NV5 Holdings Inc (NVEE), trading around $13, is our most recent GeoBargain.

The GeoTeam is always on the lookout, not only for good businesses to invest in but perhaps more importantly, businesses with proven management teams. This selection process led us to find GeoBargain Costar Tech Inc (CSTI), an idea we alerted premium GeoInvesting members to on August 16, 2013 at $4.10. Shares of CSTI are up 265% since then.

In NV5 Holdings, we have found a management team that has rapidly built the company from a startup in 2009 to a growing, highly profitable, and formidable firm that provides professional and technical engineering, as well as consulting solutions, to public and private sector clients in the infrastructure, energy, construction, real estate and environmental markets.

- NV5 Holdings fits our criteria for a GeoBargain; it’s cheap and it’s led by a management team with significant pedigree and a proven track record.

- Dickerson Wright, NVEE’s founder has a history of entrepreneurial success that we believe will continue with the growth of NVEE.

- Management is targeting $300 million revenue and 12% to 15% EBITDA by 2016, a feat that we think they can achieve and is supported by industry dynamics.

- We believe that recent cash from a warrant redemption will be put to good use as management continues to pursue accretive acquisitions.

- Our price target of around $21.00 does not take into account future acquisitions that we think NVEE will complete that should be accretive to earnings.

NVEE completed its IPO in March 2013, and the resulting performance of the company speaks for itself. The company initially offered 1.4 million units of common stock and warrants to investors for $6.00 per unit. The market cap at the time of the company’s IPO was around $25 million. The market cap has recently hovered around $75 million. Since the IPO, that is a rate of return that is approaching 200%, and we think the company is just getting started. Our near-term price target of around $21.00 does not take into account future acquisitions that we think NVEE will complete that should be accretive to earnings . Shares are off about $2 from their recent high of $15.24, as investors have wrongly lumped the company into the pool of firms that will be negatively impacted by falling oil prices.

Before going into the particulars of NVEE’s operations and performance, it is important that investors learn more about who manages the company, as well as some of the guiding philosophies that are driving NVEE’s success.

NVEE Strong Management Team

Often, companies have strong management teams with great plans for the future. They are highly poised and confident in their abilities to drive their businesses and build value for shareholders. There is a big difference, however, between committing to doing something without having done so before and having already accomplished in similar situations what you are setting out to do now. NVEE has a founder/leader and management team who are industry veterans that have already been highly successful in their previous entrepreneurial business endeavors.

NVEE was founded by Dickerson Wright, PE Chairman, CEO and President in 2009. Mr. Wright founded U.S. Laboratories Inc. in 1993, completed an IPO in 1999 and sold the company to Bureau Veritas in 2002 for $83 million cash, or $14.50 a share, a 48% premium over the price prior to the announcement of the transaction. He next served as CEO of Bureau Veritas (“BV”) North America from 2002-2008 and grew the company’s revenues from $80 million to $300 million. He continued to push his entrepreneurial endeavors forward when he founded NV5 in 2009, and started operations with the same key managers who served him so well in his previous companies.

To gain insight into Mr. Wright’s business philosophy that has served him and his shareholders so well during his career, we referenced an interview of him done by The Wall Street Transcript in August 2001. What was true then still applies today, as he drives NVEE to what could potentially be an even greater success than what he achieved with US Laboratories. Specific quotes from his 2001 interview that piqued our interest include:

- Acquisitions : “We will not buy a company that does not have a blue chip client base, does not have a long relationship with their clients, that does not have a history of making a profit, does not have a second tier management group that’s willing to stay on with our company, and last, a company that we think that we can add value to.”

- Operating philosophy : “We run a very decentralized company and we are truly a practice. We have a very flat organization, we rely on our people, we rely on our operating principles, and we are really the only publicly traded company that I know of that is aggressively looking for acquisitions in a very fragmented industry.”

- Mangers with skin in the game : “We also drive stock ownership very, very deep into the company, so that when we bring people on, we bring people on in an equity position where they feel that they are working as owners of the company. We have wonderful bonus plans and a compensation plan with equity so that we bring on partners, we don’t bring on employees.” Note that according to NVEE’s 2013 Form 10K, Mr. Wright owns 38.3% and directors and executive officers as a group 47.1% of NVEE’s shares.

