouraging. To our surprise, in the most recently available filings we examined, a good chunk of the financials portrayed in the SAIC financials were similar to the numbers in YUII’s SEC filings. So much so, that our lead investigator gave me the green light to buy the stock. The stock was trading around $3.00 at this time, but had previously traded as high as $12.28 in March of 2010. I nibbled, gingerly.

For those of you who might be unfamiliar with what SAIC filings are, these are filings that companies and their subsidiaries doing business in China must file at the provincial level where the business and subsidiaries are located. Only revenue generated in China has to be recorded.

Upon closer inspection to the SAIC filings, we noticed that in the most recent year we inspected, the SAIC financials started diverging from SEC filings. But we didn’t want to draw any conclusions. So, we sent our China team hunting for the truth.

When we eventually sent one of our investigators to the province in China where YUII’s farms were located, we continued to have high hopes that the company might be somewhat legit. We had actually located some of YUII’s farms and it looked like business as usual. Could we have finally found a microcap U.S Listed China-based stock that was worth our investment?

Our Hopes Were Dashed

We eventually got a call from one of our investigators, where he said we had a fraud on our hands. He had hailed a taxi to go visit one of YUII’s chicken farms. In an incredible stroke of luck, in a country with over 1.3 billion people, the taxi driver happened to know of the business that YUII claimed to have acquired for $15 million dollars, with proceeds from $29 million it had raised in 2010. At some point during the ride, the topic of the acquisition came up. The driver told our investigator that YUII is full of shit. He never sold the company to anyone. The rest is history.

We ended up actually having a conversation with the alleged acquiree and recorded the conversation where he revealed that he never sold his business to YUII. There was a back-and-forth period where YUII kept denying our allegations, prompting us to make more calls to the acquiree that we also recorded. It got to the point where the acquiree actually commented that YUII was facing bankruptcy and that YUII’s founder actually asked the him to go along with the “plan” so they could both pocket the money Chairman Gao had stolen.

By the time NASDAQ finally halted YUII, pre-market on June 17, shares were trading at a little over $1, down from the ~$4.00 the stock was at when we first published our exposé.

Personally, I couldn’t believe that the exchange waited so long to halt the stock. I get it, it’s our word against YUII’s regarding the acquisition. However, no one seemed to care about what I believed to be our “drop the mic” evidence that we uncovered. Between our publication date and the halt date, investors continued their complacency and even outright denial. Feedback like this regarding the YUII case pervaded message boards across the internet:

…Thanks, Geo, for dragging your feet on whatever information–presumably nothing–you’ve waited months to reveal.

…You waited too long and then printed something completely irrelevant.

…I think the China fraud play is pretty much dead. YUII was a nice catch and good work. But that didn’t buy you the credibility you needed to clean up this space, and your own foot-dragging certainly didn’t help.

…Good luck to all. Hopefully my many China long positions will be able to shake off Geo and the other shorts.

Of course, this individual was proven to be dead wrong about the “China fraud play” in the years to come. (see China Hustle). As to dragging our feet, sometimes that’s what it takes to build a complete picture of fraud and an entire case against companies seriously and materially misrepresenting the truth.

This is illustrated well with what happened during one of our final edits of the research report.

I decided to take one last look at YUII’s SEC filings and pay closer attention to the company’s risk factors. And bang, I could not believe what I came across. I had never seen anything like this risk factor that explained that personal bank accounts of employees that were used to transact business.

“The Company uses company-controlled personal bank accounts of certain of its employees for transit purposes to transact a substantial amount of its business and the Company transacts a significant amount of its business in cash without using bank accounts.”

YUII’s auditors at the time, Child, Van Wagoner & Bradshaw, PLLC, even seemed to have signed off on this disclosure and the “it’s just normal course of business in China” excuse YUII gave for it in the filing!

Nothing to see here…

Obviously, this confirms our suspicions that we can’t assume that auditors will always do their homework, choosing instead to hide behind their disclosures. I guess they might night not believe reading ALL risk factors is important!

Now, everything started to make sense. We already knew that YUII lied about making their acquisition and had concluded that Chairman Gao had instead used ACH transfers to deposit millions of dollars to his personal bank account.

We had also pointed out numerous other risks disclosed or gleaned from SEC filings:

- YUII’s 2010 Form 10-K filing disclosed, “The Company uses company-controlled personal bank accounts of certain of its employees for transit purposes to transact a substantial amount of its business and the Company transacts a significant amount of its business in cash without using bank accounts.”

- YUII reports $42 million cash as of QI 2011, yet continues to take out short-term loans for “liquidity needs”.

- Despite having $42 million in cash, the company’s 2010 Form 10K reports being delinquent on “employee benefit payments” of around $600,000 at December 31, 2010. Given the company reports having $42 million why wouldn’t they just pay the benefits liability with existing cash?

- The company reported in its Form 10-K filings less than $1,000 of AR for the years ended December 31, 2008 and 2009, and no AR for the year ended December 31, 2010. How is that possible? Did management really run a $67 million revenue business during 2010 entirely on a cash basis?

- Despite having a beginning cash balance in January 2010 of over $14 million and an ending cash balance at December 31, 2010 of over $35 million, the company only generated $35,000 of interest income during 2010 according to its 10-K filing. Even a 1% yield on an average cash balance of $24 million would have generated $240,000 of interest income during the year. Does management maintain its cash balances in non-interest-bearing accounts and, if so, why?

On the day the stock was halted, the company held a conference call before the market opened. I made sure that the GeoTeam would ask a question about the bank account disclosure risk that for some reason no one seemed to be talking about. Well, a YUII representative on the call actually admitted, on record, to depositing around $12 million into his personal account. After this statement, another YUII representative was heard in the background, speaking in Mandarin, that he should not have said that. Minutes after that comment, the NASDAQ halted the stock in the premarket after it traded 1.7 million shares. In retrospect, what amazes me most about this case study is that YUII continued and was permitted to trade for 3 days, even given the market’s knowledge of this risk factor.

Nothing illustrates this frustration better than this YouTube video of an investor who bought YUII that morning premarket and got stuck in the halt.

YUII is a hard-core lesson that not all risk factors are boilerplate. Obviously, not all are going to be this type of slam dunk. You also have to understand that not all negative boiler plate risk factors will manifest into something tangible and actionable. But you should definitely understand them when they are associated with a potential investment. Studying and knowing where to find risk factors in 10K SEC filings are good first steps to perform this task. In other words, read the “dayam” risk factors.