Summary

- Our extensive on-the-ground due diligence at Sino Grandness Food Industry Group Limited’s (“SGFI”) canned goods manufacturing subsidiaries showed little to no activity. It appears as though either 2016 will be a massively disappointing year, or prior year’s annual results were significantly overstated.

- We obtained 2014 and 2015 SAIC files for SGFI beverage subsidiaries in July and again in August. The SAIC files obtained in July indicated light production according to revenue numbers, leading us to believe that combined with our on-the-ground due diligence, SGFI’s revenues reported in press releases and annual reports to investors are significantly overstated.

- The company’s SAIC files that we obtained in August show numbers for its beverage subsidiaries that are significantly bigger than numbers we obtained in July. We believe the company amended its filings so they would essentially “match” the numbers being reported in the prospectus of the beverage business as it prepares to go public in Hong Kong.

- It appears SGFI’s planned IPO of its beverage subsidiary in Hong Kong has suffered a setback, although few details have been given. We suspect the delay could be permanent, and that it might have put the company in a dangerous spot financially.

- With its “lapsed” Hong Kong IPO, the company is proposing a dilutive rights offering in Singapore at a substantial discount to its market price, while reporting robust business growth and claiming to have over RMB 500 million in cash and cash equivalents.

Introduction

For over 7 years, GeoInvesting has been providing unprecedented looks on-the-ground at companies and businesses listed in the United States but domiciled in Asia. Over the course of these 7 years, we have exposed both the good and the bad — when we see material misrepresentations or fraud, we bring it to the attention of investors and regulators. Over 12 companies have been halted or delisted on our reports, and we have exposed more than $10 billion in market cap worth of fraud or material misstatements. When we find that a company is doing exactly as it claims, we are happy to report that as well. Our commitment from the beginning has always simply been to uncover the truth about companies, present it with as little sensationalism as possible, and then let the market decide accordingly. Most importantly, our on-the-ground diligence has been giving investors and regulators looks into businesses that can’t practically be fully vetted by investors isolated by geographical, lingual and cultural challenges.

For the first time, our research has brought us to Singapore, where we have been conducting on-the-ground due diligence on Sino Grandness Food Industry Group. Sino Grandness Food Industry Group Limited (“SGFI”) was established in 1997, and is principally engaged in the production and distribution of beverages in China under the name é²œç»¿å› (“Garden Fresh”) and canned food products under the name of 振é¹è¾¾ (“Grandness”). SGFI trades in Singapore under the symbol SGX:T4B and in the United States on the Over the Counter Market under the symbol SFOOF

On-The-Ground Due Diligence Indicates To Us a Deterioration of Canned Business

In sum, SGFI operations play host to seven total subsidiaries engaged in manufacturing activities for both the beverage business and the canned goods business. The following chart shows the company split up into its manufacturing subsidiaries:

(note: Shenzhen Garden Fresh and Shenzhen Grandness do not have manufacturing facilities)

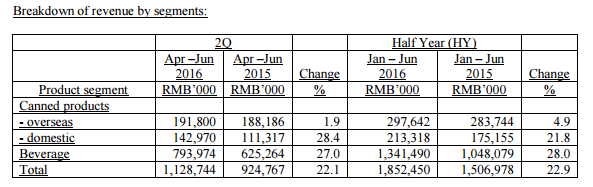

According to SGFI’s Q2 2016 financial results reported in its earnings release, its domestic canned products business increased 28.4% YOY and its overseas canned products business increased 1.9% YOY (its overall canned products business increased 11.8% YOY). On a half year 2016 basis, the company’s domestic canned products business increased 21.8% YOY and its overseas canned products business increased 4.9% YOY (overall canned products business increased 11.3% YOY).

Source: SGFI’s Q2 2016 earnings release

After reviewing the company’s financials in press releases and its beverage business IPO prospectus, we also conducted on-the-ground due diligence at seven manufacturing subsidiaries of SGFI, including at both their canned food and beverage businesses. We expected to see robust business operations at each of these subsidiaries, but instead were surprised to see several facilities shut down or idled. Based on our due diligence and observations, we believe that SGFI’s canned business is shrinking, if not totally shutting down, rather than expanding. We’ve also concluded that the company’s in house beverage business does not appear to be anywhere near the peak shape that the financials suggest.