What NVEE Does and How it Bills Customers

NVEE’s Form 10-K for the year ended December 31, 2013, gives an excellent description of what the company does for its clients:

“We are a provider of professional and technical engineering and consulting solutions to public and private sector clients. We focus on the infrastructure, construction, real estate, and environmental markets. The scope of our projects includes planning, design, consulting, permitting, inspection and field supervision, and management oversight. We also provide forensic engineering, litigation support, condition assessment, and compliance certification. Our primary clients include U.S. federal, state, municipal, and local governments; military and defense clients; and public agencies. We also serve quasi-public and private sector clients from the education, healthcare, energy, and utilities fields, including schools, universities, hospitals, health care providers, insurance providers, large utility service providers, and large and small energy producers.”

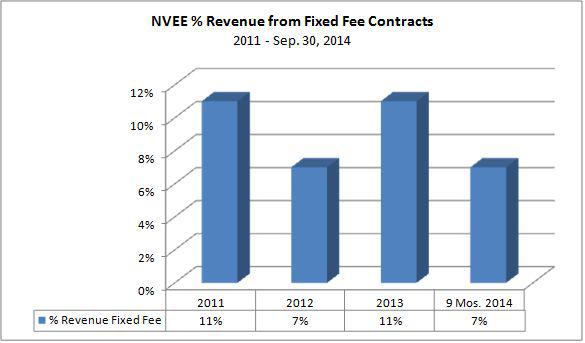

The company conducts business by entering cost-reimbursable and fixed fee/lump-sum contracts with its clients. Fixed fee/lump sum contracts require that all work be performed under the contract for a specified lump-sum fee, subject to adjustment if the scope of the project changes or if unforeseen conditions arise. Cost-plus contracts are predominantly used by US federal, state and local governments. Under these arrangements, the company bills its customers for actual costs and overhead plus a predetermined fee. When using cost-reimbursable contracts, NVEE bills the customer for actual hours expended on a project at negotiated rates (time and materials arrangements) or at predetermined rates (cost plus) in which customers are billed for actual hours expended on a project. Fixed contracts introduce an element of risk if the company underbids a project that it has been awarded. It appears that NVEE management is aware of this risk, since fixed price contracts have historically not accounted for a major portion of revenues. Since 2011, NVEE’s % of revenues generated by fixed fee contracts have ranged between 7% and 11%. In contrast, its closest competitors are much more exposed to fixed fee commitments – TRR @ 37% and WLDN @ 31%.

NVEE operates in five business verticals:

- Infrastructure (24% of 2014 revenue): Civil engineering, structures, transportation, water resources, surveying, construction management.

- Construction Quality Assurance (“CQA”, 19%): Code compliance, forensics, geotechnical engineering, materials testing, special inspections, technical drilling.

- Energy (33%): Environmental permitting, inspections, program management, design, surveying provided primarily to natural gas supply and energy generating companies.

- Program Management (18%): Program management, owner’s representative, preconstruction services, construction management.

- Environmental (6%): Environmental, occupational health and safety, environmental risk management, cultural resources, wetland studies, archeological studies, hydrogeological engineering, environmental permitting.

Investors concerned about the recent decline in oil prices should note that the clients/sectors NVEE serves have nothing to do with oil and oil exploration. The company’s clients are engaged in natural gas pipeline and services in the North East, Mid Atlantic and South East, and public utilities that generate energy.

Strategic Acquisitions Drive Growth Strategy

In a recent call with management, we learned that NVEE will aggressively seek strategic acquisitions that will enhance and expand the company’s service offerings. At any given time, the company has several deals in its pipeline. In fact, since our call at the end of January, one transaction has already recently closed . Typically, the company will close transactions at 4X to 6X trailing earnings while NVEE itself currently trades at around 14X its estimated 2014 earnings.

There are almost boundless opportunities for NVEE to grow through accretive acquisitions.

