- Global Expansion: The company has outlined plans to increase its presence in global markets, which are currently less than 10% of its revenue.

- Acquisitions: Last year, the company made an acquisition to execute its new global market focus, acquiring a company that will help extend its reach as well as introduce a competitive “moat” type product line.

- Earnings Growth: The company is entering a phase of strong earnings growth, where we expect most (if not all) of the next 14 quarters to show strong growth.

Valuation

While the company’s current trailing P/E ratio of approximately 20x might seem a little expensive, we see potential for substantial upside. Looking at the valuation on a trailing basis is like looking in the rearview mirror, as many investors are doing. This is what is giving us an opportunity ahead of what we think is coming.

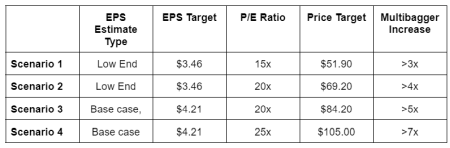

A reasonable P/E ratio of 15x applied to the low end of our EPS target of $3.46 would imply an eventual price target of $51.90.

However, using a P/E of 20x, the P/E the stock is currently trading at, would imply a target price target of $69.20. Referencing our base case earnings per share estimate of $4.20, we derive a price target of $84.00.

Ultimately, considering the company’s growth trajectory, a multiple of 25x a on base case earnings per share estimate should be in the cards, justifying an eventual price target of $105.00.

Key Facts

Themes

BigCapMicro; Restructuring; New Products; Strong Earnings Power Ranking; InfoArb

Catalyst(s)

Recent Acquisition; Expanding Into global markets; Strong earnings growth for multiple quarters in a row; Gaining more revenue from current customers due to cross selling; Analysts will have to increase their financial estimates.

Industry

Safety Products

Price & Revenue

Price; $10 to $20; Revenue: >$100M