We note that the company has claimed outsourcing and self-production each represent about 50% of its total beverage production capacity in its Hong Kong IPO filing, yet with its canned products segment, there is no mention of outsourcing that we could find.

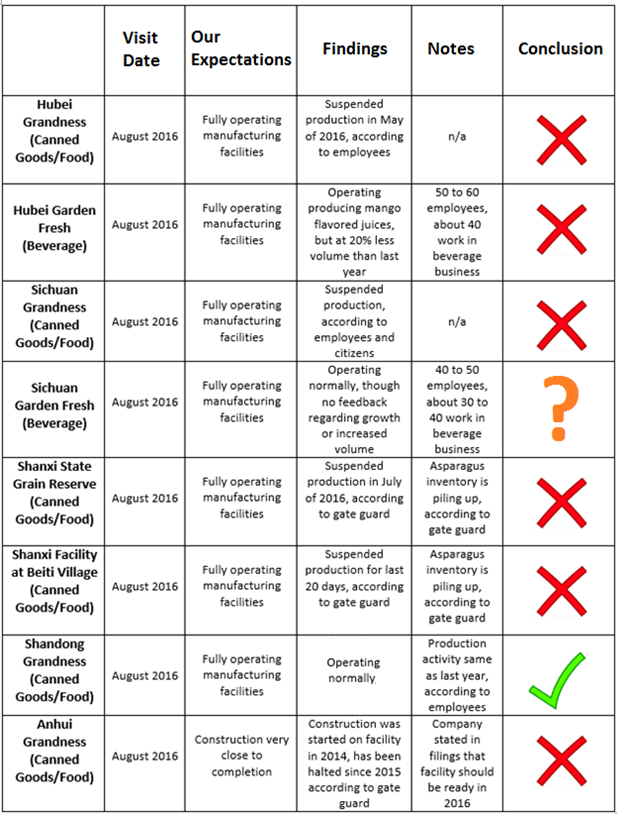

Here is a summary of how our on-the-ground due diligence did not meet our expectations at 6 of the 8 subsidiaries we visited.

Here are our detailed findings from our on-the-ground visits to these locations:

Hubei:

1.Grandness (Hubei) Foods Co., Ltd (湖北振é¹è¾¾é£Ÿå“有é™å…¬å¸) &

2.Garden Fresh (Hubei) Fruit and Beverage Co., Ltd. (鲜绿å›(湖北)食å“饮料有é™å…¬å¸)

We obtained Hubei Grandness’s SAIC file in August of 2016, which indicates that its production was very light in 2014 and 2015. In it, we found the following data:

Grandness (Hubei) Foods Co., Ltd (湖北振é¹è¾¾é£Ÿå“有é™å…¬å¸)

Both Hubei Grandness and Hubei Garden Fresh are located in the city of Yichang, Hubei Province and both companies use the same production facility. Hubei Grandness mainly produces canned fruits and Garden Fresh is primarily in the beverage business. Our diligence indicates Garden Fresh Hubei currently has 50 to 60 employees, of which about 40 workers for the beverage business, according to employees that we spoke with.

When we arrived, we expected to see fully operating manufacturing facilities. According to several employees at the Garden Fresh Hubei facility, Grandness’ canned goods business suspended production in the middle of May 2016, with only very minimal production activity before that. It was operating normally at the same time last year, according to the same employees. As of late August 2016, the canned products business was still suspended.

According to these employees, Garden Fresh’s beverage business is operating normally and is mainly producing mango flavored juices. We were told by employees that beverage production volume this year has been about 20% less than last year.

Below are our pictures of Garden Fresh (Hubei):

Sichuan:

3.Grandness (Sichuan) Foods Co., Ltd. (å››å·æŒ¯é¹è¾¾é£Ÿå“有é™å…¬å¸) &

4.Sichuan Garden Fresh Fruit and Beverage Co., Ltd (å››å·é²œç»¿å›æžœè”¬é¥®æ–™æœ‰é™å…¬å¸)

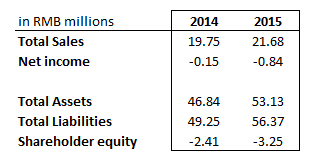

Sichuan Grandness’s SAIC file, obtained in August 2016, shows the business deteriorating from 2014 to 2015. The SAIC info for Sichuan Grandness shows the following:

Sichuan Grandness and Sichuan Garden Fresh are located in the same facility in the city of Qionglai, Sichuan Province. According to various interviews with employees and local citizens, the facility currently has 40 to 50 employees, of which 30 to 40 are working on the beverage production line. The company’s canned goods business is currently suspended, but was operating normally at the same time last year, according to these same employees and citizens.