The company estimates there are 144,000 engineering firms in the US with under 50,000 of those in NVEE’s “sweet spot,” which includes companies is posting revenues of $4 million to $40 million. Despite the large number of potential acquisition prospects, relatively few meet NVEE’s requirements. The company describes its acquisition strategy on page 8 of its 2013 Form 10- K , which states:

“We intend to pursue the following growth strategies as we seek to expand our market share and position ourselves as a preferred, single-source provider of professional and technical consulting and certification services to our clients:

- Seek strategic acquisitions to enhance or expand our services offerings . We seek acquisitions that allow us to expand or enhance our capabilities in our existing service offerings. In analyzing new acquisitions, we pursue opportunities that provide critical mass to function as a profitable stand-alone operation, are geographically situated to be complementary to our existing operations, and profitable with strong potential for organic growth. We believe that expanding our business through strategic acquisitions will enable us to exploit economies of scale in the areas of finance, human resources, marketing, administration, information technology, and legal, while also providing cross-selling opportunities among our vertical service offerings.”

Increasing NVEE’s Growth Profile While Mitigating Business Risk

Approximately two thirds of NVEE’s revenues are derived from public (U.S. government) and quasi-public clients, but the private sector also provides great potential. We are impressed that the company has been able to grow its government business in times of tight budget conditions. This partly has to do with the fact that the public sector can no longer ignore the need to address the decaying U.S. infrastructure problem. Yet, management still understands that it needs to build up its private sector business to improve its growth outlook, reduce risk that comes with a reliance on the government and to experience an expansion of its valuation multiples. The investor kit on the company s website provides key information and data points for investors including the enormous scope of opportunities the company is positioned to pursue:

- Private Sector Opportunity – $641 billion in energy-related capital expenditure forecast in U.S./Canada 2014-2035.

- Public Sector Opportunity – The deteriorating U.S infrastructure will require $3.6 trillion of investment by 2020.

Management describes its business strategy in the 2013 Form 10-K, page 8, as follows:

“Continue to focus on public sector clients while building private sector client capabilities. We have historically derived the majority of our revenue from public and quasi-public sector clients. For the years ended December 31, 2013 and 2012, approximately 67% and 66%, respectively, of our gross revenues were attributable to public and quasi- public sector clients. Even during unsteady economic periods, we have capitalized on public sector business opportunities resulting from outsourcing initiatives, continued efforts to address the challenges presented by the nation’s aging infrastructure system, and the need to provide solutions for transportation, energy, water, and waste water requirements. However, we also seek to obtain additional clients in the private sector, which typically experiences greater growth during times of economic expansion, by networking, participating in certain organizations, and monitoring private project databases. We will continue to pursue private sector clients when such opportunities present themselves. We believe our ability to service the needs of both public and private sector clients gives us the flexibility to seek and obtain engagements regardless of the current economic conditions.”

NVEE in Sync with Industry Trends and Challenges

A recent article listed the top ten business trends engineering firms should look for in 2015. Three of those trends are particularly relevant to NVEE:

- “2014 was a great year with a resurgent economy boosting profits of firms across the country. This will continue into 2015. Firms can’t find enough talent quickly enough to meet demand -this simple equation will drive us toward a record profit year in 2015.

- A big concern for firms is finding talent. It’s back to the pre-recession market for talent.

- Mergers and acquisitions will have a record year in 2015 and will increase some 25% over 2014. The industry is at a tipping point from a consolidation perspective. High-performing firms in hot markets and geographies will command record valuations.”

NVEE’s management has already demonstrated their prowess capitalizing on acquisition opportunities. The key challenge for any engineering firm that is growing rapidly is managing its human resources and making sure they have the talent their clients need when it is needed. NVEE is well in tune with this issue and a key component of the company’s growth strategy is focused on its most critical asset – human capital. It is therefore not surprising that a top business priority is to:

“Strengthen and support our human capital . Our experienced employees and management team are our most valuable resources. Attracting, training, and retaining key personnel have been and will remain critical to our success. To achieve our human capital goals, we intend to remain focused on providing our personnel with entrepreneurial opportunities to increase client contact within their areas of expertise and to expand our business within our service offerings. We will also continue to provide our personnel with training, personal and professional growth opportunities, performance-based incentives, including opportunities for stock ownership, and other competitive benefits.”

