In 2016, Fitlife, founded over 18 years ago, was on the verge of bankruptcy, selling its nutritional supplements through brick and mortar channels, with GNC as their biggest customer.

Brick and mortar revenue can become unpredictable since, in the case of smaller companies, distributors and retailers can dictate pricing, what products to carry and how the product is marketed to customers, potentially the degree of success these smaller companies may achieve, a scenario FTLF was facing with GNC.

So, when an investor/activist, Dayton Judd, entered the picture, he bought a large percentage of the company’s stock and eventually took control of the company, becoming CEO, where he began his efforts to turn the company around.

He improved the balance sheet by selling off receivables at a discount to bring cash into the company, instituted new ways to market the company’s products, and developed an online direct-to-consumer strategy.

Eventually, the company got to a point where it was strong enough to look for acquisitions, culminating in the company buying two nutritional supplement businesses over the last 12 months.

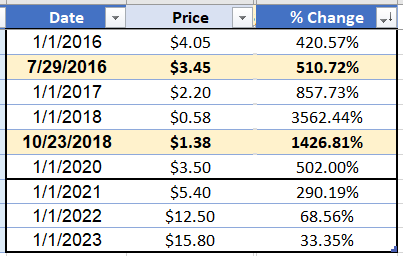

Since Judd took over, revenues have increased from $17 Million to $45 Million, and Earnings Per Share have increased from losses to a current annual EPS run-rate of $1.44. Today, on-line revenues represent 68% of total revenues.

Finally, outstanding shares are about 4.5 million today, versus what they were when Judd took over in 2016, 4.2 million – an only 7% increase.

So, what’s so special about the company I’m looking at right now whose story is so similar to that of FTLF’s?

For starters, this company’s outstanding shares have actually decreased 12.8% since the mid 1990s (the earliest SEC filings we could reference).

This company is in the same industry as FTLF and has been around since 1985 (to reiterate, this checks off the long operating history criterion).

Previously, shares traded at ~$13, and the stock is now well under $1. The company was on the verge of debt-induced bankruptcy and struggled to maintain relationships with its retailers and distributors.

The old CEO’s tenure was riddled with mis-executions, as well as related party transactions and shareholder battles, also similar to FTLF.

Now, with the leadership of a new CEO and a turnaround plan (6th trait above), the company sold one of its assets to pay off all of its debt and has one of the highest cash balances in its history. He has also embarked on an aggressive online marketing strategy where they are already seeing this revenue grow by almost 50%.

The company is also concentrating on its higher margin products with the belief that they, combined with all of the turnaround moves, will result in the company quickly returning to profitability.

What I find interesting here is that the stock has fallen to bankruptcy price levels because of the once weak balance sheet. However, the stock has barely moved upwards after it announced that it restructured its balance sheet.

I think investors have become sick of the company’s past management narrative of overpromising and under delivering. But, what they might not realize is that the company is now being run by the new CEO.

It appears the new management team is much more shareholder friendly, and is executing on turnaround initiatives that previous management could not bring to the finish line.

This set-up is almost an exact blueprint to FitLife.

It’s such a blueprint that I’m going to introduce the CEO of FTLF to this company to see if he might be interested in joining their Board of Directors.

If this opportunity makes sense to you, then please join GeoInvesting Premium today to follow my due diligence journey and receive access to all of our premium content.