The beverage business is still in operation. Below are our pictures from outside the facility:

Shanxi:

5.Shanxi Yongji Huaxin Food Co., Ltd. (山西永济åŽé‘«é£Ÿå“有é™å…¬å¸)

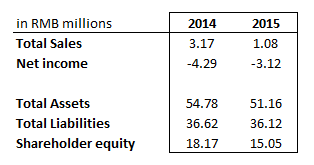

We obtained Shanxi Yongji’s SAIC file, from which we can draw the conclusion that Shanxi Yongji’s business was deteriorating substantially from 2014 to 2015. Based on our on-the-ground due diligence, the business could be experiencing an inventory glut. Shanxi Yongji’s SAIC data is as follows:

There are two facilities located in city of Yongcheng, Shanxi Province. Upon arrival, we expected to see fully operating facilities but were surprised to hear that the company had suspended production. The first facility is within Yongcheng city’s State Grain Reserve, and the facility does not have a name plate outside. According to the gate guard, the company suspended its production in July of 2016, yet production was at normal operation during the same time last year. According to the gate guard, finished goods inventory is piling up in the warehouse and hasn’t been sold. The major product at this facility is canned asparagus.

Here is a picture of the first facility:

The second facility is located in Beiti Village, and its production is also suspended. According to its gate guard, its primary product is also asparagus, which has been over-produced resulting in a warehouse full of inventory. The gate guard also mentioned that, as of the time of our visit in August 2016, production had been halted for 20 days, and there is no timeline for resumption. Below are our pictures:

Shandong:

- Grandness (Shanxian) Food Co., Ltd. (山东å•åŽ¿æŒ¯é¹è¾¾é£Ÿå“有é™å…¬å¸)

Grandness Shanxian’s SAIC file shows that its business loses a considerable amount of money. Financial information for 2015 is conspicuously listed at zero.

Grandness Shanxian is located in Shan County, Shandong Province. The company is operating normally, according to its employees, mainly producing different types of canned products. The production activity this year is almost the same as last year. Based on the information given to us by its employees, it currently has more than 100 employees, and had over 200 employees at its prior peak season. Its major product is asparagus, with other supplemental products such as yellow peaches and oranges. Currently, asparagus production has been halted, and the company is mainly producing canned yellow peaches and oranges.

Below are our pictures of the facility:

Anhui:

7.Grandness (Anhui) Food Co., Ltd. (振é¹è¾¾ï¼ˆå®‰å¾½ï¼‰é£Ÿå“有é™å…¬å¸)

Grandness Anhui’s SAIC file shows that Grandness Anhui did not have any business in 2014 and 2015. The SAIC file shows the following:

Grandness Anhui is located in Guzhen County, Anhui Province. According to the facility’s security guard, SGFI started to build its current facilities in 2014, and its construction was halted around 2015. According to the same guard, no construction or business operations have taken place at the site since then, and the facilities have remained idle for more than one year. The company stated in its annual report that it expects construction to be completed this year. However, as we are nearing the end of 2016, we have serious doubts that construction will actually be completed on time, if at all, given the business condition we observed at SGFI’s other manufacturing facilities. The company’s 2015 annual report stated:

“In view of the growing demand of health-promoting products, growing affluence among the Chinese, and growth on retail sales, the Group will continue to focus on boosting its production capacities. With the new Anhui facility to be operationally ready in 2016, we expect to meet the rising demands for our products in the future.”

It continued:

“In financial year 2013, the Group has entered into a Cooperation Agreement with Guzhen (固镇) Municipal Government of Anhui Province, PRC whereby the Group principally agreed to invest RMB 600.0 million to construct a production plant to produce canned products and beverages. The investment cost would be executed in 3 phases whereby construction work was commenced in 2014 and expected to be completed by 2016.”

Below are our pictures of the facility:

The simple fact is that our on-the-ground due diligence at these manufacturing facilities for the company’s canned goods business largely contradicts with what the company has reported in press releases and its annual reports while listed on the Singapore stock exchange.