Operating Performance since IPO Indicates Business Strategy is Working

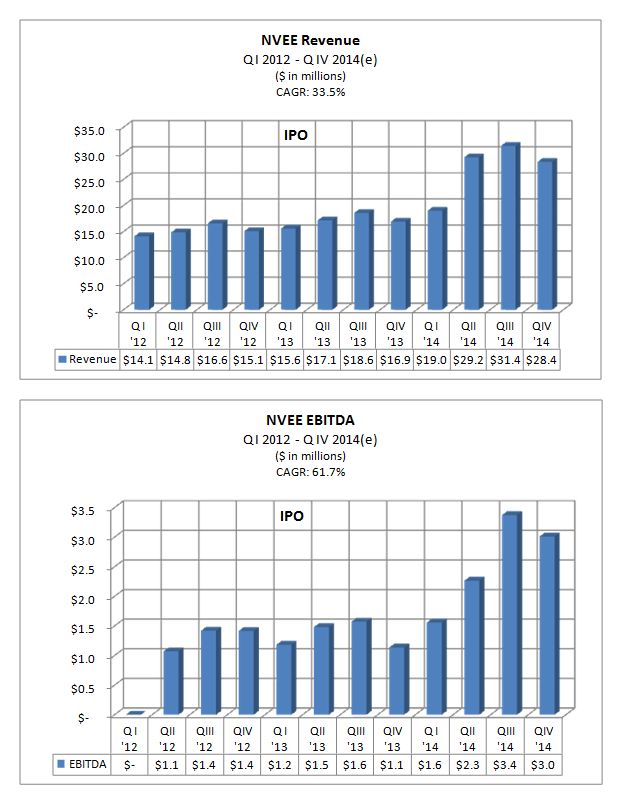

Factoring in NVEE’s 2014 financial guidance , the company will have produced uninterrupted revenue and net income growth every quarter since its IPO on March 26, 2013, while 5 of 7 quarters will have shown sequential revenue growth (keeping in mind that Q4 is seasonally the company’s weakest quarter).

In the most recently published financial results for the nine months ended September 30, 2014 , the company reported (page 25) that its revenues increased by $28.3 million, or 55.2%, compared to the same period in 2013. Acquisitions completed during the first nine months of 2014 accounted for $19 million or 67% of the year over year revenue increase. It’s not just acquisitions, however, that are driving NVEE’s revenue growth. Organically, the company has also been growing its business impressively. During first three quarters of 2014, the company’s existing business platform, excluding acquisitions closed in 2014, grew by $9.1 million or 18%.

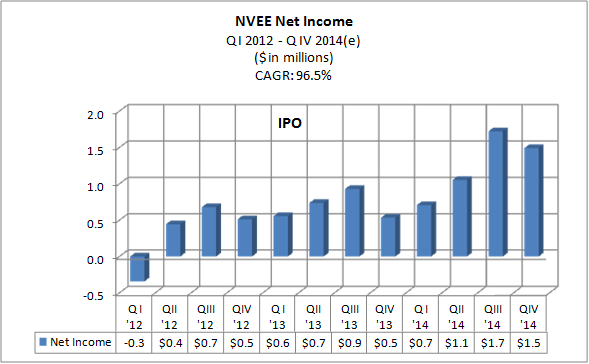

Overall, NVEE has shown impressive revenue, EBITDA and net income growth since completing its IPO in March 2013. Particularly noteworthy is that CAGR for revenues: EBITDA and net income since the IPO were 33.5%, 61.7% and 96.5%, respectively.

The fact that EBITDA is growing at a more rapid rate than revenues and net income more than EBITDA validates management’s ability to acquire net income streams at lesser multiples than NVEE’s shares command in the market. It also indicates the company has an organizational structure that enables management to absorb an ever increasing number of complementary businesses and greater revenues across its existing infrastructure.

The following charts reflect quarterly (Q IV 2014 estimated) revenues, EBITDA and net income for the period 2012- 2014.

Management’s Ambitious Growth Targets are Achievable

Management is targeting $300 million revenue and 12% to 15% EBITDA by 2016. The EBITDA % target is certainly reasonable as in Q III and Q IV(e) the EBITDA % was over 10% and it was over 9% for all of 2014. NVEE’s EBITDA target % is also comfortably within the range of its closest competitors that range from 6% to 10% for TRR and WLDN.

The $300 million revenue target is much more aggressive. The current annual run rate for revenues, including the recent acquisition of a $10 million business, is around $120 million. If we allow for 18% organic growth in 2015 and 2016, the existing business platform should generate around $170 million in 2016. That means management will have to complete acquisitions that will generate $130 million revenue in 2016. Based on management’s track record, we believe they will achieve that.

