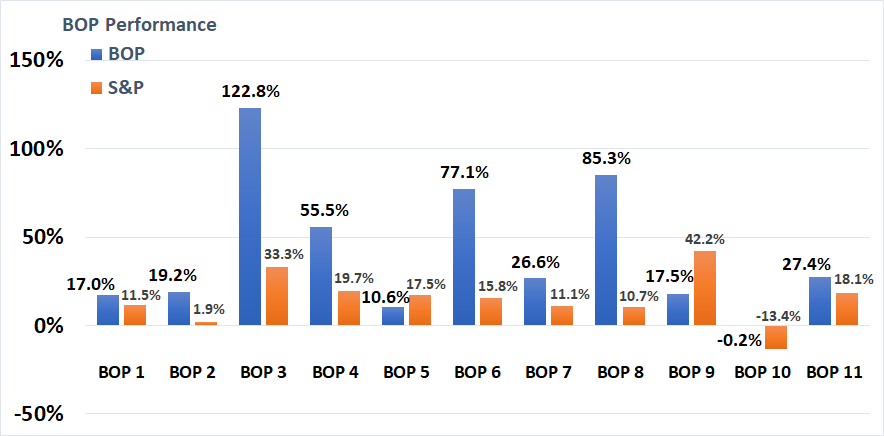

Besides stock education, stock picking ideas, video investment pitches, investor solutions, and model portfolios that beginner investors benefit from at GEO, we also provide other stock investment services that more experienced investors, such as stock analysts and fund managers, have been utilizing since 2007.

Investors use GEO to help them with their own research or as a way to add ideas to their own research pipeline. Our members appreciate that we perform in-depth research on companies, going beyond press releases to read SEC filings and conference call transcripts. Our stock analysts also perform on-site company visits and interview CEOs and CFOs of companies we are researching. Our nearly daily premium newsletters written by our own stock analysts provide breakdowns of company earnings reports, as well as stock coverage updates on stocks entering and exiting our model portfolios. Our analysts publish:

Detailed research reports on our highest conviction microcap stocks

Shorter form reports, or what we call Reasons For Tracking, on stocks that are just starting to attract our interest

Quick daily and weekly research briefs on stocks in our coverage universe

We were recently contacted by a premium member who said:

Thank You Geo! Hi Maj & the Geo team, I joined Geo in October so I can’t technically say “thanks for a great year”, but I have every intention of being able to next year! You can consider my subscription recurring revenue. Joining Geo was a big transition from how I previously traded but it has been the best decision I’ve made since starting this journey in 2014. I love the research-driven approach to the opportunity-abundant microcap market and the ability to use my accounting and finance background in decision-making, without having to monitor every market move. My account hit a record annual % gain this year even though I joined in October. The generous market probably helped, but so did Geo. Thanks for everything you do, and I wish you all the best in 2021! Aaron

To be clear, beginner to intermediate investors will also see tremendous benefits from the intense microcap stock research we do and the stock investing education we provide. We allow our members to experience the kind of research and stock analyst education that Wallstreet only saves for their wealthiest clients.

If you are new to investing, Geoinvesting provides the best stock education around and can teach you how to become an investor. We’re one of the best companies around that can help you learn how to invest in stocks and find the best microcap stock picks today. Our services are also beneficial to investment clubs and investment groups.