Garden Fresh’s SAIC Data Shows Alarming Discrepancies

The company’s beverage business may be the most important part of the company currently, as it is preparing for an IPO in Hong Kong under the “Garden Fresh” name. On April 1, 2016, Garden Fresh filed its IPO application with the Hong Kong stock exchange. Before this application, SGFI’s stock in Singapore had increased from 30 cents to 70 cents from January 2016 to April 2016.

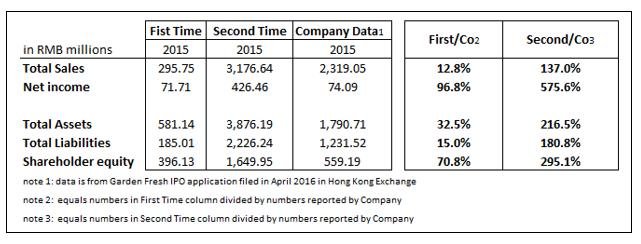

When we conducted our research on SGFI, we obtained Garden Fresh’s SAIC files on two separate occasions, including files for all three of Garden Fresh’s operating subsidiaries, Shenzhen Garden Fresh, Hubei Garden Fresh, and Sichuan Garden Fresh. We first obtained Garden Fresh’s SAIC files in July of 2016 and then obtained additional copies in August 2016.

What we found was that two of Garden Fresh’s three subsidiaries had different numbers on their SAIC files in July versus August 2016, with the more recent filings showing significantly higher sales, net income, assets, liabilities and equity. We found these differences with both Shenzhen Garden Fresh and Hubei Garden Fresh. Due to vast differences in the files we pulled for the beverage business, we chose to go one step further and pull the files for the company’s canned foods business. Here’s the comparison of what these files listed previously, with what they listed the second time we checked, for the three beverage subsidiaries:

Subsidiary 1

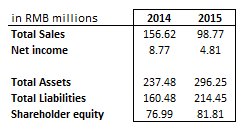

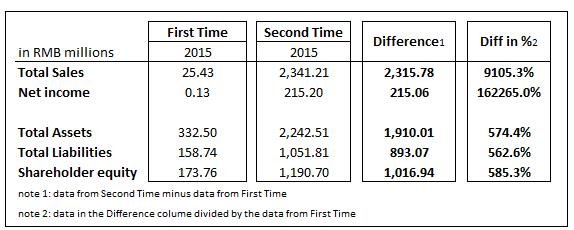

Garden Fresh (Shenzhen) Fruit and Beverage Co., Ltd (鲜绿å›(深圳)果蔬饮料有é™å…¬å¸)

The total sales in 2015 were 9105.3% higher than the number obtained the first time (2.32 billion RMB higher), and the net income is over 162,000% higher on the new file (215 million RMB higher). On the balance sheet side, total assets, total liabilities and shareholder equity have all been raised to over 6 times what they were first listed at. For example, total assets were 1.91 billion RMB higher, and shareholder equity was 1.02 billion RMB higher.

What’s worth pointing out is that the second time we obtained the SAIC file, the financial data for Shenzhen Garden Fresh in for 2014 has been left blank. If the company was operating and reporting to SAIC, we’d expect at least some results for the year 2014.

Subsidiary 2

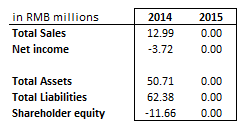

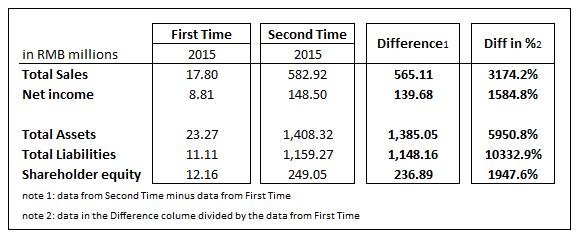

Garden Fresh (Hubei) Fruit and Beverage Co., Ltd (鲜绿å›(湖北)食å“饮料有é™å…¬å¸)

Total sales in 2015 were over 3100% higher than the number obtained for the first time (565 million RMB higher), and net income is close to 1600% higher on the second SAIC file (140 million RMB higher). On the balance sheet side, total assets, total liabilities and shareholder equity is over 5900%, 10,300% and 1900% higher than numbers listed the first time, respectively. For example, total assets were 1.39 billion RMB higher and shareholder equity was 237 million RMB higher on the second files.