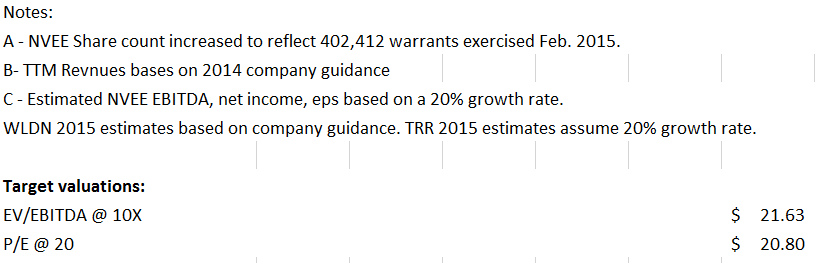

If NVEE reaches the stated revenue target of $300 million in 2016, generates 12% EBITDA, depreciation and interest expenses are $4 million, the effective tax rate remains at 37%, and the share count is 8 million after inevitably issuing new shares to help fund acquisitions (currently 6.1 million after exercise of warrants), EPS two years from now could be $2.50 or more.

Warrant Redemption Leads to 99% Exercise Rate

Investors recently gave NVEE a vote of confidence.

The company successfully redeemed all of its outstanding public warrants . 99% of the warrants were exercised at $6.80, generating approximately $3.2 million. We have confidence that this cash will be put to good use as management continues to pursue accretive acquisitions.

Some Caveats

In order to provide balance and objectivity, the following are among the risk factors investors should consider:

- Human resources : Growing its business and winning new contracts does NVEE little good if they don’t have the professional staff needed to do the work. The loss of key personnel or inability to attract and retain qualified personnel when required to meet client needs could disrupt and ultimately damage the business. This is a critical issue because as the macro economy improves the demand for topflight engineers will only become more intense. This environment will inevitably lead to not only competition to recruit talent but also drive compensation higher ultimately squeezing margins if NVEE is unable to pass costs on to clients.

- Key personnel : NVEE depends on the continued services of its Chairman, Chief Executive Officer, and President, Mr. Dickerson Wright, and the management team he has assembled. Mr. Wright is the visionary and driving force behind NVEE and its success. His unique knowledge, experience, skills, and relationships with major clients and other members of the management team have been a key factor in NVEE’s success to date. Although this dependence will become less critical longer term the loss of his services in the near or intermediate term would adversely affect operations.

- Concentration of business with government agencies : NVEE derives two-thirds of its revenues from public and quasi-public clients the majority of which (over 80%) are in California. A significant amount of the revenue is derived from multi-year contracts with many appropriated on an annual basis. Consequently, at the beginning of a project, the related contract may be only partially funded, and additional funding is normally committed only as appropriations are made in each subsequent year. NVEE is therefore vulnerable to the vagaries of government politics and spending.

- Gross Margins : NVEE’s Gross margin is double that of some of its competitors, which could lead some investors to speculate that this level of margin may not be sustainable over the longer-term.

Estimated Valuation

We believe that based on NVEE’s current operations, 2014 operating performance and relative valuations of other companies engaged in professional services businesses, that NVEE’s stock is undervalued. NVEE’s Filings list the following companies as being among its principal competitors:

- Jacobs Engineering Group Inc (JEC)

- Tetra Tech Inc. (TTEK)

- TRC Companies Inc. (TRR)

- Willdan Group, Inc. (WLDN)

We threw out JEC and TTEK as valuation comps since they are multi-billion dollar companies. That leaves us with TRR and WLDN. We put greater emphasis WLDN since it has experienced consistent growth over the past several quarters compared to TRR. (Although on a sub-note, TRR might be a stock to watch if the company can begin to deliver consistent top and bottom line growth, helped along by acquisition activity).

We believe that NVEE should ultimately trade at a premium valuation for the following reasons:

- NVEE has shown the most consistent growth in both revenue and net income since 2012

- NVEE management pedigree and track record

- Less risk in business plan due to lower emphasis on fixed-price contract projects

- Comparable gross margins

- Aggressive growth planned for next two years from a management team that has delivered in the past

We used two measures to arrive at what we believe to be achievable multiples and we peg NVEE’s value at around 70% more than its recent trading price of around $12.50 per share; EV/EBITDA of 10X, and P/E of 20. Our target price for NVEE, based on the median of these three metrics, is approximately $21.00.