Subsidiary 3

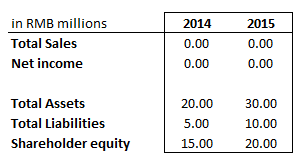

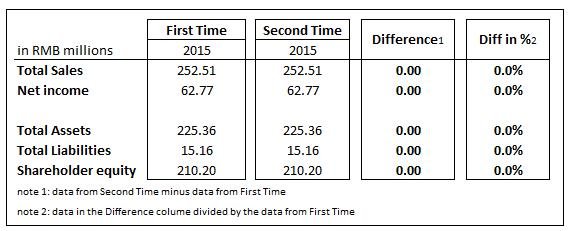

Sichuan Garden Fresh Fruit and Beverage Co., Ltd (å››å·é²œç»¿å›æžœè”¬é¥®æ–™æœ‰é™å…¬å¸)

The SAIC file financial data for Sichuan Garden Fresh is the same for both times we pulled the information.

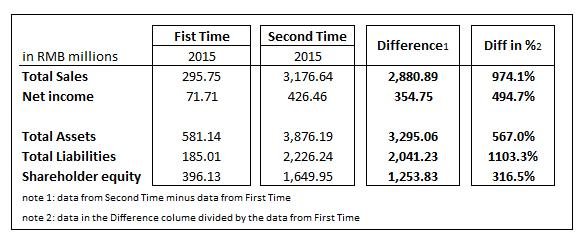

We also compared the aggregate amount of all three subsidiaries filed in SAIC obtained in the two different sets of filings:

Comparing the two different SAIC file data sets, the combined sales, net income, total assets, and total liabilities of the three subsidiaries of Garden Fresh in the second set of filings are 316% to 1103% higher than first set of filings we obtained. Total sales are 2.88 billion RMB higher, net income is 355 million RMB higher. Total assets are 3.3 billion RMB higher, and shareholder equity is 1.25 billion RMB higher.

We also compared the first and second data set with the financial numbers filed by Garden Fresh in its IPO application April this year.

One can see from the diagram above that for the year 2015, total sales per SAIC files obtained the first time were only about 13% of the 2.32 billion RMB reported in company’s filed IPO application. However, on the second file we pulled, the total sales are 137% of the number reported by the company. Net income per the first filing was almost the same as the number reported by the company, but on the second file, the net income is 426.5 million RMB, which is 576% of the number the company reported.

On the balance sheet, total assets per SAIC files obtained the first time were only about 33% of the 1.79 billion RMB reported in company’s filed IPO application. However, on the second SAIC file, the total assets are 217% of the number reported by the company. The total liabilities per the first filing was only about 15% of the 1.23 billion RMB reported in company’s filed IPO application. However, on the second SAIC file, total liabilities are 181% of the number reported by the company. Shareholder equity per SAIC files obtained in the first time was about 71% of the 559 million RMB reported in company’s filed IPO application. On the second SAIC file pulled, the shareholder equity is 295% of the number reported by the company.

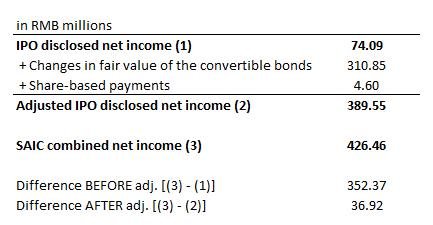

Reviewing the SAIC file data obtained the second time, the combined SAIC net income is 352.37 million RMB larger than the reported net income number for the IPO. This discrepancy could narrow to be 36.92 million RMB if we add back 310.85 million RMB of changes in fair value of the convertible bonds and 4.60 million RMB of share-based payments to the IPO disclosed net income of 74.09 million RMB. This brings the numbers much closer, and could indicate that the second set of SAIC file data we obtained reflects amended amounts to support the financials in the IPO filing. Here’s a chart we made to show the reconciliation:

In our view, these adjustments could help get the combined net income in the second set of SAIC files we obtained closer to the net income reported in the IPO filing. We are unclear if those adjustments could explain the vast difference in revenues, assets and liabilities between the second set of SAIC files and the amounts reported in the IPO filing.

Garden Fresh’s Suspicious Growth with Shrinking Numbers of Distributors

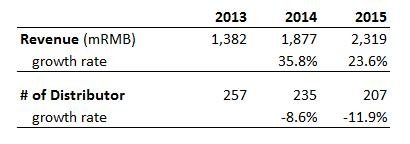

According to Garden Fresh’s IPO prospectus, the number of its distributors decreased by 8.6% from 257 in 2013 to 235 in 2014. This number further decreased to 207 in 2015. However, the company managed to grow its beverage business revenue from 1.38 billion RMB in 2013 to 1.88 billion RMB in 2014, an increase of 35.8%, and grow another 23.6% to 2.32 billion RMB in 2015. From our perspective, the shrinking number of distributors is more reflective of the weakness of the business as indicated by our on-the-ground due diligence rather than the strength reported in the IPO filing.

Is the Company’s Hong Kong IPO Dead on Arrival?

To the casual observer, SGFI’s business is performing exceptionally well. According to SGFI’s 2015 annual report, total sales increased from RMB 2.82 billion to RMB 3.31 billion, a year over year increase of 17.5%. The company’s gross profit also increased 21.8% from 2014 to RMB 1.37 billion. Finally, the company reported net profit of RMB 206.7 million in 2015, a decrease of 17.2% from RMB249.5 million in 2014.

On April 1, 2016, SGFI filed an application for an IPO of its beverage business in Hong Kong. To begin our due diligence, we pulled the SAIC files for the company’s beverage business, and only its beverage business, so that we could try and evaluate the data surrounding the company’s IPO.

As of today, the status of this IPO is listed as “lapsed” under the “inactive” section of the Hong Kong Stock Exchange website.

The company also admitted in a regulatory filing on September 30 that “there can be no assurance” that the IPO will take place:

The Company wishes to highlight that there can be no assurance that the approval for the Proposed Listing will be granted by the HKSE. In the event that the approval for the Proposed Listing is not granted by the HKSE, the Company will not be able to proceed with the Proposed Listing.

While the company gives mixed color on how the IPO will proceed, we can assure investors that the IPO will not be taking place for as long as it remains “lapsed” under the “inactive” section of the Hong Kong stock exchange website. However, SGFI proposed a rights offering in Singapore (despite the IPO schedule being scheduled in Hong Kong) to sell new shares to existing stockholders at a 28.7% discount to the stock’s recent price. We believe that this could mean that the company’s plan of raising capital through a Hong Kong IPO of its beverage business may have hit a wall, and the issuance of shares through the rights offering in Singapore tells us that the company is currently in need of capital. The company’s IPO prospectus was previously available publicly on the Hong Kong Stock Exchange website, but it is now currently unavailable through public means.

Based on SGFI’s most recent Q2 2016 financial results, the company booked 157.6 million RMB in net profit, an increase of 25.0% compared to the same quarter last year, and the company’s net profit for the first half of 2016 amounted to 517.7 million RMB, an increase of 121.3% compared to last year.

The company also reported cash and cash equivalents of 587.3 million as of June 30, 2016. Despite this cash on hand, the company is issuing up to 243,713,276 new ordinary shares at a price of S$0.31 per share, an aggregate of S$75.6 million (~368 million RMB) in a rights offering. The company stated 60% of proceeds, after deducting expenses, will be used for capital expenditures for the Group’s non-beverage business and 40% of it will be used for distribution network expansion as well as general working capital.

To us it seems strange that the company is proposing this rights offering at a 28.7% discount to its recent market price, despite reporting more than RMB500 million in cash and cash equivalents on its balance sheet while its net profit reportedly grows at a very high rate. This issuance will increase the company’s total share count by up to 33%. We believe this action could indicate that the company’s real financial condition may not be what has been reported. We also think this could mean that the company needs a capital injection in order to sustain its business operations, especially if it isn’t going to be able to raise capital from an IPO of its beverage business.

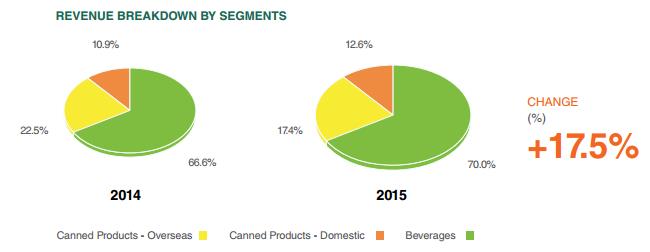

Below are the company’s revenue segments and corresponding geographies, according to the company’s 2015 annual report:

The company also disclosed the following detailed revenue segment breakdowns:

The company’s beverage business also looks, to the casual observer, to be performing exceptionally. According to the company’s reported financials, revenue from beverages sold under the Garden Fresh name increased from RMB 1.88 billion in 2014 to RMB 2.32 billion in 2015. Revenue from the canned food businesses increased from RMB 942.7 million in 2014 to RMB 994.9 million in 2015.

Shenzhen Grandness’ SAIC Files Raise More Questions than Answers

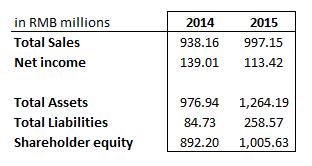

As part of our comprehensive due diligence, we pulled Shenzhen Grandness’ SAIC files for a deeper look at the company. As mentioned in SGFI’s annual report, Shenzhen Grandness is a trading company without manufacturing activities, engaged in the “sale of canned vegetables and canned fruits”. The numbers reported on its SAIC filing were:

As a sales and trading company with a leased office, we would expect Shenzhen Grandness to host only nominal amounts of non-current assets, different from the manufacturing arm of the business. Accordingly, we believe most of Shenzhen Grandness’s total assets should be current assets, such as cash and cash equivalents, trade receivables and inventory.

Based on Shenzhen Grandness’ SAIC file, in 2015, its total assets (which we believe should be mostly current assets) were about 1.26 billion RMB. However, parent company SGFI booked 1.527 billion RMB in current assets according to its 2015 annual report, meaning that Shenzhen Grandness, only one trading subsidiary of the company, likely occupied up to 82% of the total current assets of SGFI. We would not expect the majority of SGFI’s assets would come from Shenzhen Grandness, one of SGFI’s trading subsidiaries.

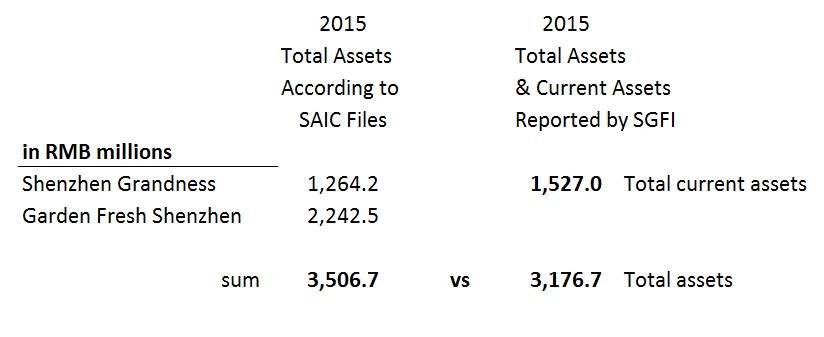

Garden Fresh Shenzhen, another trading company engaged in the “sale of fruits and vegetable juices” booked its total assets for 2015 in its SAIC file as 332.5 million RMB according to the first time we pulled the data and 2.24 billion RMB according to the second time we pulled the data. To reiterate, we believe as a trading company, most of Garden Fresh Shenzhen’s total assets should be current assets.

Combining these two trading subsidiaries’ total assets together, namely Shenzhen Grandness’ SAIC data and Garden Fresh Shenzhen’s second SAIC data, total assets (which we believe should be mostly current assets) based on these two SAIC files are RMB 3.5 billion. This is far more than SGFI’s reported current assets of RMB 1.527 billion (per its annual report), and even more than the total assets (both current and non-current) of RMB 3.17 billion reported by SGFI. Here’s a look at this data:

Shenzhen Grandness’ income statement data, such as total sales, closely matches SGFI’s disclosure regarding its canned goods business. Based on SGFI’s SAIC file regarding its manufacturing subsidiaries and our due diligence regarding those manufacturing subsidiaries, it is tough for us to believe that SGFI could have the sizeable canned goods business it has claimed.

This conflicting information on the company’s SAIC files only furthers the list of questions we have about the company’s integrity and corporate governance.

Potential Liability for the Company’s Hong Kong IPO Sponsors

We also wanted to make note of potential liability for the sponsors of the company’s beverage business IPO in the event that its financials and business condition are untrue or have been misrepresented. According to the Securities and Futures Commission “Supplemental Consultation Conclusions on the regulation of IPO Sponsors — Prospectus Liability” guide published in August of 2014:

“The SFC has accordingly reaffirmed its view that its original position in the Consultation Paper — that sponsors are already covered under the existing law — is correct. Sponsors are among those persons who have potential statutory criminal and civil liability under the CWUMPO for untrue statements (including material omissions) in a prospectus. It has therefore concluded that the proposed legislative amendments need not be pursued as they would serve no purpose.”

It should also be noted that SGFI’s Singapore auditor is Foo Kon Tan LLP, a former member of Grant Thornton in Singapore. Foo Kon Tan LLP separated itself from Grant Thornton in 2015. Foo Kon Tan LLP was also the auditor for two other Singapore listed China related frauds: China Printing & Dyeing Holding Limited and China Fibretech Ltd. SGFI’s Hong Kong auditor for its planned IPO is BDO Hong Kong, an audit firm that also has associations with notorious Chinese frauds, such as China Biotics (CHBT).

Should SGFI’s planned beverage subsidiary IPO continue, we would urge its sponsors to conduct further due diligence befitting of a company to which they wish to lend their name and credibility.

Reasonable Explanation or Rotten to the Core?

We would like to hear the company’s response to each of our findings. We find it very difficult to believe that SGFI’s business units are growing as reported by the company, taking into consideration the recently proposed dilutive financing to fund its business development.

For years, we have been specializing in on-the-ground due diligence in China and other parts of Asia. To supplement our on-the-ground research, we often look for help from a company’s SAIC filings. These filings can be a great secondary source to gather a financial picture to reconcile with our on-the-ground due diligence. There are times, like with SGFI, that the SAIC files simply don’t make sense for some subsidiaries. For this reason, we rely mostly on our first-hand observations, which we believe tell the story of a company that is not operating as its annual report and filings indicate to the public.

The SAIC files provided a mixed and inconsistent picture of SGFI. We are confident that our on-the-ground due diligence and the company’s recent baffling need to raise money in a dilutive rights offering at a discount both provide us with red flags that investors and regulators need to scrutinize carefully.

Our on-the-ground due diligence just plainly does not reconcile with the numbers that the company is reporting, particularly for its canned products business. In our opinion, the seasonality defense is out of play for the company based simply on numerous idle company facilities being in production at the same time last year.

When we are given several substantial pieces of financial data that do not add up, we have no option but to question the business in its entirety and we believe regulators and the company’s Hong Kong IPO sponsors should do the same. We also think it’s worth noting again that the company’s actions suggest that its “lapsed” Hong Kong IPO is running into difficulties. We hope both Singapore and Hong Kong regulators view this company with as much scrutiny as we have and we look forward to a point by point response from the company.

Disclosure: Neither GeoInvesting, nor any of its employees, has a short position in Sino Grandness due to vague trading laws in conjunction with research reports in Singapore.

Disclaimer

You agree that you shall not republish or redistribute in any medium any information on the contained in this report without our express written authorization. You acknowledge that GeoInvesting is not registered as an exchange, broker-dealer or investment advisor under any federal or state securities laws, and that GeoInvesting has not provided you with any individualized investment advice or information. Nothing in this report should be construed to be an offer or sale of any security. You should consult your financial advisor before making any investment decision or engaging in any securities transaction as investing in any securities mentioned in the report may or may not be suitable to you or for your particular circumstances. Unless otherwise noted and/or explicitly disclosed, GeoInvesting, its affiliates, and the third party information providers providing content to the report may hold short positions, long positions or options in securities mentioned in the report and related documents and otherwise may effect purchase or sale transactions in such securities.

GeoInvesting, its affiliates, and the information providers make no warranties, express or implied, as to the accuracy, adequacy or completeness of any of the information contained in the report. All such materials are provided to you on an ‘as is’ basis, without any warranties as to merchantability or fitness neither for a particular purpose or use nor with respect to the results which may be obtained from the use of such materials. GeoInvesting, its affiliates, and the information providers shall have no responsibility or liability for any errors or omissions nor shall they be liable for any damages, whether direct or indirect, special or consequential even if they have been advised of the possibility of such damages. In no event shall the liability of GeoInvesting, any of its affiliates, or the information providers pursuant to any cause of action, whether in contract, tort, or otherwise exceed the fee paid by you for access to such materials in the month in which such cause of action is alleged to have arisen. Furthermore, GeoInvesting shall have no responsibility or liability for delays or failures due to circumstances beyond its control.

Our research and reports express our opinions, which we have based upon generally available information, field research, inferences and deductions through our due diligence and analytical process. To the best of our ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the stock covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind, whether express or implied.